- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Exail Technologies (ENXTPA:EXA) Valuation After New Defense Drone Contract Wins

Recent contract wins for Exail Technologies (ENXTPA:EXA) in autonomous surface and mine neutralization drones are drawing fresh attention as investors weigh what expanded defense roles and recurring revenue potential might mean for the stock.

See our latest analysis for Exail Technologies.

The back to back defense contracts appear to have arrived during a strong run for the shares, with a 7 day share price return of 28.83% and a 1 month share price return of 18.78% contributing to a very large 1 year total shareholder return. Taken together, these figures suggest that momentum has been building rather than fading.

If Exail’s drone wins have caught your eye, this can be a good moment to see what else is moving in aerospace and defense by scanning aerospace and defense stocks.

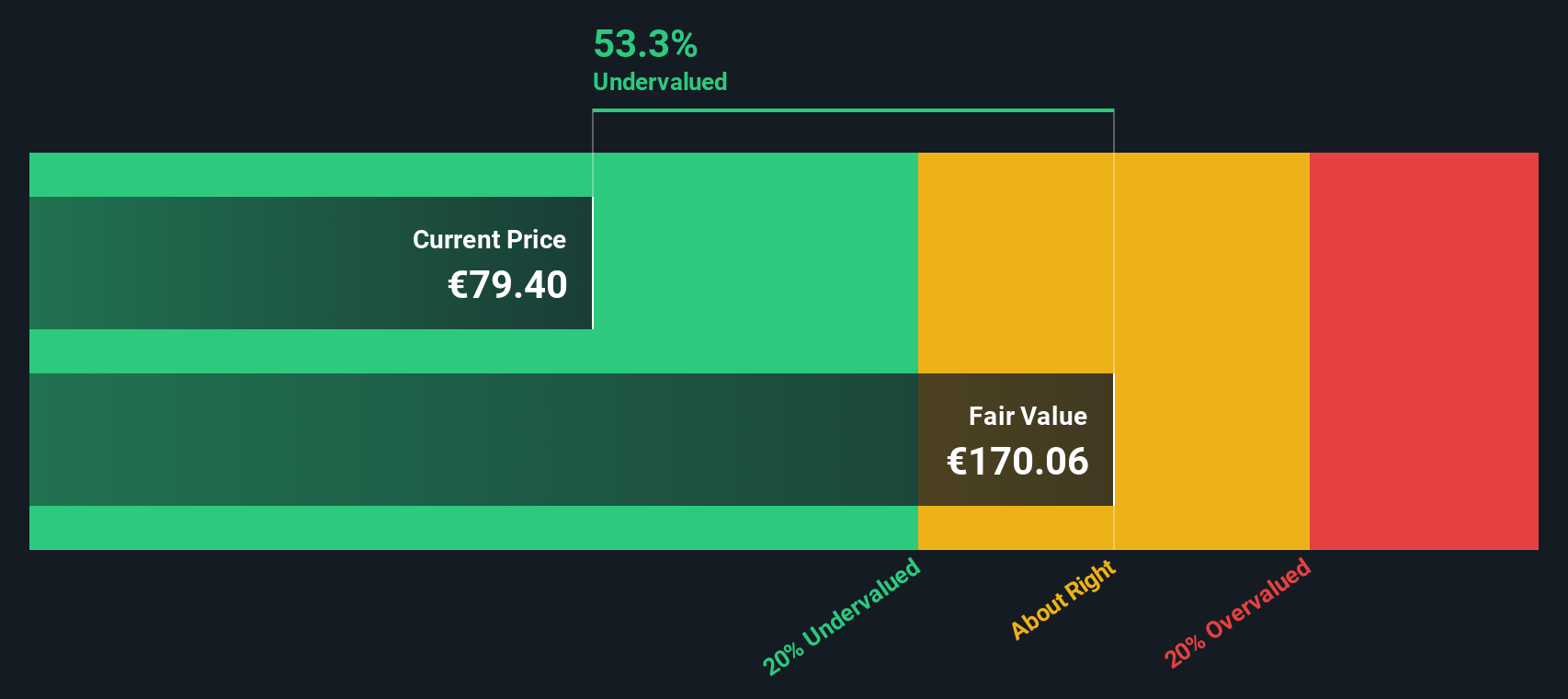

With Exail shares up sharply over the past year, yet trading at what appears to be a roughly 35% discount to one intrinsic value estimate and below analyst targets, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Price to Sales of 3.9x: Is it justified?

On the headline numbers, Exail Technologies trades on a P/S of 3.9x, which screens as expensive compared with both peers and an estimated fair level.

The P/S ratio compares the company’s market value to its revenue and is a common shorthand for how much investors are paying for each €1 of sales, especially when profit history is short or still stabilising.

For Exail, the current 3.9x P/S sits well above the estimated fair P/S of 2x that our models suggest the market could move toward. It is also above the European aerospace and defense average of 2.3x and the peer average of 3.3x, which all point to the market assigning a premium price tag to its current revenue base.

Explore the SWS fair ratio for Exail Technologies

Result: Price-to-Sales of 3.9x (OVERVALUED)

However, you also have to weigh risks, such as a sharp reversal in recent share price momentum and any disappointment around defense contract timing or profitability.

Find out about the key risks to this Exail Technologies narrative.

Another View: DCF Points the Other Way

The P/S of 3.9x suggests Exail Technologies is expensive, yet our DCF model points to a very different picture. On that approach, the shares trade about 35% below an estimated fair value of roughly €162.21 versus the current €105 price. This frames the recent run up as potentially less stretched than it looks.

That gap between a rich P/S, sector premiums and a discount on the SWS DCF model raises a simple question for you as an investor: which signal do you trust more, the headline revenue multiple or the long term cash flow estimate?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Exail Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 884 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Exail Technologies Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to build on your own research, you can put together a personalised view in just a few minutes with Do it your way.

A great starting point for your Exail Technologies research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about putting your research to work, do not stop at a single stock. Use targeted screens to spot ideas others might overlook.

- Zero in on potential mispriced opportunities by scanning these 884 undervalued stocks based on cash flows where current prices sit below cash flow based estimates.

- Hunt for growth stories at lower price points with these 3545 penny stocks with strong financials that pair smaller market caps with stronger fundamentals.

- Tap into the intersection of medicine and algorithms through these 29 healthcare AI stocks that focus on companies applying AI to real world health problems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com