- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Better Home & Finance Holding Among 3 High Growth Stocks With Strong Insider Confidence

As the S&P 500 and Dow Jones Industrial Average reach new highs, investors are demonstrating resilience despite ongoing concerns, such as the DOJ probe into Fed Chair Powell. In this robust market environment, identifying growth companies with high insider ownership can be pivotal, as insider confidence often signals strong potential for future performance.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Super Micro Computer (SMCI) | 13.9% | 50.7% |

| StubHub Holdings (STUB) | 14.1% | 59% |

| SES AI (SES) | 12% | 68.9% |

| Ryan Specialty Holdings (RYAN) | 15.5% | 45.6% |

| Prairie Operating (PROP) | 32.2% | 100% |

| Niu Technologies (NIU) | 37.2% | 93.7% |

| Credo Technology Group Holding (CRDO) | 10% | 30.7% |

| Corcept Therapeutics (CORT) | 11.5% | 43.6% |

| Bitdeer Technologies Group (BTDR) | 33.4% | 135.5% |

| Astera Labs (ALAB) | 10.5% | 29.0% |

We're going to check out a few of the best picks from our screener tool.

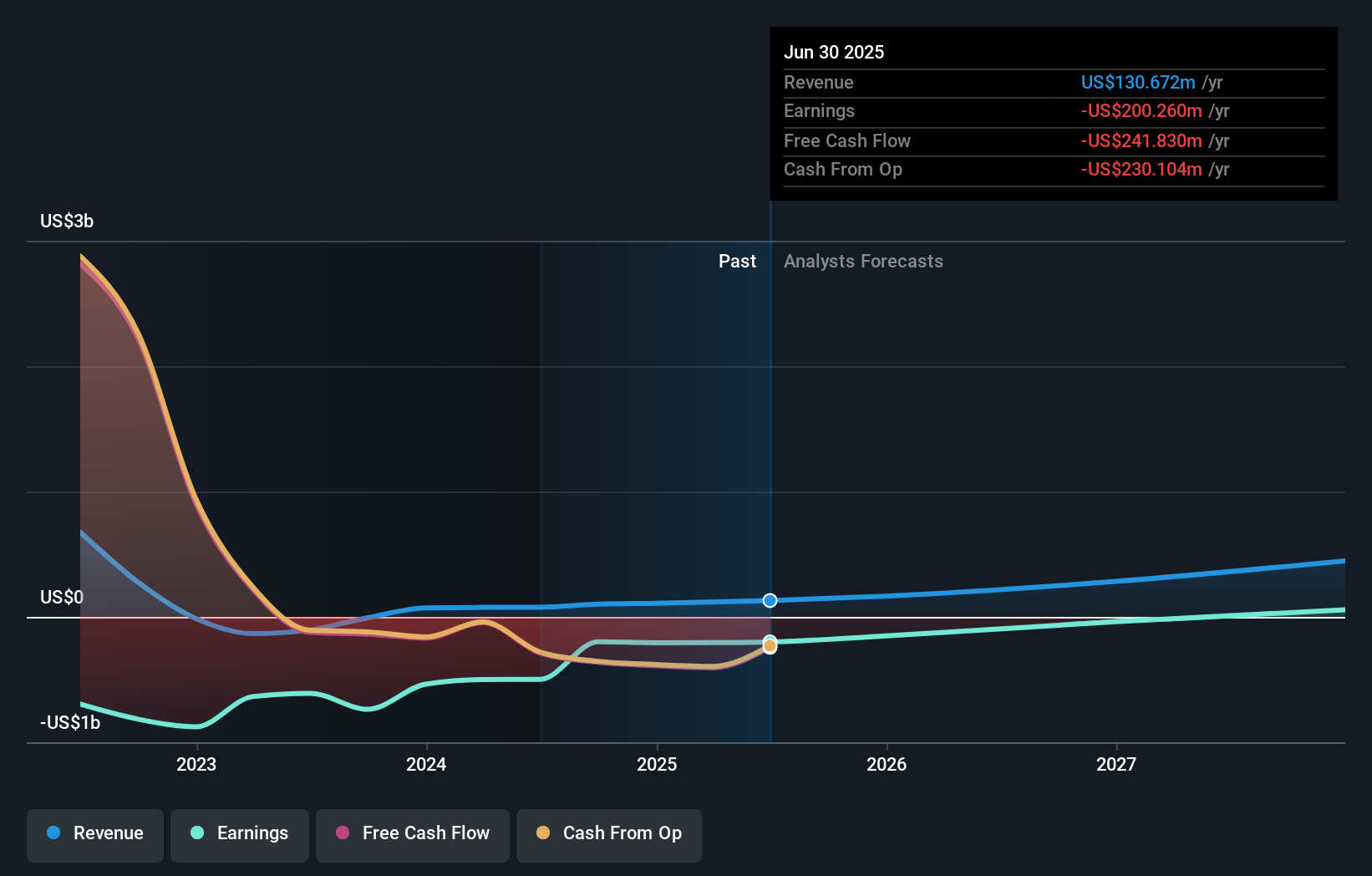

Better Home & Finance Holding (BETR)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Better Home & Finance Holding Company operates as a homeownership company in the United States with a market cap of approximately $601.50 million.

Operations: The company generates revenue from its Financial Services segment, totaling $145.55 million.

Insider Ownership: 19.9%

Earnings Growth Forecast: 95.3% p.a.

Better Home & Finance Holding is experiencing rapid growth, with revenue expected to increase by 50.9% annually, significantly outpacing the US market average. Despite high volatility and substantial insider selling recently, the company anticipates becoming profitable within three years. Recent executive appointments aim to bolster strategic alignment and operational efficiency as Better expands its AI-driven home finance offerings. However, financial challenges persist with a net loss of US$39.13 million reported for Q3 2025.

- Click here and access our complete growth analysis report to understand the dynamics of Better Home & Finance Holding.

- Our valuation report unveils the possibility Better Home & Finance Holding's shares may be trading at a premium.

Cardinal Infrastructure Group (CDNL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Cardinal Infrastructure Group Inc. is a civil contracting company offering infrastructure services across various sectors in the United States, with a market cap of $877.87 million.

Operations: The company's revenue is primarily derived from its Heavy Construction segment, which generated $395.16 million.

Insider Ownership: 12.8%

Earnings Growth Forecast: 27.7% p.a.

Cardinal Infrastructure Group has seen substantial insider buying recently, indicating confidence in its growth prospects. Despite having a high level of debt and illiquid shares, the company is positioned for significant earnings growth at 27.7% annually over the next three years, outpacing the US market average. Recent developments include an IPO raising US$241.5 million and inclusion in the NASDAQ Composite Index, which may enhance visibility and investor interest.

- Unlock comprehensive insights into our analysis of Cardinal Infrastructure Group stock in this growth report.

- Upon reviewing our latest valuation report, Cardinal Infrastructure Group's share price might be too optimistic.

Warby Parker (WRBY)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Warby Parker Inc. operates in the United States and Canada, offering eyewear products, with a market cap of $3.46 billion.

Operations: The company generates revenue of $850.58 million from its Holistic Vision Care segment in the United States and Canada.

Insider Ownership: 15.3%

Earnings Growth Forecast: 48.7% p.a.

Warby Parker has demonstrated strong growth potential, becoming profitable this year with net income of US$7.59 million for the first nine months of 2025, compared to a loss last year. The company forecasts revenue between US$871 million and US$874 million for 2025, marking a 13% increase. Despite high share price volatility and significant insider selling recently, earnings are expected to grow significantly at 48.7% annually over the next three years, outpacing market averages.

- Delve into the full analysis future growth report here for a deeper understanding of Warby Parker.

- Our valuation report here indicates Warby Parker may be overvalued.

Key Takeaways

- Investigate our full lineup of 211 Fast Growing US Companies With High Insider Ownership right here.

- Contemplating Other Strategies? We've found 12 US stocks that are forecast to pay a dividend yeild of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com