- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

3 Stocks That Investors Might Be Undervaluing By Up To 32.3%

As the S&P 500 closes at a record high, buoyed by stronger-than-expected economic growth and a tech stock rally, investors are keenly observing which sectors might lead the market next year. Amidst this optimistic environment, identifying undervalued stocks becomes crucial as they may offer potential opportunities for those looking to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Zymeworks (ZYME) | $26.79 | $52.64 | 49.1% |

| UMB Financial (UMBF) | $119.21 | $233.51 | 48.9% |

| Sportradar Group (SRAD) | $23.11 | $45.57 | 49.3% |

| SmartStop Self Storage REIT (SMA) | $31.23 | $61.55 | 49.3% |

| Gold Royalty (GROY) | $4.20 | $8.38 | 49.9% |

| Firefly Aerospace (FLY) | $26.46 | $51.58 | 48.7% |

| Community West Bancshares (CWBC) | $22.64 | $44.11 | 48.7% |

| Columbia Banking System (COLB) | $28.61 | $57.00 | 49.8% |

| Clearfield (CLFD) | $29.63 | $58.38 | 49.2% |

| BioLife Solutions (BLFS) | $25.46 | $49.96 | 49% |

Let's review some notable picks from our screened stocks.

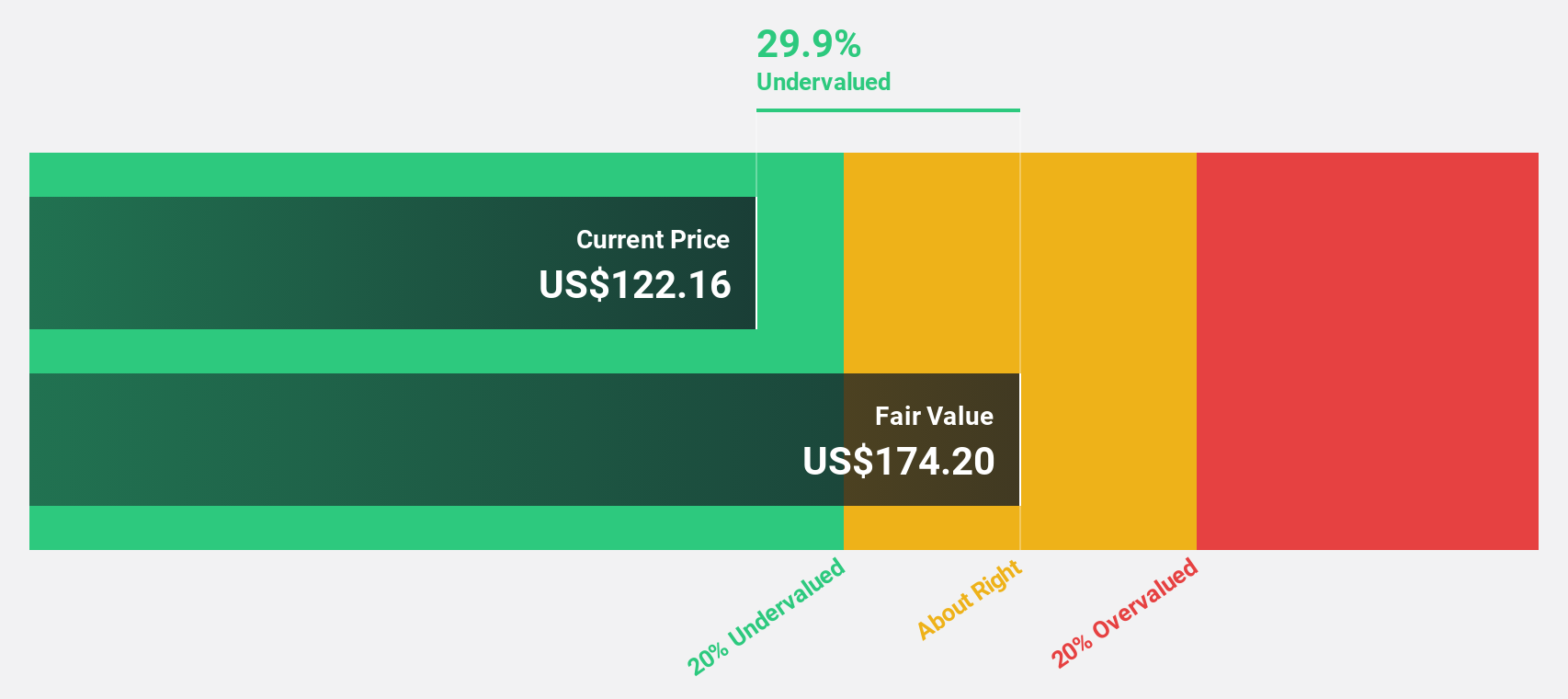

Datadog (DDOG)

Overview: Datadog, Inc. provides an observability and security platform for cloud applications globally, with a market cap of approximately $49.53 billion.

Operations: The company generates revenue primarily from its IT Infrastructure segment, which accounts for $3.21 billion.

Estimated Discount To Fair Value: 32.3%

Datadog is currently trading at US$141.23, significantly below its estimated fair value of US$208.66, suggesting it may be undervalued based on cash flows. Despite a decline in profit margins from 7.6% to 3.3%, Datadog's revenue and earnings are forecast to grow faster than the US market, with earnings expected to rise by over 34% annually. Recent partnerships with Contrast Security and Flywl enhance its security offerings and cloud marketplace visibility, potentially driving future growth.

- The analysis detailed in our Datadog growth report hints at robust future financial performance.

- Get an in-depth perspective on Datadog's balance sheet by reading our health report here.

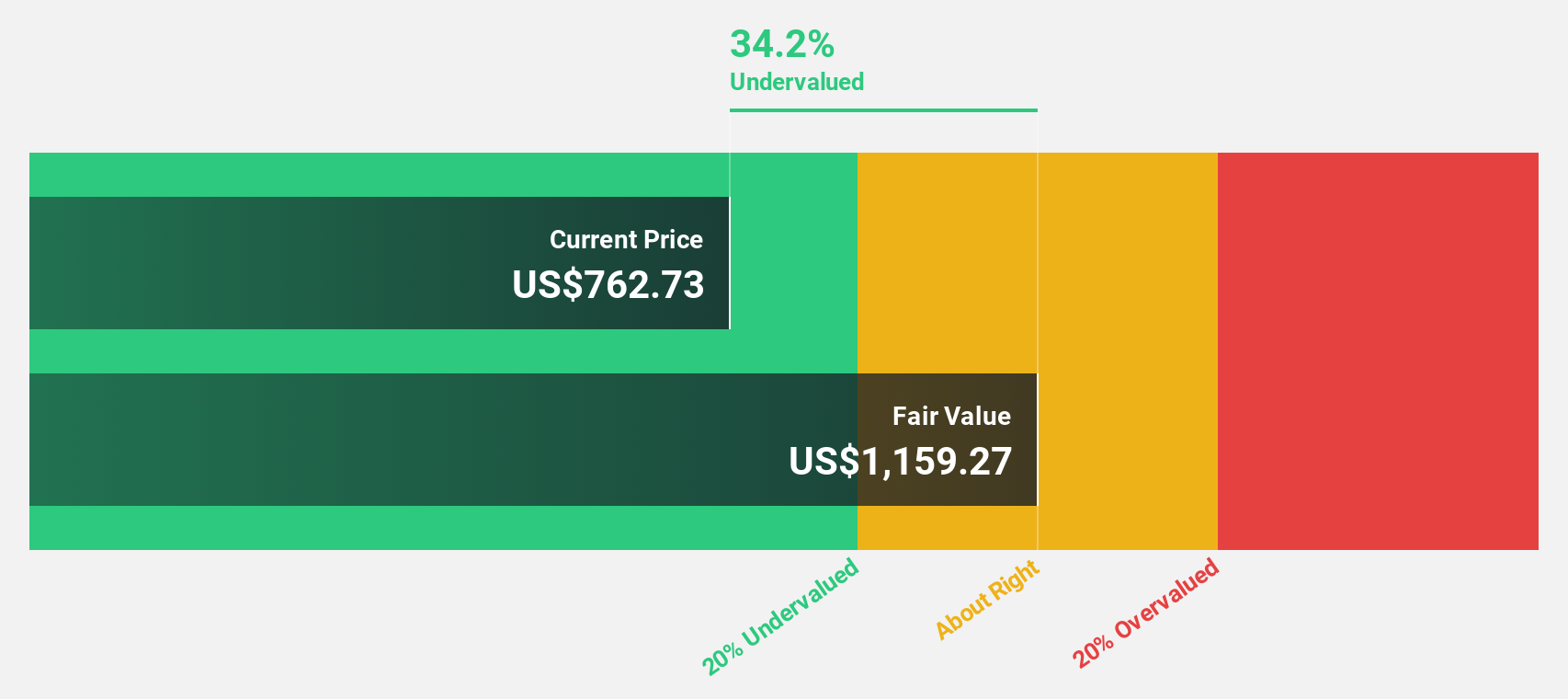

Eli Lilly (LLY)

Overview: Eli Lilly and Company is engaged in the discovery, development, and marketing of human pharmaceuticals across the United States, Europe, China, Japan, and other international markets with a market cap of approximately $963.86 billion.

Operations: Eli Lilly generates revenue of $59.42 billion from the discovery, development, manufacturing, marketing, and sales of pharmaceutical products across various global markets.

Estimated Discount To Fair Value: 15.9%

Eli Lilly is trading at US$1071.64, slightly below its estimated fair value of US$1274.08, indicating potential undervaluation based on cash flows. Despite high debt levels, its earnings are forecast to grow significantly faster than the US market, driven by innovative products like orforglipron for obesity and Inluriyo for breast cancer. Recent positive trial outcomes and FDA submissions highlight robust product development, although legal challenges related to Actos could pose financial risks.

- The growth report we've compiled suggests that Eli Lilly's future prospects could be on the up.

- Click here and access our complete balance sheet health report to understand the dynamics of Eli Lilly.

Vertiv Holdings Co (VRT)

Overview: Vertiv Holdings Co is a company that designs, manufactures, and services critical digital infrastructure technologies for data centers, communication networks, and various industrial environments globally, with a market cap of approximately $63.56 billion.

Operations: The company's revenue is derived from three main segments: $5.82 billion from the Americas, $2.29 billion from the Asia Pacific, and $2.43 billion from Europe, the Middle East, and Africa.

Estimated Discount To Fair Value: 23.4%

Vertiv Holdings Co is trading at US$166.26, below its estimated fair value of US$217.14, suggesting undervaluation based on cash flows. With earnings projected to grow significantly faster than the US market, Vertiv's strategic alliances with Caterpillar and NVIDIA enhance its position in energy solutions and AI infrastructure. Recent dividend increases reflect strong financial performance, though investors should consider potential execution risks associated with rapid expansion and complex project collaborations.

- Insights from our recent growth report point to a promising forecast for Vertiv Holdings Co's business outlook.

- Unlock comprehensive insights into our analysis of Vertiv Holdings Co stock in this financial health report.

Next Steps

- Investigate our full lineup of 210 Undervalued US Stocks Based On Cash Flows right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com