- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Should Assurant’s (AIZ) Earnings Beat and New Device Partnerships Require Action From Investors?

- Assurant recently reported quarterly results that exceeded earnings and revenue expectations, while expanding its mobile device protection and extended service contract programs through new financial services partnerships.

- This combination of consistent earnings outperformance and broader protection offerings across connected devices, homes, and automobiles has reinforced confidence in Assurant’s business model resilience.

- We’ll now explore how this continued earnings outperformance, alongside stronger analyst sentiment, reshapes Assurant’s investment narrative for long-term investors.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Assurant Investment Narrative Recap

To own Assurant, you need to believe its protection services across devices, homes, and autos can keep growing despite regulatory and competitive pressures. The latest earnings beat and new financial services partnerships support the near term catalyst of Lifestyle segment expansion, while the biggest ongoing risk remains regulatory scrutiny and pricing pressure in lender placed insurance, which this news does not materially change.

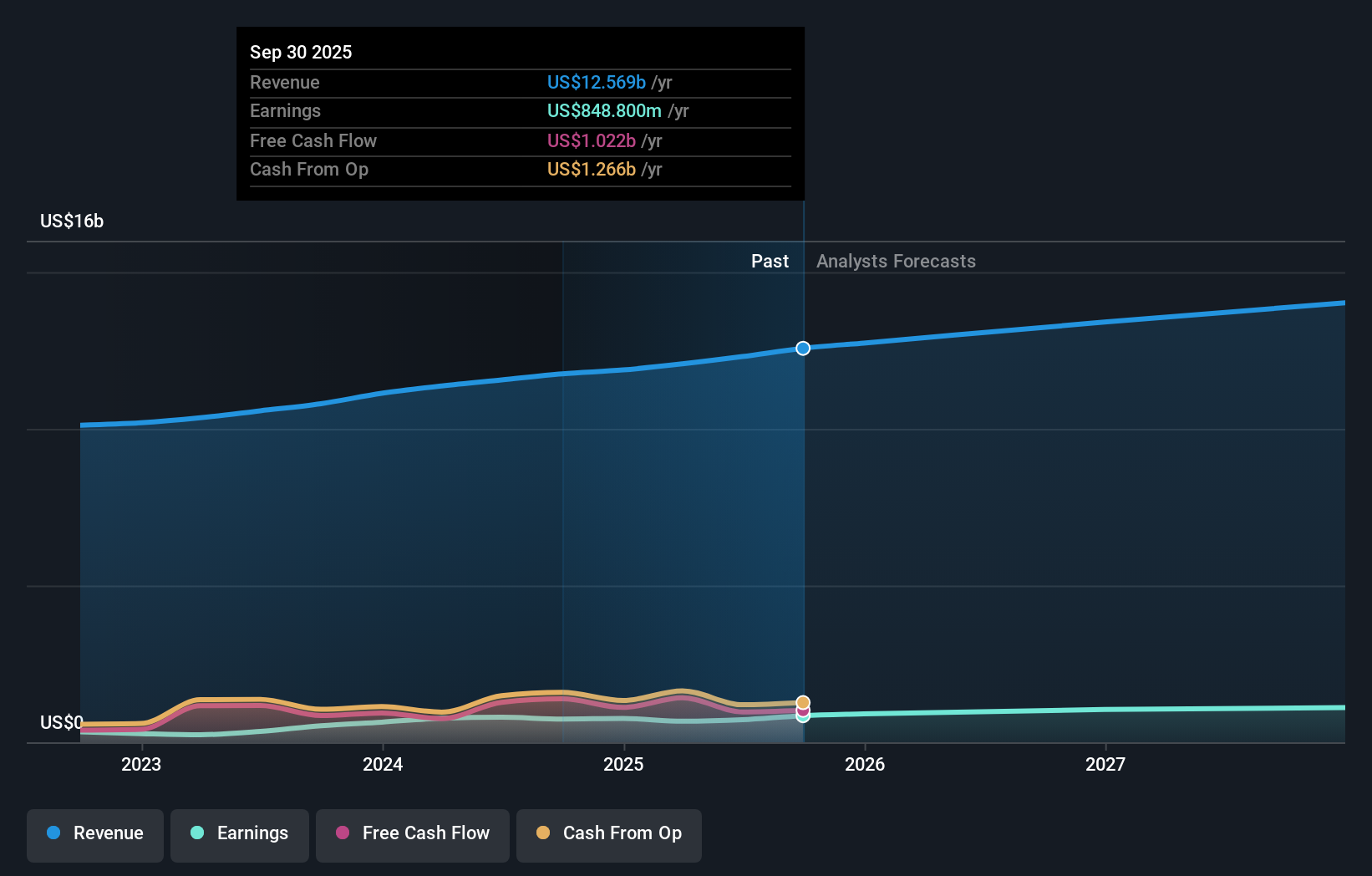

The most relevant recent development here is Assurant’s steady earnings outperformance, with the company topping expectations in each of the last four quarters. That pattern, alongside multiple analysts lifting price targets and maintaining positive ratings, ties directly into the current bullish sentiment catalyst around its Lifestyle and Housing businesses and helps explain why the stock has been testing new 52 week highs.

Yet against this backdrop of strong results, investors should still be aware of the mounting risk that tighter rules around lender placed insurance could...

Read the full narrative on Assurant (it's free!)

Assurant's narrative projects $14.2 billion revenue and $1.2 billion earnings by 2028. This requires 4.9% yearly revenue growth and about a $483 million earnings increase from $717.0 million today.

Uncover how Assurant's forecasts yield a $253.67 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Four Simply Wall St Community fair value estimates for Assurant span from about US$185 to more than US$320,700, underscoring how widely opinions can differ. Readers can weigh these views against the company’s reliance on lender placed insurance, where any regulatory shift could influence profitability and growth.

Explore 4 other fair value estimates on Assurant - why the stock might be a potential multi-bagger!

Build Your Own Assurant Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Assurant research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Assurant research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Assurant's overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com