- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Is Stantec’s Steady Execution Being Fairly Valued Versus Peers (TSX:STN)?

- Recent commentary on Stantec has highlighted that, despite steady operational performance and consistent earnings, the company has faced renewed scrutiny over how its valuation compares with other engineering and infrastructure peers.

- This debate is being fueled by the perception that Stantec’s resilient margins and diversified project backlog may not be fully reflected in current market expectations, even though there have been no major new contracts or corporate announcements in the past week.

- With that in mind, we’ll now examine how this renewed focus on Stantec’s valuation relative to its operational consistency may influence its investment narrative.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Stantec Investment Narrative Recap

To own Stantec, you have to believe in a long-term need for infrastructure renewal, water and environmental services, and a business model that converts that demand into steady earnings. The latest share price weakness versus stable results does not appear to materially change the near term growth catalyst of sustained project demand, but it does sharpen attention on the key risk around valuation stretch if growth or margins were to slow.

The most relevant recent update in this context is Stantec’s guidance raise, with management lifting 2025 net revenue growth expectations to 10% to 12%. That reaffirmation of growth ambitions sits beside concerns about integration risk from acquisitions and the company’s higher Price To Earnings multiple relative to peers, giving investors a clearer contrast between the upside from execution and the downside if integration or macro conditions disappoint.

Yet investors should also be aware that the real pressure point could be if public infrastructure funding were to...

Read the full narrative on Stantec (it's free!)

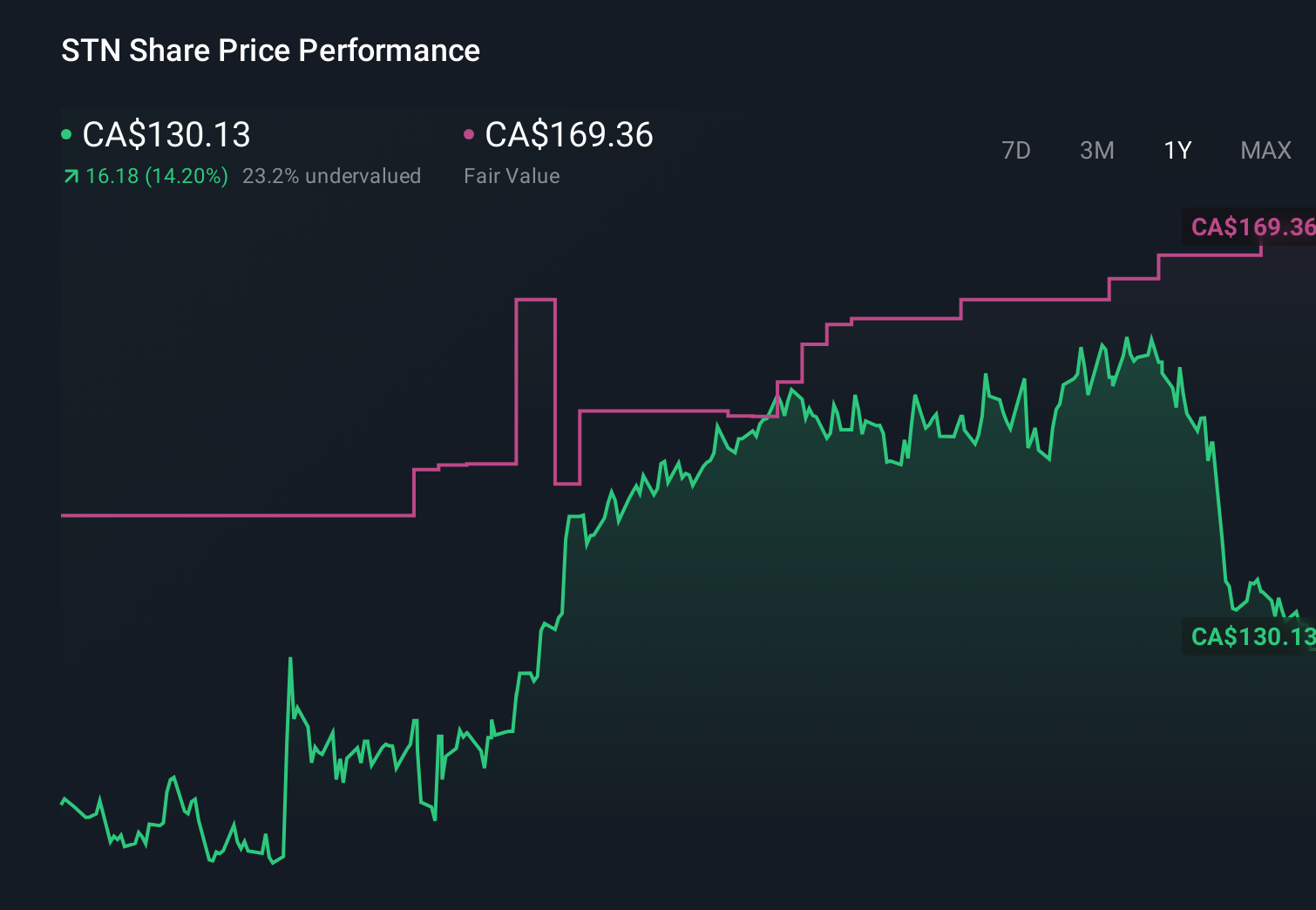

Stantec's narrative projects CA$8.2 billion revenue and CA$785.7 million earnings by 2028. This requires 10.0% yearly revenue growth and a CA$349.0 million earnings increase from CA$436.7 million today.

Uncover how Stantec's forecasts yield a CA$169.36 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community currently place Stantec’s fair value between CA$118.03 and CA$169.36, underscoring how far opinions can spread. Against that backdrop, reliance on sustained public infrastructure funding becomes a central issue for the company’s future performance and is worth assessing through several independent viewpoints.

Explore 6 other fair value estimates on Stantec - why the stock might be worth 9% less than the current price!

Build Your Own Stantec Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Stantec research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Stantec research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Stantec's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com