- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Chewy (CHWY) Valuation Check As Shares Hover Near Flat One Month Return

Chewy (CHWY) has drawn investor attention after recent trading left the shares with a return of about 0% over the past month, while the past 3 months show roughly an 11% decline.

See our latest analysis for Chewy.

Chewy’s 1-day share price return of 1.33% and 7-day share price return of 0.69% sit against a 90-day share price decline of 11%. The 1-year total shareholder return of 9.66% and 5-year total shareholder return of 65.53% indicate that longer term momentum has been fading.

If Chewy’s recent moves have you reassessing your watchlist, this could be a useful moment to broaden your search with fast growing stocks with high insider ownership.

With Chewy trading around $33.49 and sitting on an intrinsic discount of about 43%, plus a value score of 3, you have to ask whether the stock is genuinely undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 25.5% Undervalued

With Chewy’s fair value estimate at about $44.95 versus a last close of $33.49, the most followed narrative argues the current price undervalues its long term earnings power.

The company's increased focus on innovation, such as the Chewy+ membership and mobile app improvements, is associated with new customer acquisition and higher conversion rates, which in turn supports revenue growth and net sales per active customer (NSPAC). Active customer growth is described as having reached an inflection point, with expectations for continued growth in 2025 due to improved marketing strategies and customer acquisition channels, which would positively affect top line revenue.

Curious what has to happen for Chewy to justify that higher fair value? The narrative emphasizes steady revenue expansion, resilient margins and a richer earnings multiple. The exact mix of growth, profitability and valuation expectations might be different from what many investors anticipate.

Result: Fair Value of $44.95 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story could change quickly if Chewy’s heavy reliance on Autoship subscriptions, or the push into vet clinics and ads, fails to deliver the expected customer and revenue traction.

Find out about the key risks to this Chewy narrative.

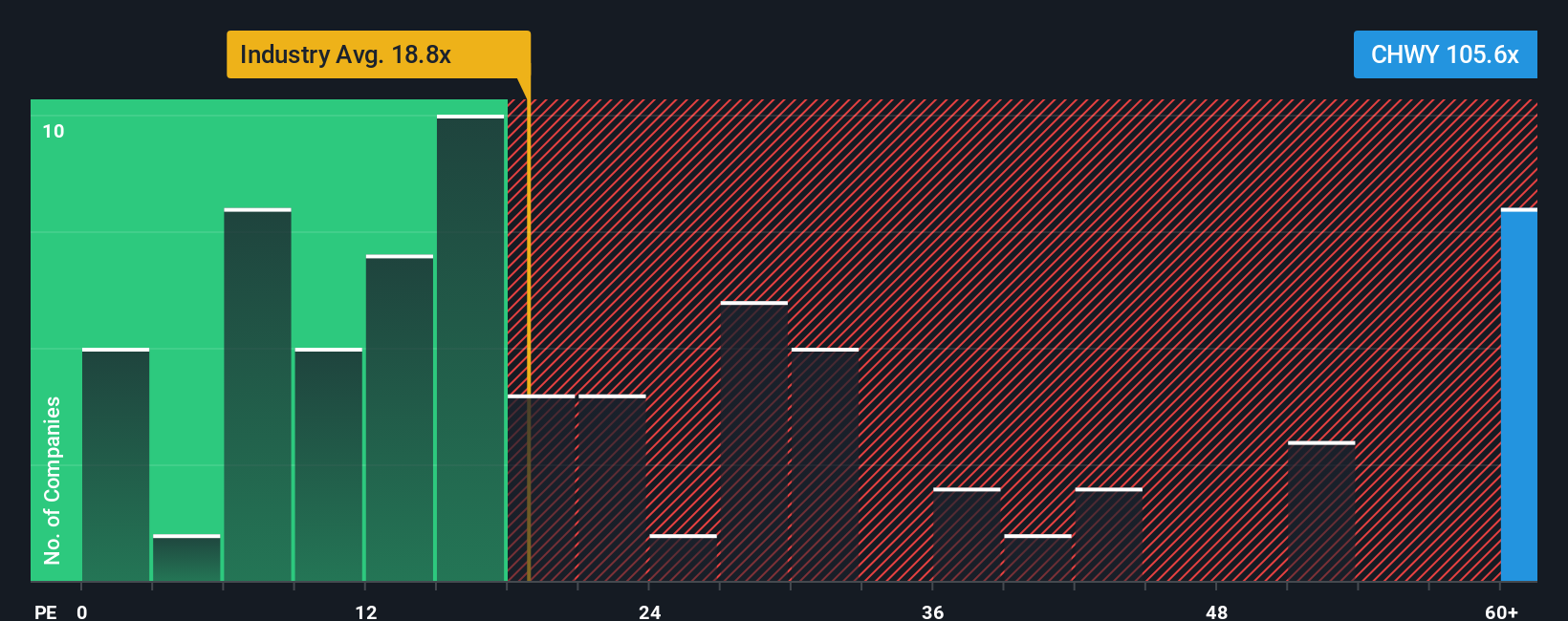

Another View: High P/E Puts Pressure On The Story

Chewy screens as undervalued on fair value estimates, yet the current P/E of 67.3x is far higher than the US Specialty Retail average of 19.8x and the fair ratio of 28.6x. That gap points to real valuation risk if expectations cool, so which signal do you trust more?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Chewy Narrative

If you see the numbers differently or prefer to look under the hood yourself, you can build a custom Chewy story in just a few minutes, starting with Do it your way.

A great starting point for your Chewy research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready For Your Next Idea?

If Chewy is on your radar but you want a fuller picture of potential opportunities, now is the moment to broaden your search before prices and narratives shift again.

- Target reliable income by scanning these 14 dividend stocks with yields > 3% that may suit an investor who values consistent cash returns.

- Spot potential mispricings by running through these 878 undervalued stocks based on cash flows that might trade below what their cash flows suggest.

- Get ahead of emerging themes by reviewing these 79 cryptocurrency and blockchain stocks shaping the future of payments and digital infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com