- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Core & Main (CNM): Reassessing Valuation After Strong Q3 Results and Confident Growth Strategy Update

Core & Main (CNM) just checked several key boxes in its latest earnings update, pairing steady third quarter growth with a clear commitment to acquisitions, share buybacks and disciplined capital allocation.

See our latest analysis for Core & Main.

The stock has cooled slightly after the earnings pop, with a 1 month share price return of 18.01% and a 3 year total shareholder return of 181.16%. This suggests momentum is still firmly on Core & Main’s side.

If this kind of steady execution appeals to you, it could be worth exploring fast growing stocks with high insider ownership as a way to uncover other fast moving opportunities with committed owners behind them.

Yet with Core & Main now trading close to analyst targets after a powerful multi year run, are investors still getting a deal on durable compounder style growth, or is the market already pricing in the next leg higher?

Most Popular Narrative Narrative: 9.7% Undervalued

With Core & Main last closing at $53.87 against a most popular narrative fair value of about $59.63, the story points to upside that hinges on specific growth and margin assumptions.

Core & Main anticipates generating strong operating cash flows, enabling further investment in organic growth and M&A, in addition to returning capital to shareholders through share repurchases, positively impacting earnings per share.

Curious how modest top line expansion, rising margins and ongoing buybacks combine into this higher fair value, and what earnings power that implies by the late 2020s? The narrative stitches those moving parts into a single valuation roadmap that might surprise anyone treating Core & Main as just another distributor.

Result: Fair Value of $59.63 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, leadership transitions and higher borrowing costs could squeeze margins and slow execution, which may challenge the bullish case if growth falls short of expectations.

Find out about the key risks to this Core & Main narrative.

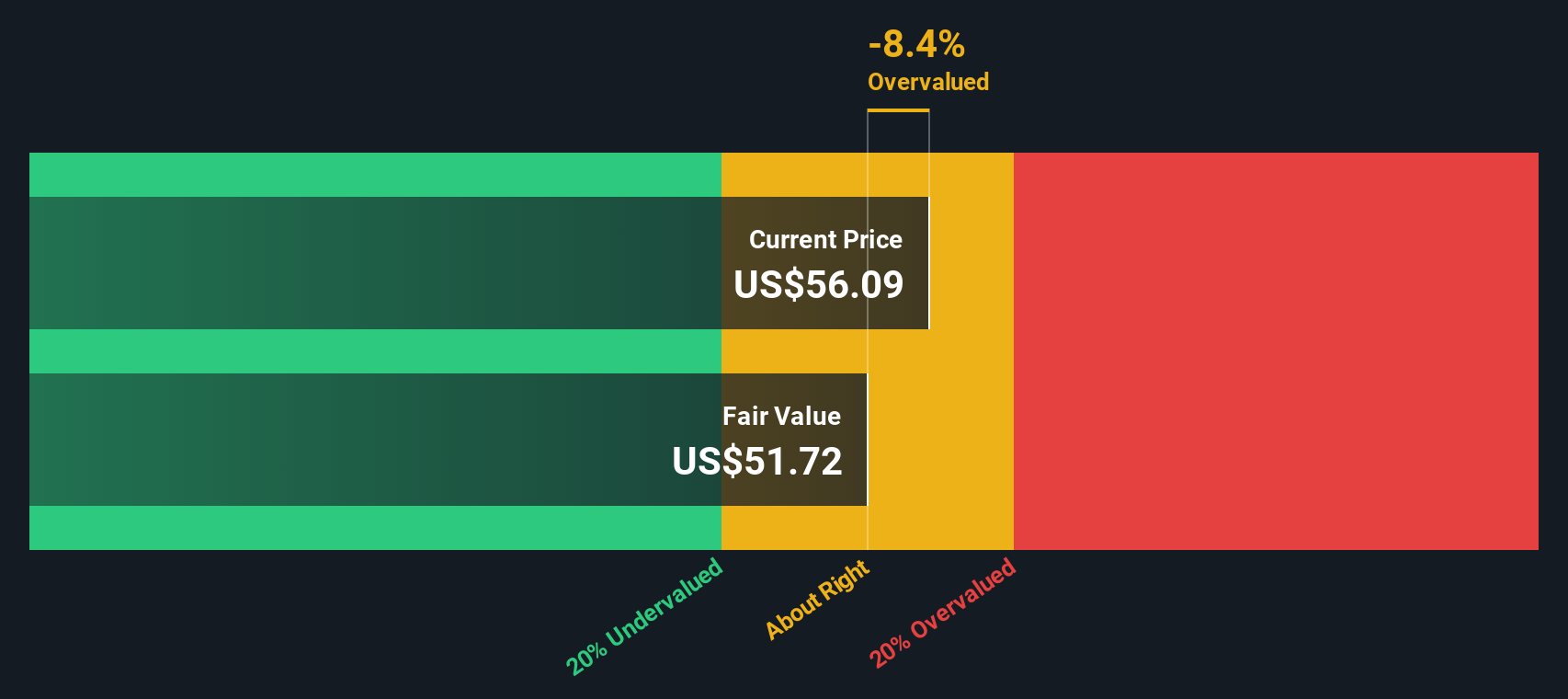

Another Angle on Valuation

While the narrative points to upside, our DCF model actually pegs fair value nearer $51.60, slightly below the current $53.87 share price. That implies Core & Main might already be pricing in a lot of the growth story, leaving less room for error if conditions soften.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Core & Main for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 903 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Core & Main Narrative

If you are not fully convinced by this view or prefer to dig into the numbers yourself, you can build a custom narrative in just a few minutes: Do it your way.

A great starting point for your Core & Main research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you stop here, you could miss standout opportunities. Put Simply Wall Street’s powerful screener to work and upgrade your watchlist with fresh, data backed ideas.

- Capture overlooked upside by targeting these 903 undervalued stocks based on cash flows that strong cash flows suggest the market has not fully recognized yet.

- Capitalize on the AI revolution by zeroing in on these 24 AI penny stocks riding structural tailwinds in automation, data, and intelligent software.

- Boost your income potential by focusing on these 12 dividend stocks with yields > 3% that offer attractive yields while still maintaining solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com