- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Here's Why Asian Granito India (NSE:ASIANTILES) Can Manage Its Debt Responsibly

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Asian Granito India Limited (NSE:ASIANTILES) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

What Is Asian Granito India's Net Debt?

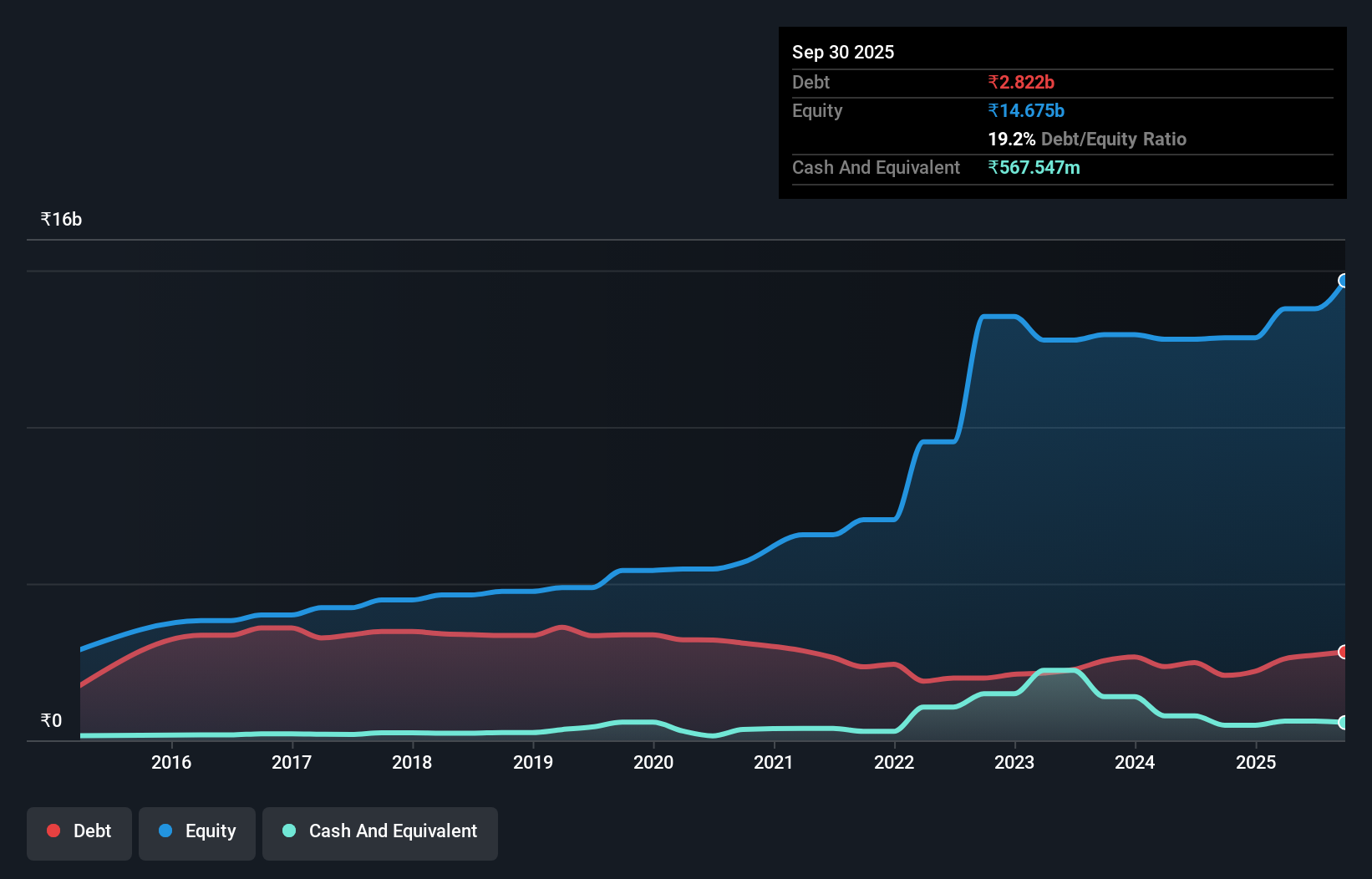

You can click the graphic below for the historical numbers, but it shows that as of September 2025 Asian Granito India had ₹2.82b of debt, an increase on ₹2.07b, over one year. On the flip side, it has ₹567.5m in cash leading to net debt of about ₹2.25b.

How Strong Is Asian Granito India's Balance Sheet?

The latest balance sheet data shows that Asian Granito India had liabilities of ₹6.97b due within a year, and liabilities of ₹1.24b falling due after that. Offsetting these obligations, it had cash of ₹567.5m as well as receivables valued at ₹5.92b due within 12 months. So its liabilities total ₹1.72b more than the combination of its cash and short-term receivables.

Since publicly traded Asian Granito India shares are worth a total of ₹16.7b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

View our latest analysis for Asian Granito India

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Asian Granito India's net debt is sitting at a very reasonable 2.3 times its EBITDA, while its EBIT covered its interest expense just 2.7 times last year. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. Notably, Asian Granito India's EBIT launched higher than Elon Musk, gaining a whopping 4,367% on last year. When analysing debt levels, the balance sheet is the obvious place to start. But it is Asian Granito India's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last two years, Asian Granito India saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Asian Granito India's conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered were considerably better. There's no doubt that its ability to to grow its EBIT is pretty flash. When we consider all the factors mentioned above, we do feel a bit cautious about Asian Granito India's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for Asian Granito India you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.