- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At WEBTOON Entertainment (WBTN) Valuation After Securities Class Action Is Allowed To Proceed

The recent decision by the U.S. District Court to let a securities fraud class action proceed against WEBTOON Entertainment (WBTN), focused on alleged IPO era user metrics, has sharpened investor attention on the company’s legal and reputational exposure.

See our latest analysis for WEBTOON Entertainment.

WEBTOON Entertainment’s share price closed at $13.69, with a 7 day share price return of 5.07% and a 30 day share price return of 1.26%, while the 90 day share price return of 18.02% indicates fading momentum despite a 1 year total shareholder return of 3.32%. Recent developments, including the court’s decision to allow the securities class action to proceed and a US$32.8m private placement to The Walt Disney Company at $12.29 per share, have kept both growth expectations and legal risks in focus.

If legal risk and partnership headlines have you reassessing WEBTOON, it could be a good moment to broaden your watchlist with fast growing stocks with high insider ownership.

With WEBTOON trading at $13.69 against an indicated intrinsic value gap and a recent private placement at $12.29, the real question is whether current legal and growth headlines create a buying window, or if markets already price in future growth.

Most Popular Narrative: 13.4% Undervalued

With WEBTOON Entertainment last closing at $13.69 against a narrative fair value of $15.81, the valuation gap hinges on how major content partnerships translate into monetization over time.

The recently announced multi-year collaboration with Disney (encompassing Marvel, Star Wars, and 20th Century Studios IPs) is expected to accelerate new user acquisition and engagement, especially among younger, mobile-native demographics; this should drive strong top-line revenue and expand the monetizable user base in the mid

to long term.

Curious what kind of revenue build, margin lift, and future P/E multiple are embedded here? The narrative focuses on ambitious growth, a potential profitability inflection, and a premium earnings multiple that is typically associated with category leaders.

According to the most widely followed narrative, this fair value uses an 8.29% discount rate and is based on expectations for faster revenue expansion, improving margins, and WEBTOON eventually reaching positive earnings, along with a relatively high future P/E multiple to support the long term upside implied in the model.

Result: Fair Value of $15.81 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on reversing recent pressure on global MAUs and avoiding further margin strain if content, creator, and marketing spend outpace near term revenue.

Find out about the key risks to this WEBTOON Entertainment narrative.

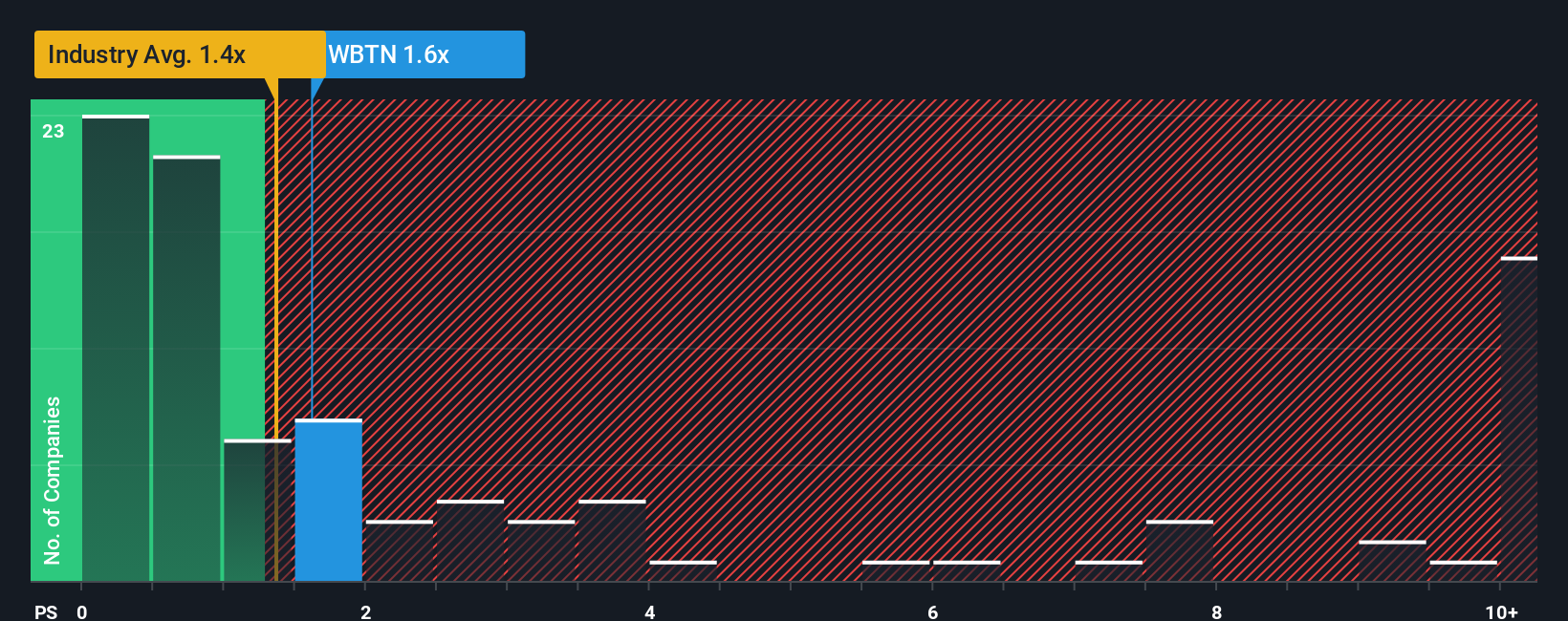

Another View: Price To Sales Sends A Different Signal

While the narrative fair value of US$15.81 points to upside, the current P/S ratio of 1.3x tells a more cautious story. It sits above both the US Interactive Media and Services industry at 1x and the peer average at 0.9x, and it is also above the fair ratio of 1.2x suggested by our work.

In practice, that means you are paying more per dollar of revenue than both the sector and closest peers, with limited room for disappointment if growth or margins fall short. If the market moves closer to the fair ratio or peer levels instead, would WEBTOON still look as appealing to you?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own WEBTOON Entertainment Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a personalized WEBTOON view in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding WEBTOON Entertainment.

Ready For More Investment Ideas?

If WEBTOON has sharpened your thinking, do not stop here. The next move could be in the ideas you have not checked yet.

- Spot potential mispricings by scanning these 876 undervalued stocks based on cash flows for opportunities that may offer more attractive entry points on a cash flow basis.

- Target income opportunities by reviewing these 11 dividend stocks with yields > 3% to explore options that aim to combine yield with underlying business strength.

- Explore growth themes by tracking these 28 AI penny stocks focused on artificial intelligence and related technologies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com