- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Cohu (COHU) Valuation Check After Needham Upgrade And AI Linked Neon HBM Order Momentum

Cohu (COHU) is back on investor radars after an upgrade from Needham, repeat orders for its Neon HBM inspection systems tied to AI demand, and quarterly earnings that topped analyst expectations.

See our latest analysis for Cohu.

Cohu’s share price has been volatile, with an 11.99% 7 day share price return and 30.69% 90 day share price return to US$26.06. However, the 1 year total shareholder return is slightly negative and longer term total returns remain weak. This suggests that recent momentum is building from a low base as AI related orders and the Needham upgrade reset expectations around its risk and growth profile.

If Cohu’s AI angle has caught your attention, it could be worth widening the lens to other chip names using Simply Wall St’s screener for high growth tech and AI stocks.

With Cohu trading at US$26.06 and analyst targets clustered around US$29 to US$30, the recent AI driven enthusiasm is clear. The key question is whether the stock remains underappreciated or if the market is already pricing in the next leg of growth.

Most Popular Narrative: 10.8% Undervalued

At a last close of US$26.06 versus a narrative fair value near US$29.20, the current setup hinges on how much earnings recovery you think is realistic.

The push towards automation, data analytics, and AI-driven yield/process optimization through Cohu's software suite (DI-Core, Tignis) supports an ongoing shift to higher-margin, recurring software and services revenue, which is expected to enhance long-term net margins and earnings stability.

Curious how a still unprofitable company lands on that fair value? The narrative leans heavily on rapid revenue gains, margin repair, and a future P/E reset. Want to see how those moving parts fit together into one price tag?

Result: Fair Value of $29.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on AI and HBM orders holding up and Cohu winning enough qualifications, while any manufacturing hiccups in Asia could quickly challenge those fair value assumptions.

Find out about the key risks to this Cohu narrative.

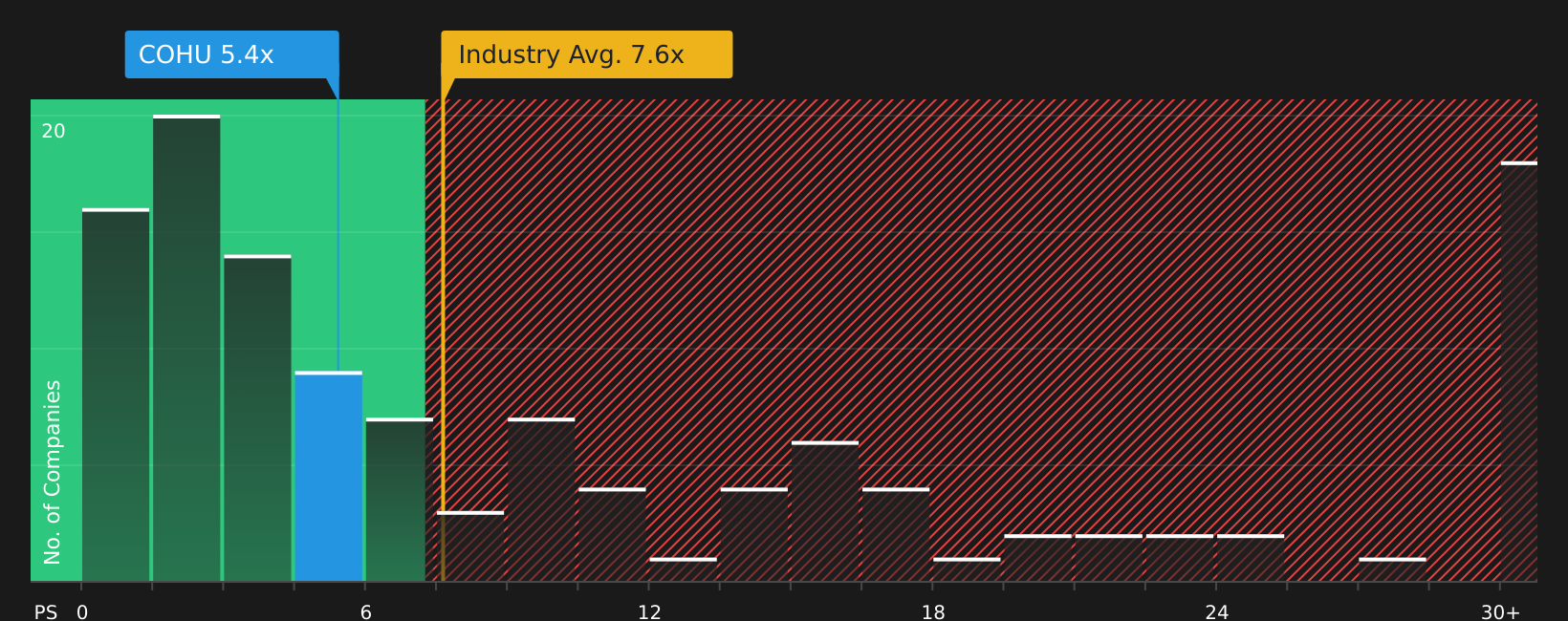

Another View: What The Sales Multiple Is Saying

Looking at Cohu through its P/S ratio makes the picture more cautious. The shares trade at 2.9x sales versus a fair ratio of 2.8x, so the stock appears slightly expensive on this basis, even though it sits well below the US semiconductor industry at 5.2x and peers at 5.5x. That gap can hint at some protection if sentiment cools, but it also suggests less obvious upside if AI optimism fades.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Cohu Narrative

If you are not fully on board with this view or simply prefer to test the numbers yourself, you can build a fresh narrative in just a few minutes and put your own stamp on it: Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Cohu.

Looking for more investment ideas?

If Cohu has sharpened your interest in AI and semiconductors, do not stop here. The next opportunity for your portfolio could be sitting in another corner of the market.

- Spot potential value ahead of the crowd by checking out these 878 undervalued stocks based on cash flows that still trade at prices many investors have not focused on yet.

- Ride the AI momentum more broadly by scanning these 28 AI penny stocks that are tied to machine learning, data infrastructure, and next generation computing demand.

- Add income potential to your watchlist by screening these 11 dividend stocks with yields > 3% that might suit a more cash focused approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com