- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Vail Resorts After Recent Share Price Weakness and Cash Flow Valuation Gap

- If you are looking at Vail Resorts and wondering whether the recent share price weakness has finally turned this into a bargain, you are not alone.

- The stock is trading around $139.66 after a choppy spell, down 10.7% over the last week but still up 3.4% over the past month, while longer term returns, such as a 20.3% drop year to date and a 23.1% slide over the last year, keep many investors cautious.

- Recently, investors have been focused on how Vail is navigating changing travel patterns and shifting consumer spending in the leisure sector, including its ongoing investments in resort upgrades and guest experience to stay competitive. There has also been attention on broader macro concerns hitting discretionary spending and how seasonality and weather risks can amplify sentiment swings around ski focused businesses like Vail.

- Despite that mixed backdrop, Vail Resorts currently scores a 5 out of 6 on our valuation checks. This suggests it screens as undervalued on most metrics we track. Next, we will walk through what those different approaches say about the stock today before finishing with a more holistic way to think about its true value.

Find out why Vail Resorts's -23.1% return over the last year is lagging behind its peers.

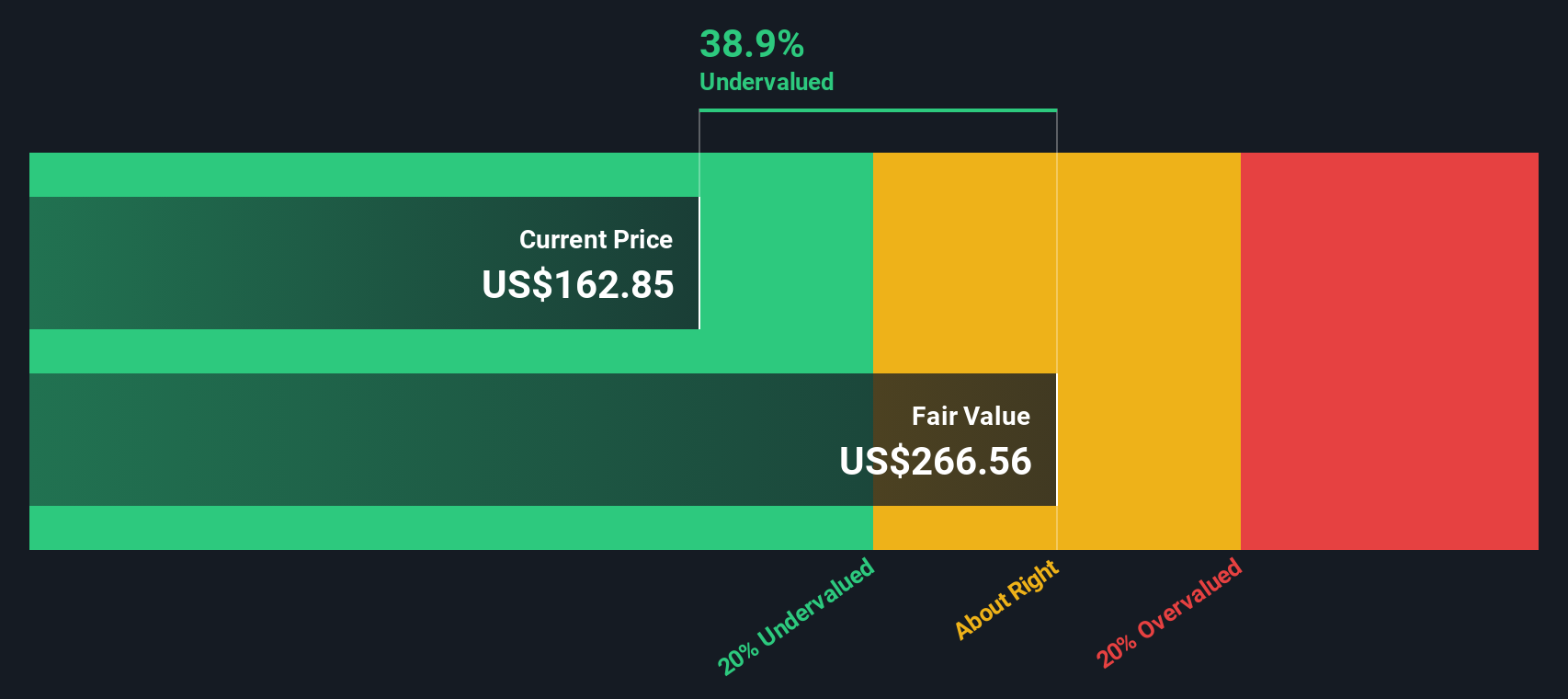

Approach 1: Vail Resorts Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business is worth today by projecting the cash it could generate in the future and then discounting those cash flows back to their value in today’s dollars.

For Vail Resorts, the model starts with last twelve months free cash flow of about $346.5 million. Analysts provide detailed forecasts for the next few years, and Simply Wall St then extrapolates further, resulting in projected free cash flow of around $825.8 million by 2035 as the business grows and matures.

Using a 2 Stage Free Cash Flow to Equity approach, these future cash flows are discounted to arrive at an estimated intrinsic value of roughly $244.04 per share. Compared with the current share price of about $139.66, the DCF suggests the stock is trading at roughly a 42.8% discount and therefore appears materially undervalued on cash flow grounds.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Vail Resorts is undervalued by 42.8%. Track this in your watchlist or portfolio, or discover 903 more undervalued stocks based on cash flows.

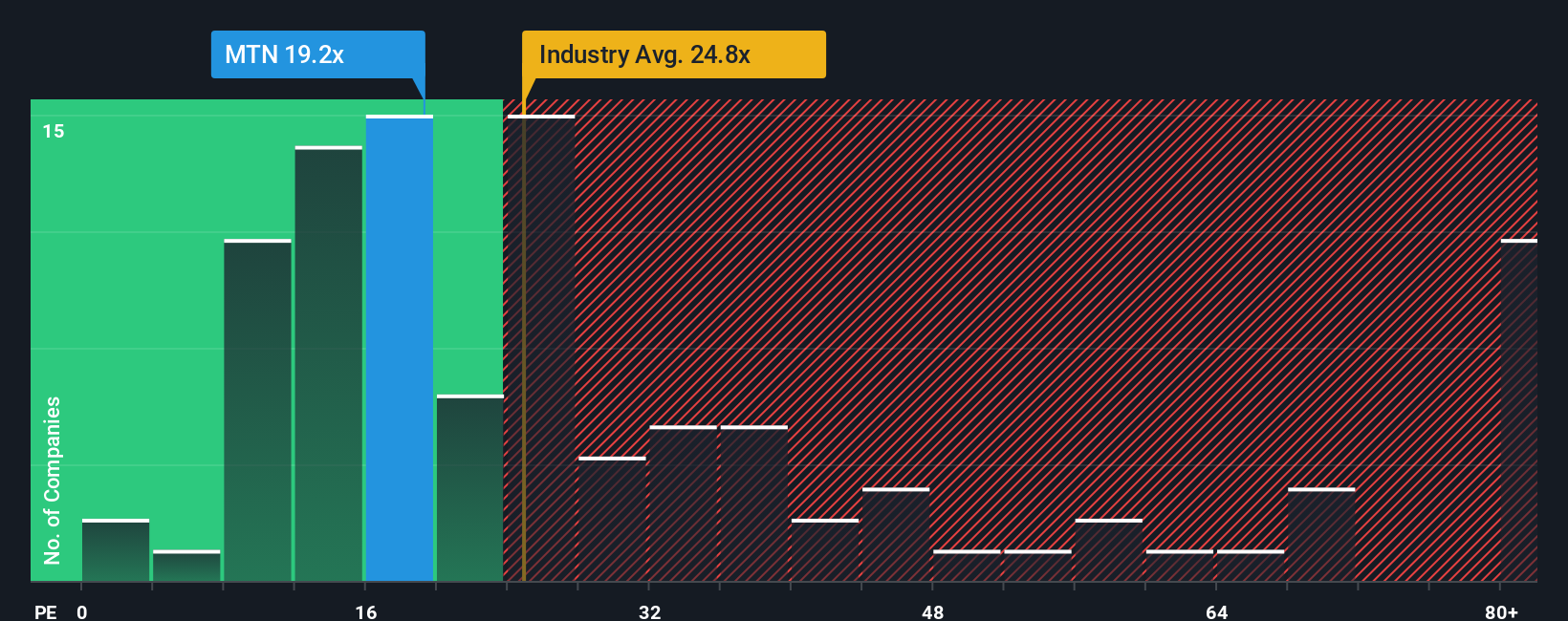

Approach 2: Vail Resorts Price vs Earnings

For profitable companies like Vail Resorts, the price to earnings, or PE, ratio is a useful shorthand for how much investors are willing to pay today for each dollar of current earnings. What counts as a reasonable PE depends on how fast profits are expected to grow and how risky those earnings are, with faster growth and lower risk typically justifying higher multiples.

Vail currently trades on a PE of about 18.75x, which sits below both the Hospitality industry average of roughly 21.87x and the broader peer group average of around 23.16x. Simply Wall St also calculates a proprietary Fair Ratio of 17.71x. This represents the PE that would be expected for Vail after accounting for its earnings growth outlook, profitability, industry, market value and company specific risks.

This Fair Ratio is more tailored than a simple comparison with peers or sector averages because it adjusts for differences in growth profiles, margins, risk levels and company size. Relative to this 17.71x Fair Ratio, Vail’s 18.75x PE is modestly higher, which points to a stock that looks slightly expensive rather than deeply mispriced on earnings.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1460 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Vail Resorts Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page that lets you turn your view of Vail Resorts into a story backed by numbers. You describe what you think will happen to its revenue, earnings and margins, link that story to a financial forecast and fair value, and then use the gap between that fair value and today’s price to help guide decisions. As a bonus, your Narrative automatically updates when fresh news or earnings arrive. For example, a bullish investor might build a Narrative that assumes Vail’s cost efficiencies, technology upgrades and international expansion support a fair value closer to $244 per share. A more cautious investor could instead focus on unstable visitation patterns, macro uncertainty and currency risks to support a fair value nearer $146, with each investor using the same data but expressing a different, transparent path from story to valuation.

Do you think there's more to the story for Vail Resorts? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com