- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Investors Interested In NG Energy International Corp.'s (CVE:GASX) Revenues

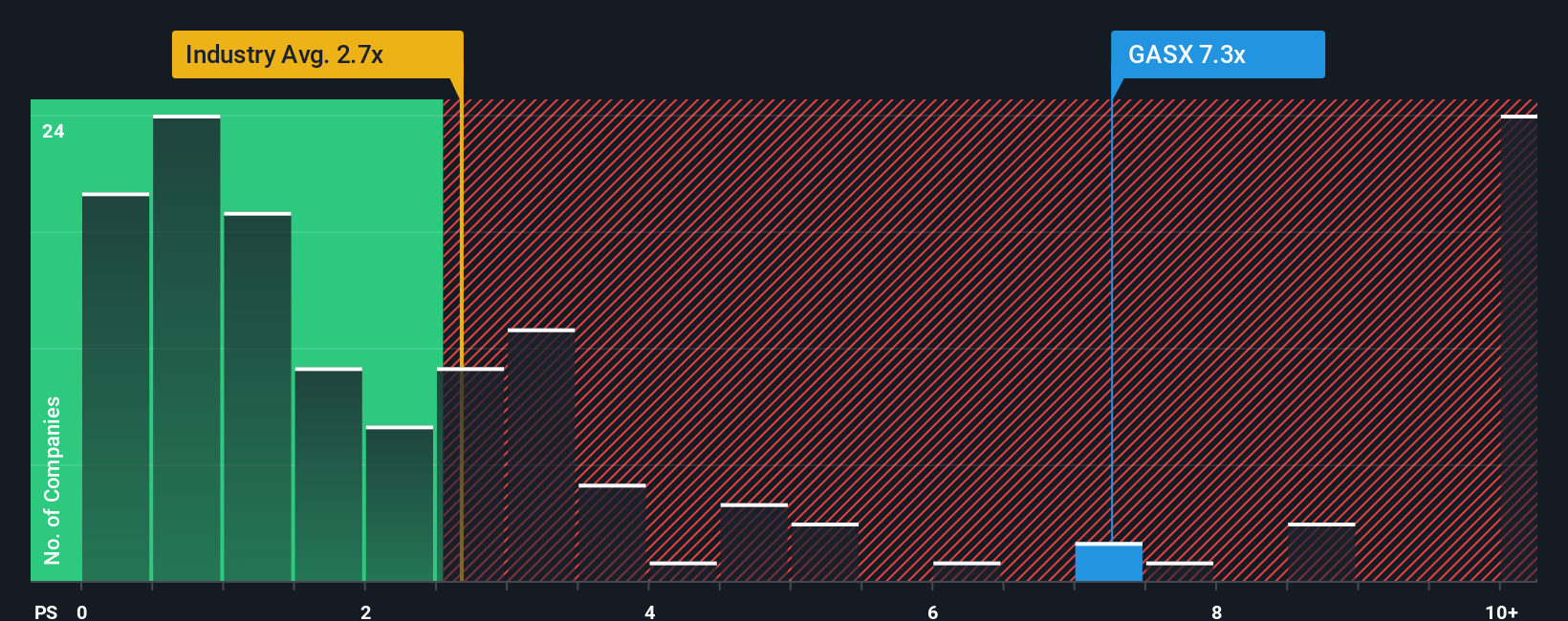

When you see that almost half of the companies in the Oil and Gas industry in Canada have price-to-sales ratios (or "P/S") below 2.7x, NG Energy International Corp. (CVE:GASX) looks to be giving off strong sell signals with its 7.3x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for NG Energy International

How NG Energy International Has Been Performing

With revenue growth that's inferior to most other companies of late, NG Energy International has been relatively sluggish. It might be that many expect the uninspiring revenue performance to recover significantly, which has kept the P/S ratio from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on NG Energy International.Is There Enough Revenue Growth Forecasted For NG Energy International?

The only time you'd be truly comfortable seeing a P/S as steep as NG Energy International's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, we see that the company managed to grow revenues by a handy 2.6% last year. Still, revenue has barely risen at all in aggregate from three years ago, which is not ideal. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Turning to the outlook, the next year should generate growth of 231% as estimated by the sole analyst watching the company. Meanwhile, the rest of the industry is forecast to only expand by 4.6%, which is noticeably less attractive.

With this in mind, it's not hard to understand why NG Energy International's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On NG Energy International's P/S

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our look into NG Energy International shows that its P/S ratio remains high on the merit of its strong future revenues. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with NG Energy International, and understanding these should be part of your investment process.

If these risks are making you reconsider your opinion on NG Energy International, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.