- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

3 Undiscovered Gems In Australia To Enhance Your Investment Portfolio

As the Australian market edges towards the holiday season with a slight dip, largely due to profit-taking and early closures, investors are keeping an eye on small-cap stocks amidst broader market fluctuations. In this environment, identifying promising yet overlooked companies can be key to enhancing your investment portfolio, especially as these gems may offer unique opportunities in times of economic shifts.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 10.00% | 9.57% | ★★★★★★ |

| Joyce | NA | 9.93% | 17.54% | ★★★★★★ |

| Hearts and Minds Investments | NA | 56.27% | 59.19% | ★★★★★★ |

| Euroz Hartleys Group | NA | 1.82% | -25.32% | ★★★★★★ |

| Argosy Minerals | NA | -12.81% | -19.89% | ★★★★★★ |

| Focus Minerals | NA | 75.35% | 51.34% | ★★★★★★ |

| Djerriwarrh Investments | 2.39% | 8.18% | 7.91% | ★★★★★★ |

| Energy World | NA | -47.50% | -44.86% | ★★★★★☆ |

| Zimplats Holdings | 5.44% | -9.79% | -42.03% | ★★★★★☆ |

| Australian United Investment | 1.90% | 5.23% | 4.56% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

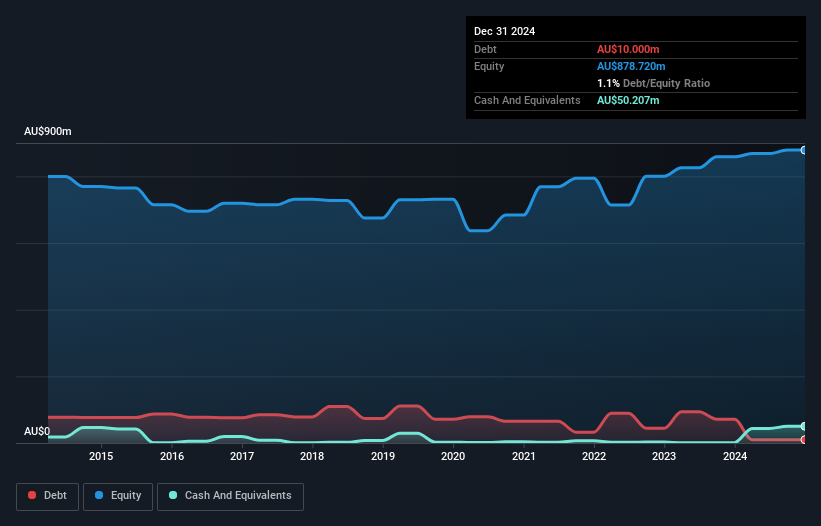

Djerriwarrh Investments (ASX:DJW)

Simply Wall St Value Rating: ★★★★★★

Overview: Djerriwarrh Investments Limited is a publicly owned investment manager with a market capitalization of A$814.87 million.

Operations: Djerriwarrh's primary revenue stream is derived from its portfolio of investments, totaling A$53.07 million.

Djerriwarrh Investments, a smaller player in the Australian market, showcases a solid financial foundation with high-quality earnings. Over the past five years, its earnings have grown at an annual rate of 7.9%, although recent growth of 0.6% lagged behind the industry's 12.7%. The company's debt management appears robust, with interest payments well covered by EBIT at 24 times and a significant reduction in its debt-to-equity ratio from 12.3% to just 2.4%. With a price-to-earnings ratio of 20.8x below the market average of 21.7x, Djerriwarrh offers an attractive valuation for investors seeking stability and potential growth within this niche sector.

- Click here and access our complete health analysis report to understand the dynamics of Djerriwarrh Investments.

Understand Djerriwarrh Investments' track record by examining our Past report.

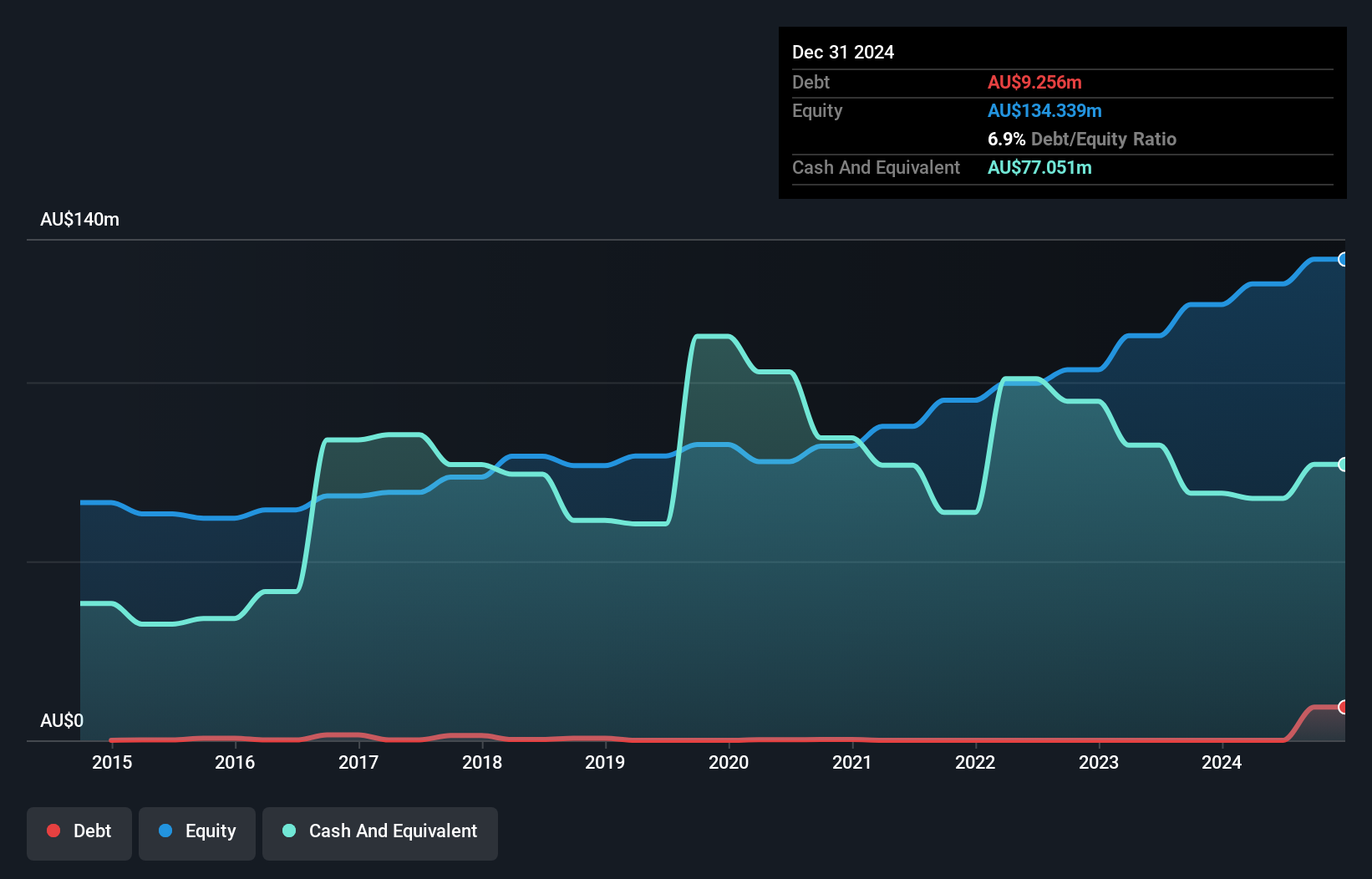

Lycopodium (ASX:LYL)

Simply Wall St Value Rating: ★★★★★☆

Overview: Lycopodium Limited offers engineering and project delivery services across the resources, rail infrastructure, and industrial processes sectors in Australia, with a market capitalization of A$558.75 million.

Operations: Lycopodium's primary revenue stream is derived from the resources sector, contributing A$342.76 million. The company also generates revenue from rail infrastructure and process industries, amounting to A$11.03 million and A$10.08 million respectively.

Lycopodium, a nimble player in the engineering consulting realm, is trading at a 44% discount to its estimated fair value. Despite recent insider selling, the firm remains financially sound with more cash than total debt and free cash flow positivity. However, it faced a challenging year with earnings growth dipping by 16.8%, contrasting with the industry average of 6.5%. The company has provided guidance for fiscal year 2026, expecting revenue between A$390 million and A$410 million. With interest payments comfortably covered by profits and high-quality past earnings, Lycopodium presents an intriguing prospect amidst its peers.

- Click to explore a detailed breakdown of our findings in Lycopodium's health report.

Examine Lycopodium's past performance report to understand how it has performed in the past.

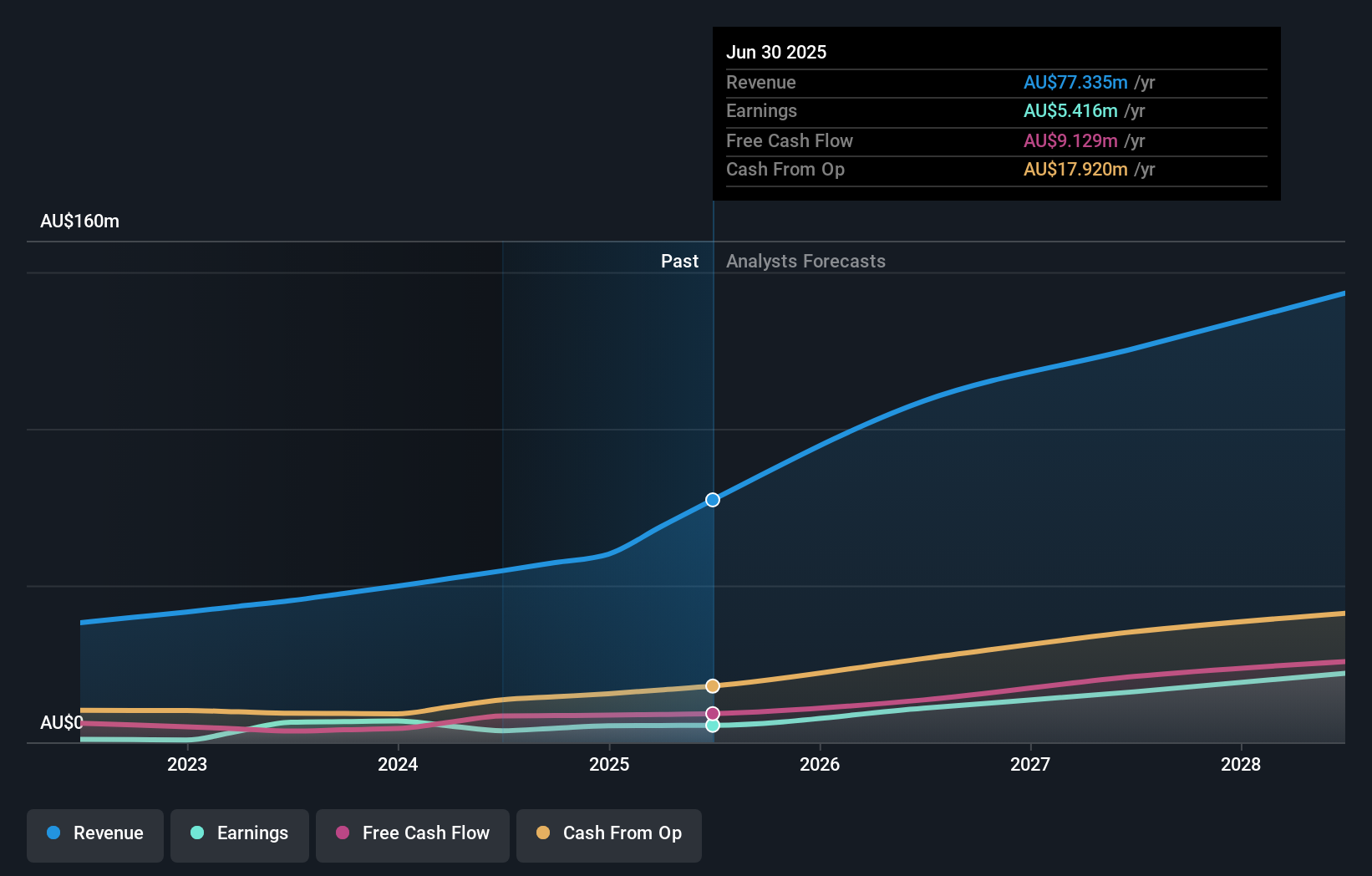

Smart Parking (ASX:SPZ)

Simply Wall St Value Rating: ★★★★★☆

Overview: Smart Parking Limited provides parking management solutions across New Zealand, Australia, Denmark, Germany, and the United Kingdom, with a market capitalization of A$522.67 million.

Operations: Smart Parking Limited generates revenue primarily from its Parking Management operations, with significant contributions from the United Kingdom (A$52.52 million) and the United States (A$10.22 million). The Technology Division also adds to its revenue streams, albeit on a smaller scale (A$5.27 million).

Smart Parking, a nimble player in the parking solutions sector, has seen its earnings grow 46.8% over the past year, outpacing industry averages. The company's debt to equity ratio has slightly increased to 0.9% over five years but remains manageable with interest payments well covered by EBIT at 7.4 times coverage. Trading at a significant discount of 43.5% below estimated fair value, Smart Parking's strategic market expansion into the U.S., Germany, and New Zealand aims to drive revenue growth while mitigating risks associated with geographic concentration and regulatory challenges that could impact profitability amidst evolving urban mobility trends.

Where To Now?

- Investigate our full lineup of 59 ASX Undiscovered Gems With Strong Fundamentals right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com