- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At United Bankshares (UBSI) Valuation As Recent Returns Draw Investor Attention

What recent performance suggests about United Bankshares

Without a single headline event driving attention, United Bankshares (UBSI) is drawing interest as investors reassess regional bank valuations by using its recent share performance and fundamentals as a reference point.

See our latest analysis for United Bankshares.

At a share price of US$39.28, United Bankshares has seen a 6.1% 90 day share price return and a 10.8% 1 year total shareholder return, which hints at gradually improving sentiment rather than fast building momentum.

If regional banks are on your radar, this could be a good moment to broaden your search and check out fast growing stocks with high insider ownership as potential next ideas.

With United Bankshares trading at US$39.28 and sitting about 4% below the average analyst price target and roughly 35% below one estimate of intrinsic value, you have to ask whether there is a genuine opportunity here or whether the market is already incorporating expectations for future growth.

Price-to-Earnings of 12.8x: Is it justified?

At a last close of US$39.28, United Bankshares trades on a P/E of 12.8x, which screens as good value against peers but slightly expensive against both its own fair ratio and the wider US Banks industry.

The P/E ratio compares what you pay today for each dollar of earnings, so for a mature, profitable bank like United Bankshares it is a common yardstick investors use to line up expectations.

Here, the picture is mixed. On one hand, the SWS fair ratio work suggests a P/E of 12.1x could be more in line with its fundamentals, which would make the current 12.8x look a touch rich if the market eventually gravitates toward that level. On the other hand, the same 12.8x P/E looks cheaper than the peer average of 15.6x, yet a bit more expensive than the broader US Banks industry at 11.9x, which hints that investors might be paying a small premium to the sector while still sitting below closer peers.

Explore the SWS fair ratio for United Bankshares

Result: Price-to-Earnings of 12.8x (ABOUT RIGHT)

However, you still have to weigh typical bank risks, such as credit quality in a weaker economy and pressure on net interest margins if funding costs remain elevated.

Find out about the key risks to this United Bankshares narrative.

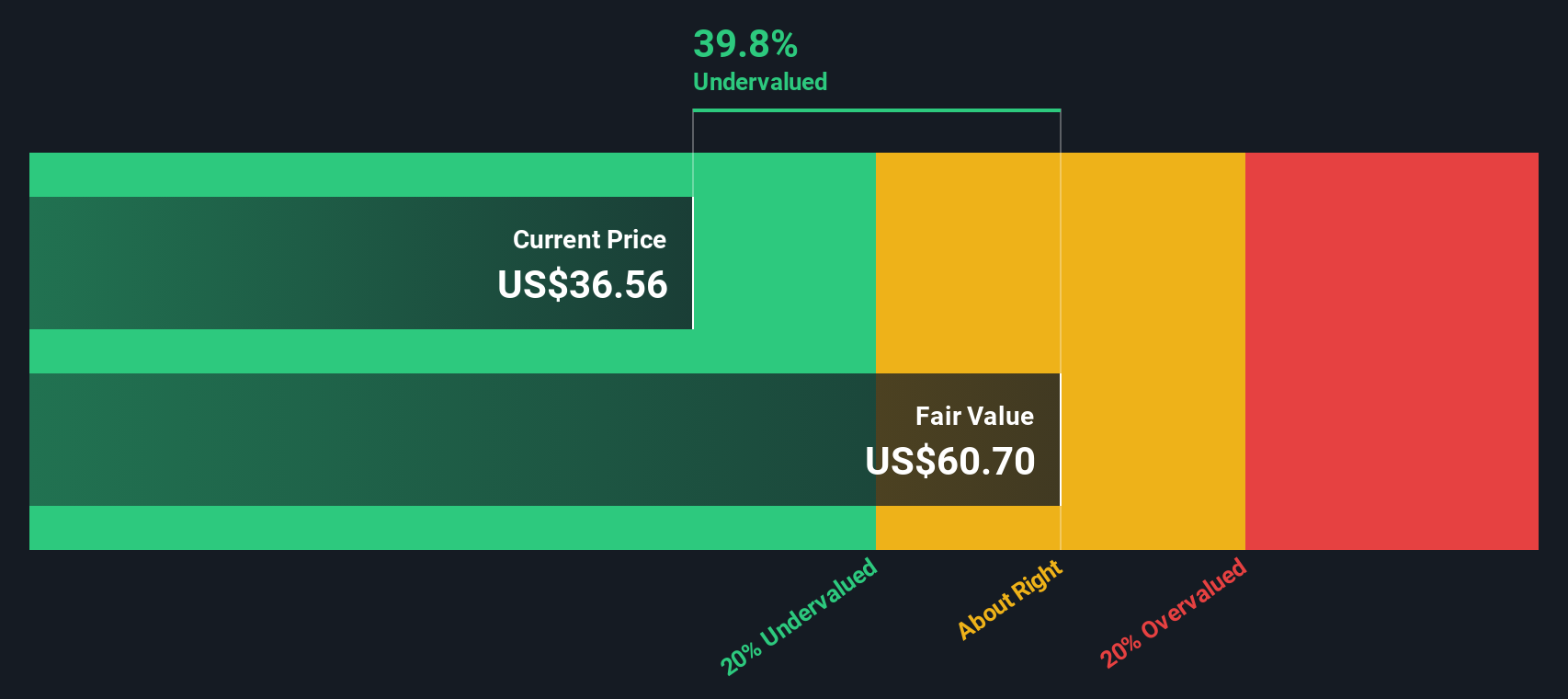

Another view: DCF points in a different direction

While the 12.8x P/E suggests United Bankshares is roughly in line with where the market often prices banks, our DCF model points elsewhere. With the shares at US$39.28 and a fair value estimate of US$60.88, the model implies the stock is undervalued. For you, the question is which signal you trust more.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out United Bankshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 884 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own United Bankshares Narrative

If you see the numbers differently or prefer to check every assumption yourself, you can build your own view in minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding United Bankshares.

Ready for more investment ideas?

If United Bankshares has sharpened your thinking, do not stop here. Your next strong idea could be sitting one screen away.

- Target dependable cash generators by zeroing in on these 12 dividend stocks with yields > 3% that aim to balance income and resilience in your portfolio.

- Seek long term growth themes by scanning these 26 AI penny stocks that sit at the crossroads of technology and real world adoption.

- Look for potentially mispriced opportunities by focusing on these 884 undervalued stocks based on cash flows that may offer more earnings for every dollar you put to work.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com