- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Astera Labs (ALAB): Assessing Valuation After Morgan Stanley’s AI and Data Center Endorsement

Morgan Stanley just spotlighted Astera Labs (ALAB) as one of its top semiconductor picks for 2026, grouping it with Nvidia and Broadcom on the strength of AI and data center demand.

See our latest analysis for Astera Labs.

The endorsement appears to be resonating with investors, with Astera Labs' share price rising to $164.40 and delivering a 1 day share price return of 12.70 percent and a year to date share price return of 22.11 percent. The 1 year total shareholder return of 24.39 percent suggests that momentum is recovering after a more challenging recent 90 day share price return of negative 32.95 percent.

If you are watching how AI infrastructure names are repricing risk and growth, it could be a good moment to explore other high growth tech and AI stocks that are catching market attention.

Yet with revenue still growing near 30 percent annually and the stock trading almost 20 percent below the average analyst target, investors now face a key question: is this a genuine entry point, or is future growth already priced in?

Most Popular Narrative Narrative: 17.5% Undervalued

With the most followed narrative placing Astera Labs' fair value above the recent 164.40 dollar close, the implied upside rests on aggressive AI infrastructure expansion.

Strong early engagement with hyperscalers and AI platform providers on open, interoperable standards like UALink (which are still in the early adoption phase with projected ramp in 2027 and beyond) enables Astera Labs to capture the industry's shift toward open, multi-vendor AI Infrastructure 2.0. This ensures exposure to significant long-term market expansion and incrementally larger addressable markets, positively impacting revenue growth rates and future margin potential as adoption accelerates.

Curious what kind of revenue surge, margin lift and earnings multiple need to line up to justify that valuation gap, and how long the narrative thinks it can last?

Result: Fair Value of $199.37 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upside case could unravel if hyperscaler AI capex slows or competitors integrate connectivity in house, eroding Astera Labs' product differentiation.

Find out about the key risks to this Astera Labs narrative.

Another Angle on Valuation

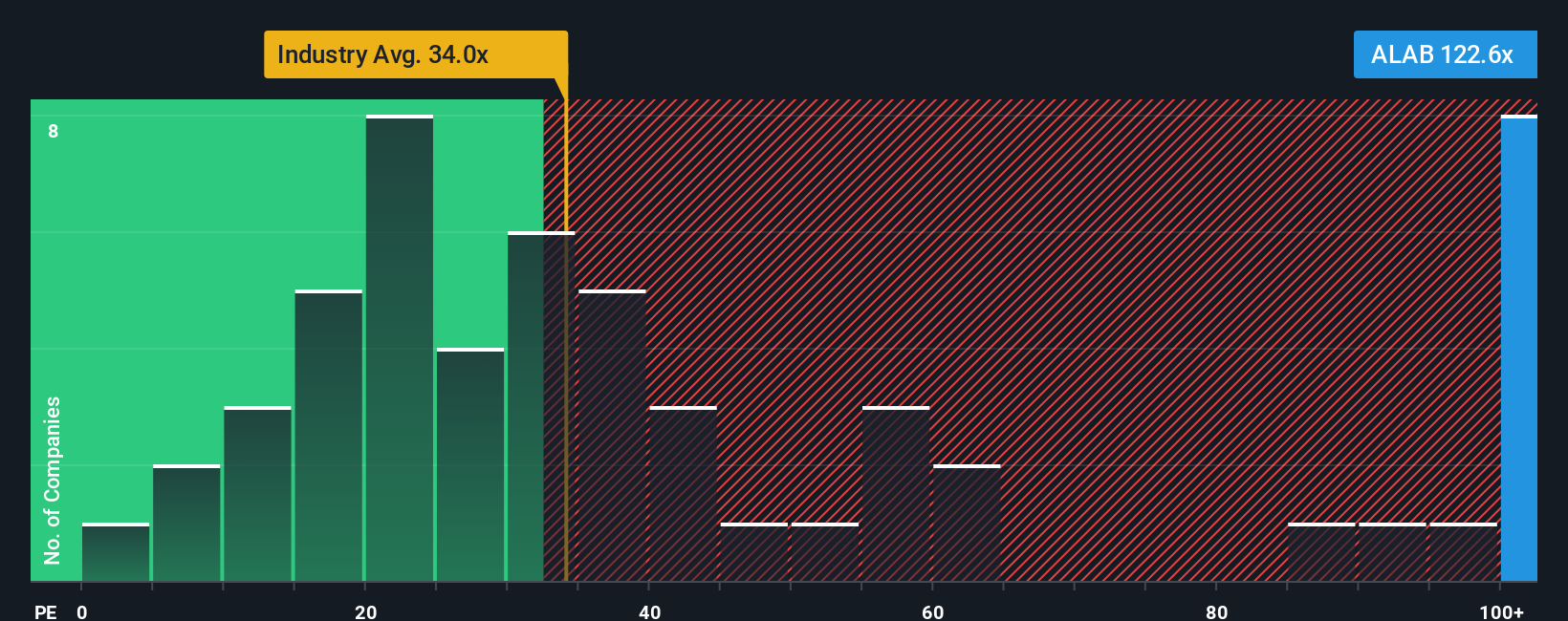

While the narrative model sees Astera Labs as about 17.5 percent undervalued, its current price to earnings ratio of 139.6 times sits far above the US semiconductor average of 36.8 times, the peer average of 60.4 times, and even our fair ratio of 67.3 times. This raises the risk that sentiment rather than fundamentals is doing the heavy lifting. Which lens do you trust when growth eventually cools?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Astera Labs Narrative

If you see the story differently or want to test your own assumptions against the numbers, you can build a personalized narrative in minutes: Do it your way.

A great starting point for your Astera Labs research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before the market prices in the next wave of winners, use the Simply Wall St Screener to spot fresh opportunities that match your strategy and risk profile.

- Capture early-stage upside by targeting under-the-radar names with strong balance sheets and momentum using these 3626 penny stocks with strong financials.

- Position yourself at the heart of the AI boom by filtering for focused innovators through these 24 AI penny stocks.

- Lock in potential mispricings by zeroing in on companies trading below intrinsic value via these 913 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com