- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Here's Why TransMedics Group (NASDAQ:TMDX) Can Manage Its Debt Responsibly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that TransMedics Group, Inc. (NASDAQ:TMDX) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is TransMedics Group's Debt?

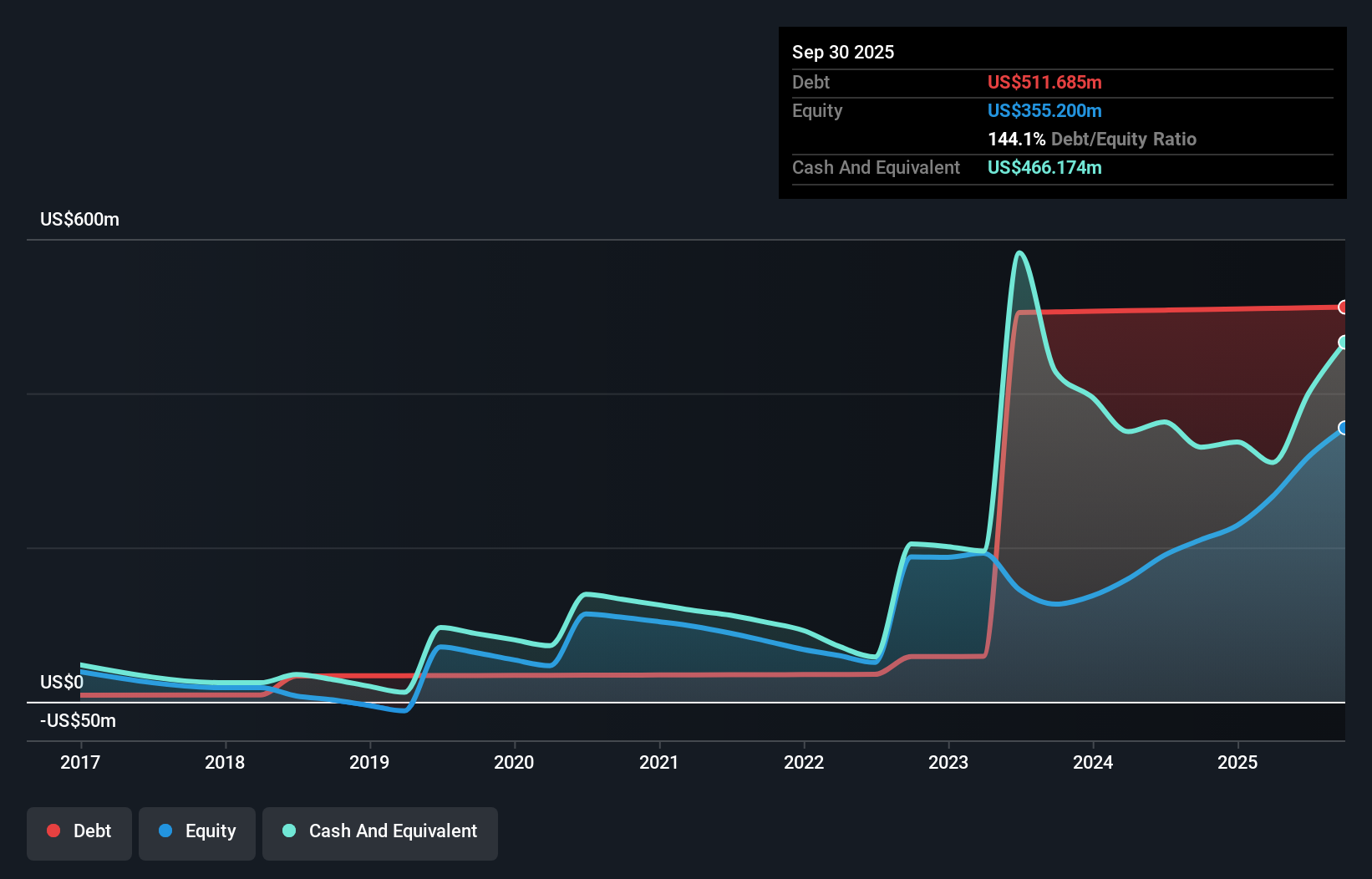

As you can see below, TransMedics Group had US$511.7m of debt, at September 2025, which is about the same as the year before. You can click the chart for greater detail. However, it does have US$466.2m in cash offsetting this, leading to net debt of about US$45.5m.

How Strong Is TransMedics Group's Balance Sheet?

We can see from the most recent balance sheet that TransMedics Group had liabilities of US$79.7m falling due within a year, and liabilities of US$511.1m due beyond that. Offsetting these obligations, it had cash of US$466.2m as well as receivables valued at US$80.7m due within 12 months. So its liabilities total US$44.0m more than the combination of its cash and short-term receivables.

This state of affairs indicates that TransMedics Group's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the US$4.21b company is struggling for cash, we still think it's worth monitoring its balance sheet. Carrying virtually no net debt, TransMedics Group has a very light debt load indeed.

Check out our latest analysis for TransMedics Group

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

TransMedics Group's net debt is only 0.38 times its EBITDA. And its EBIT covers its interest expense a whopping 32.0 times over. So we're pretty relaxed about its super-conservative use of debt. Even more impressive was the fact that TransMedics Group grew its EBIT by 187% over twelve months. That boost will make it even easier to pay down debt going forward. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if TransMedics Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. In the last two years, TransMedics Group basically broke even on a free cash flow basis. While many companies do operate at break-even, we prefer see substantial free cash flow, especially if a it already has dead.

Our View

TransMedics Group's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. We would also note that Medical Equipment industry companies like TransMedics Group commonly do use debt without problems. Looking at the bigger picture, we think TransMedics Group's use of debt seems quite reasonable and we're not concerned about it. After all, sensible leverage can boost returns on equity. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that TransMedics Group insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.