- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Illumina (ILMN) Valuation Check After MyOme Partnership Fuels Renewed Investor Optimism

Illumina (ILMN) just gave investors a fresh talking point with its new collaboration and investment in MyOme, a move that pushed the stock up as the market reassessed its growth runway.

See our latest analysis for Illumina.

The MyOme deal fits a broader shift in sentiment, with Illumina’s recent collaboration driven gains adding to a strong 90 day share price return of 46.78 percent, even as the five year total shareholder return remains deeply negative and suggests investors are only gradually rebuilding confidence.

If this genomics story has your attention, it is also a good moment to explore other innovative healthcare names using our healthcare stocks and see what else is emerging across the sector.

With Illumina shares rebounding but still sitting on steep five year losses, are investors being offered a rare chance to buy a genomics leader at a discount, or is the market already pricing in the next leg of growth?

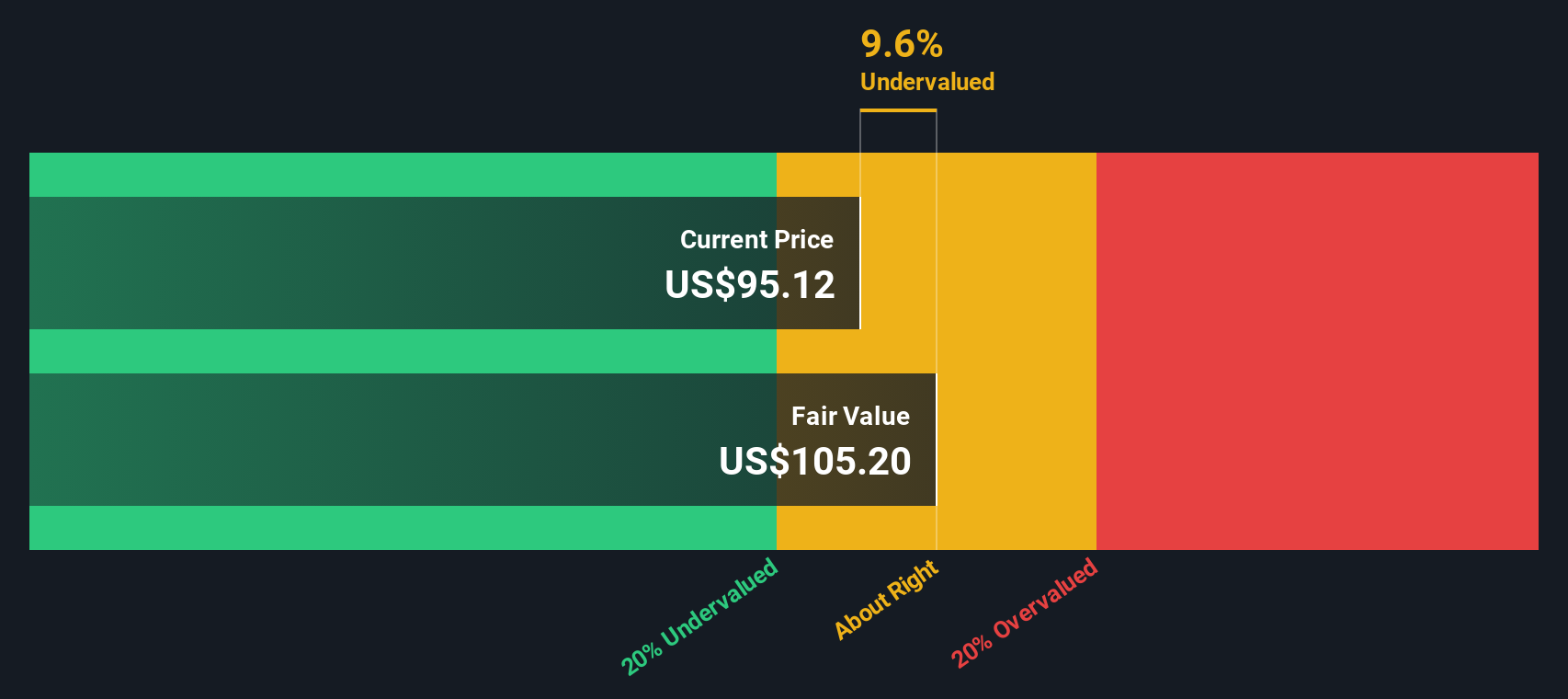

Most Popular Narrative: 12.9% Overvalued

With Illumina closing at $135.32 against a narrative fair value of $119.84, the current price implies a richer outlook than this framework suggests.

Recent research updates reflect a range of opinions on Illumina's valuation and future prospects, with both bullish and bearish analysts weighing in following the company's latest quarterly results.

Bullish analysts increased price targets in response to better than expected quarterly results and signs of effective operational management.

Want to see what justifies paying up for slower revenue growth, thinner margins, and a higher future earnings multiple than today? The narrative spells out the math behind that conviction, including how modest growth, disciplined profitability, and an upgraded valuation multiple are combined using a specific discount rate to land on that fair value.

Result: Fair Value of $119.84 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent China regulatory uncertainty and intensifying competition in high throughput sequencing could derail revenue momentum and challenge the premium valuation that underpins this narrative.

Find out about the key risks to this Illumina narrative.

Another Angle on Valuation

While the narrative fair value suggests Illumina is 12.9 percent overvalued, our SWS DCF model points the other way, with a fair value of $181.17, implying the shares trade at a 25.3 percent discount. Is the market underestimating long term cash generation, or is the model too generous?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Illumina Narrative

If you want to challenge these assumptions, or rely on your own analysis instead of ours, you can build a personalized view in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Illumina.

Ready for more investment ideas?

Do not stop at one compelling story. Use the Simply Wall St Screener to quickly uncover fresh opportunities that fit your strategy before the market catches on.

- Target reliable portfolio income by reviewing these 10 dividend stocks with yields > 3% that may strengthen your cash flow while others overlook these steady payers.

- Capitalize on cutting edge innovation with these 24 AI penny stocks that could reshape entire industries while they are still early in their growth runway.

- Hunt for mispriced opportunities through these 904 undervalued stocks based on cash flows that might be trading below their long term cash flow potential right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com