- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Metaplanet (TSE:3350) Valuation After Recent Share Price Momentum And DCF Signal

Metaplanet (TSE:3350) has drawn investor attention recently as its mix of hotel operations, bitcoin treasury activities, and Web3 related businesses trades around ¥510. This has invited fresh questions about how this blend is being valued.

See our latest analysis for Metaplanet.

The recent 1 day share price return of 9% and 7 day gain of 26% cap a 30 day share price return of 30%. However, the 90 day move shows an 11% decline, while the 1 year total shareholder return of 35% sits against a very large 3 year total shareholder return. This suggests momentum has recently picked up again after a sharp earlier rerating.

If Metaplanet has put high growth themes like bitcoin and Web3 on your radar, it could be a good moment to look at high growth tech and AI stocks as well.

With revenue growth near 97%, net income growth around 31% and the share price still well below an analyst target of ¥1,927.5, you have to ask: is Metaplanet undervalued, or is the market already pricing in future growth?

Price-to-Earnings of 28.8x: Is it justified?

Metaplanet's current valuation sits at a P/E of 28.8x, while the last close is ¥510, so the key question is how that earnings multiple stacks up against both peers and a fair reference level.

The P/E ratio compares the share price to earnings per share and is a common way investors gauge how much they are paying for each unit of profit. For a company that has only recently become profitable and is active in areas like hotels, bitcoin and Web3, the market can use a higher multiple to reflect expected earnings growth rather than current earnings alone.

According to Simply Wall St's fair ratio work, 28.8x is described as good value compared to an estimated fair P/E of 48.7x. This suggests the market is pricing Metaplanet at a discount to a level the regression analysis points to as reasonable. However, the same 28.8x P/E is described as expensive against both the peer average of 18.4x and the broader JP Hospitality industry average of 23.8x. This means the market is assigning a premium multiple versus its sector and closer competitors.

Explore the SWS fair ratio for Metaplanet

Result: Price-to-Earnings of 28.8x (ABOUT RIGHT)

However, there are clear pressure points here, including bitcoin related earnings volatility and the risk that hotel and Web3 businesses do not scale as investors expect.

Find out about the key risks to this Metaplanet narrative.

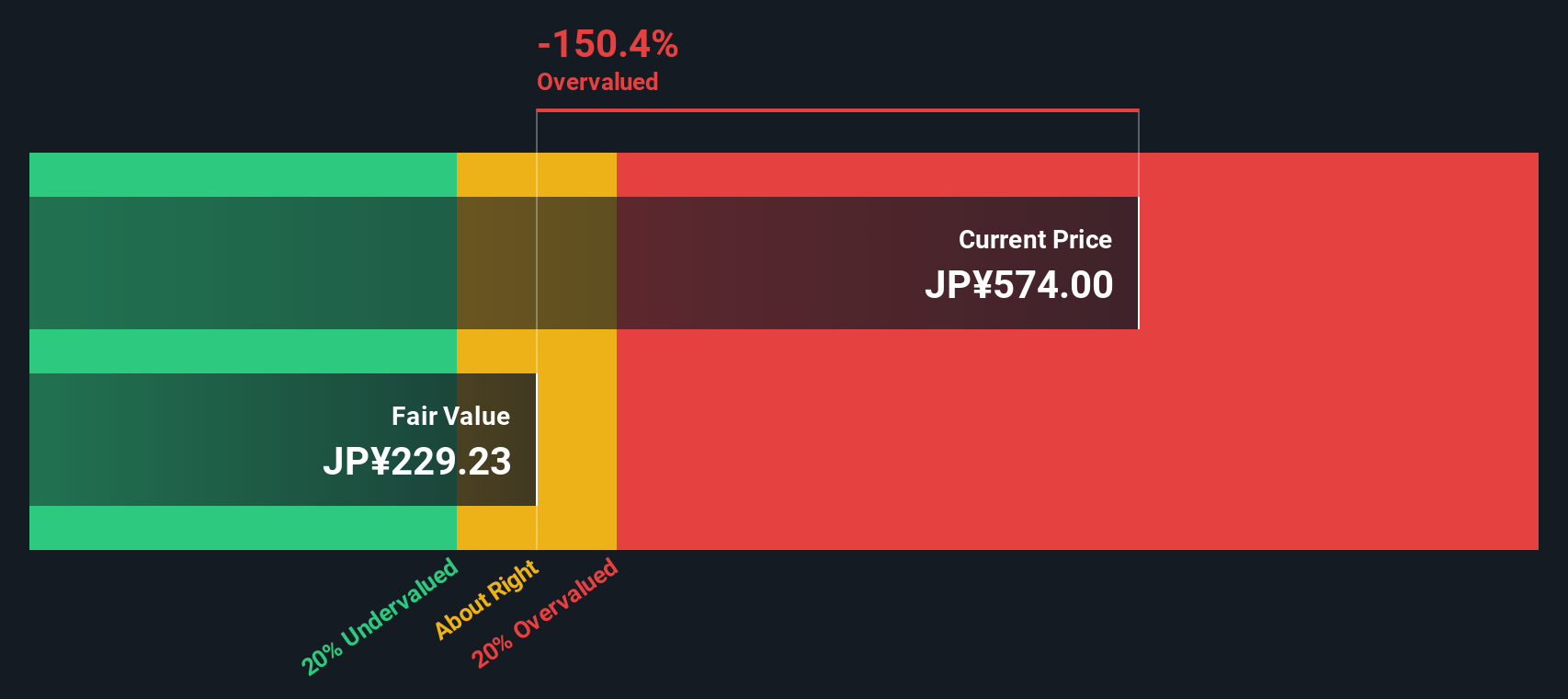

Another View: What Does The DCF Say?

While the 28.8x P/E suggests Metaplanet might be reasonably priced against its fair ratio, our DCF model points in a very different direction. At a share price of ¥510 versus an estimated fair value of ¥35.86, the DCF output frames the stock as heavily overvalued. Which signal receives more attention?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Metaplanet for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Metaplanet Narrative

If you see the numbers differently and want to stress test your own view, you can build a customised Metaplanet story in just a few minutes, starting with Do it your way.

A great starting point for your Metaplanet research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Metaplanet has sharpened your appetite for opportunities, do not stop here. Broaden your watchlist now so you are not late to the next idea.

- Target potential value gaps by checking out these 877 undervalued stocks based on cash flows that line up price with underlying cash flows.

- Spot early movers in artificial intelligence by scanning these 25 AI penny stocks shaping real world applications.

- Tap into fast growing digital asset themes with these 79 cryptocurrency and blockchain stocks tied to cryptocurrency and blockchain activity.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com