- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Alleged Employee Poaching And Branch Closures Might Change The Case For Investing In Old National Bancorp (ONB)

- Old National Bank has filed a lawsuit against Bell Bank alleging a coordinated mass resignation of eight senior employees from its Brainerd and Baxter, Minnesota branches, along with the misuse of confidential information and customer relationships that disrupted operations and led to branch closures.

- The case highlights how competition for experienced bankers and local client relationships can affect Old National’s regional presence, operational continuity, and customer retention in its Midwest footprint.

- We’ll now examine how this alleged employee poaching and operational disruption could influence Old National Bancorp’s broader investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Old National Bancorp Investment Narrative Recap

To own Old National Bancorp, you need to believe in a Midwest focused regional bank that can keep growing profitably while managing concentrated commercial real estate exposure and a still evolving regulatory backdrop. The Bell Bank lawsuit, while disruptive locally, does not appear to materially alter Old National’s near term earnings drivers, which are more tied to net interest income trends, credit quality, and the successful integration of recent acquisitions.

The current dispute sits against a backdrop of solid net interest income momentum, with Old National’s net interest income having grown 26.2% annually over the past five years and an outlook that points to further market share gains and efficiency improvements. How well the bank protects key client relationships and talent in markets like Minnesota will influence whether it can fully capture the benefits of that earnings engine and maintain its position within its Midwest footprint.

Yet investors should be aware that Old National’s meaningful commercial real estate concentration could interact with events like this in ways that ...

Read the full narrative on Old National Bancorp (it's free!)

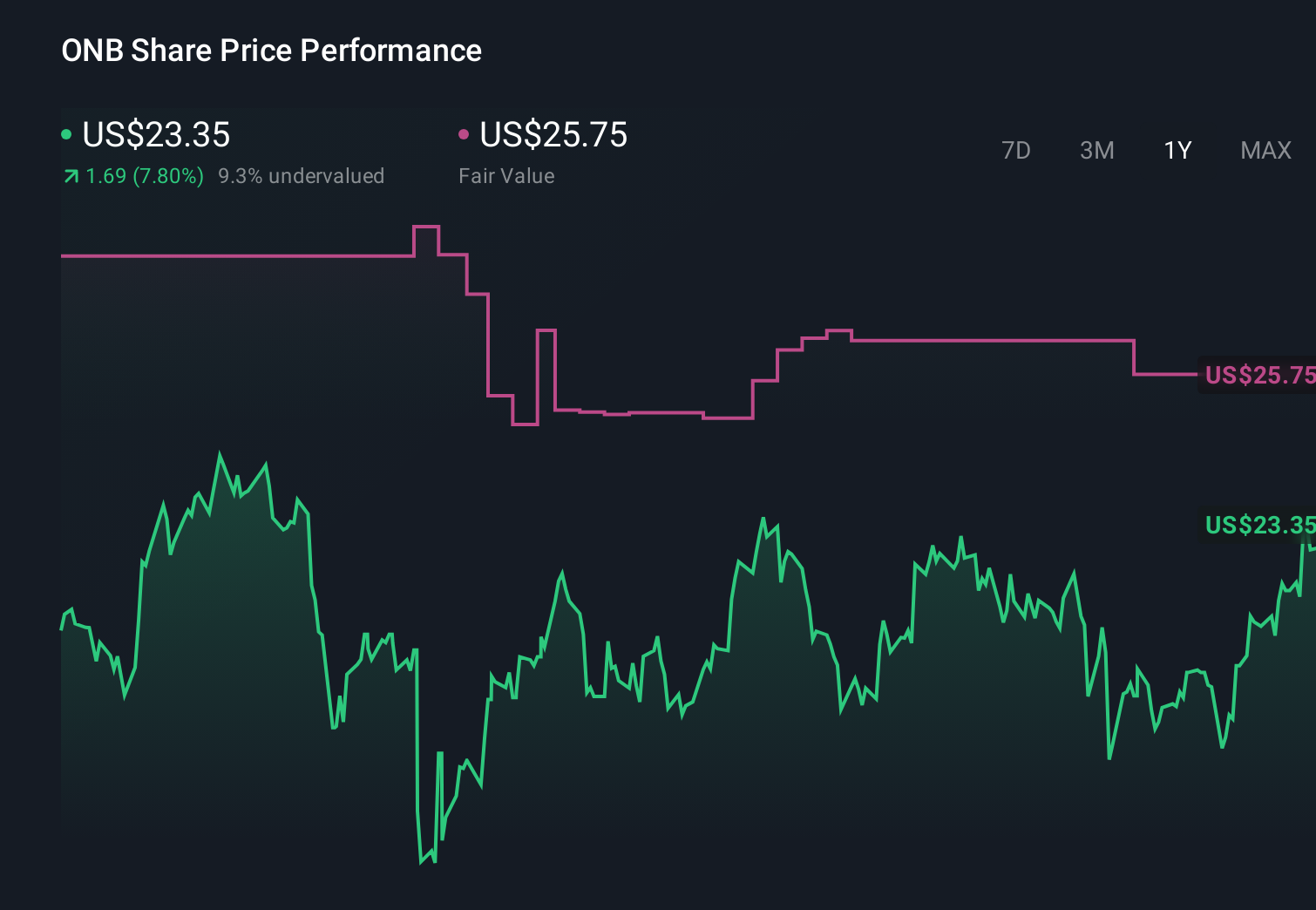

Old National Bancorp's narrative projects $3.6 billion revenue and $1.5 billion earnings by 2028. This requires 24.2% yearly revenue growth and an earnings increase of about $948 million from $551.6 million today.

Uncover how Old National Bancorp's forecasts yield a $25.75 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Old National Bancorp range from US$25.75 up to an extreme US$12,367.80, underscoring just how far apart individual views can be. When you set those opinions against Old National’s reliance on Midwest commercial and CRE lending, it becomes even more important to weigh several different risk focused perspectives before deciding how this stock fits into your portfolio.

Explore 3 other fair value estimates on Old National Bancorp - why the stock might be a potential multi-bagger!

Build Your Own Old National Bancorp Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Old National Bancorp research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Old National Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Old National Bancorp's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com