- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Does Geely Still Offer Value After Recent Volatility in China’s EV Market?

- Wondering if Geely Automobile Holdings is actually good value at today’s price, or if the market has already driven off with the easy gains? This breakdown is designed to give you a clear, no-jargon answer.

- Despite a choppy ride in the short term, with the share price down 6.3% over the last week and 3.7% over the last month, the stock is still up 17.6% year to date and 7.6% over the last year. It has delivered 52.9% over three years but lost 23.0% across five years.

- Recent headlines around competition in the Chinese EV space, shifting export strategies and evolving government support for domestic automakers have all added extra noise to Geely’s share price. At the same time, investor attention on partnerships in electric and hybrid vehicles, plus the company’s international expansion ambitions, has sharpened the focus on what a fair long-term value might look like.

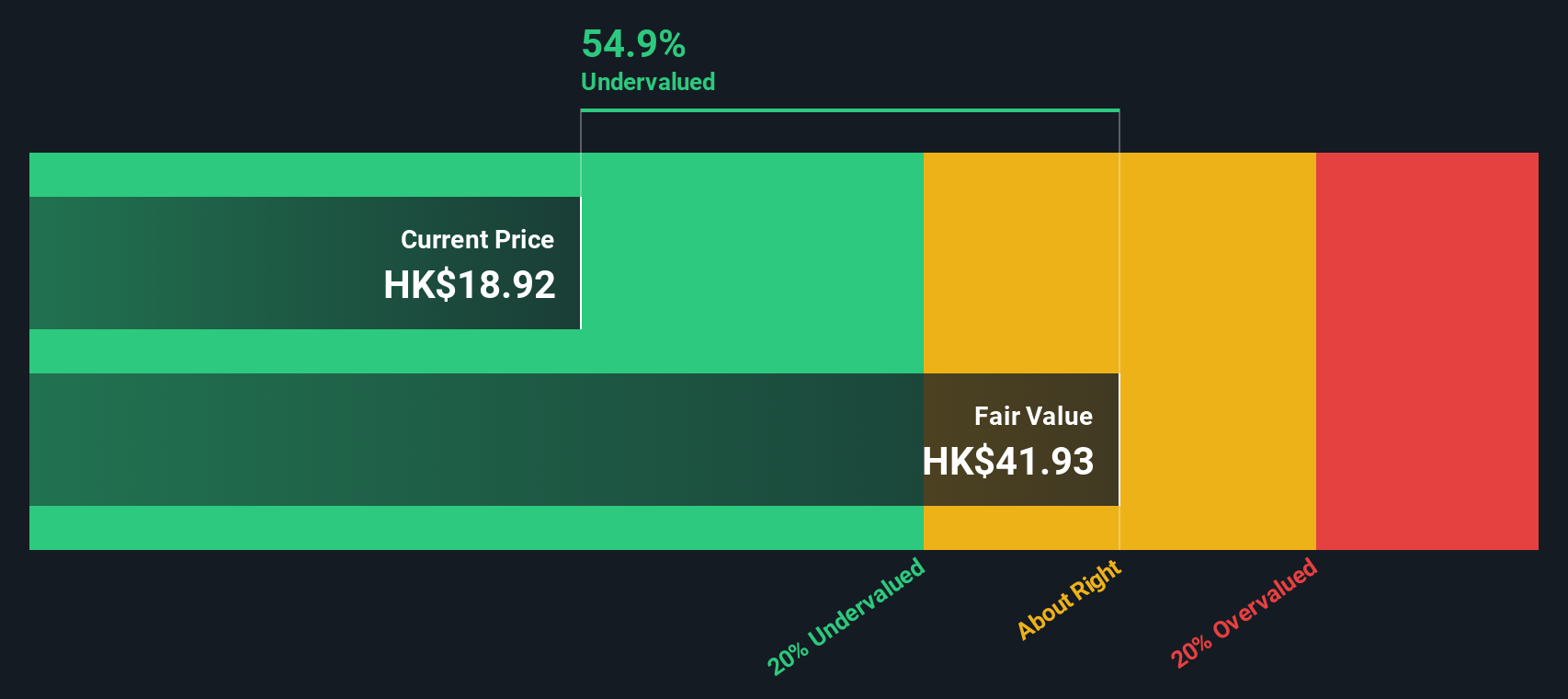

- On our checks, Geely scores a solid 5 out of 6 for valuation. This suggests the market may still be underestimating parts of the story. Next, we will walk through the main valuation approaches before finishing with a more holistic way to think about what the stock is really worth.

Find out why Geely Automobile Holdings's 7.6% return over the last year is lagging behind its peers.

Approach 1: Geely Automobile Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today. For Geely Automobile Holdings, this uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections.

Geely generated trailing twelve month free cash flow of about CN¥5.9 billion. Analysts provide detailed forecasts for the next few years, and Simply Wall St then extrapolates those out, with projected free cash flow rising to roughly CN¥45.1 billion by 2035. These growing cash flows are discounted back and summed to estimate what the entire stream is worth in today’s money.

On this basis, the model arrives at an intrinsic value of around HK$46.04 per share. Compared to the current market price, the DCF implies the stock is about 64.0% undervalued, indicating that investors may be placing a steep discount on Geely’s future cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Geely Automobile Holdings is undervalued by 64.0%. Track this in your watchlist or portfolio, or discover 913 more undervalued stocks based on cash flows.

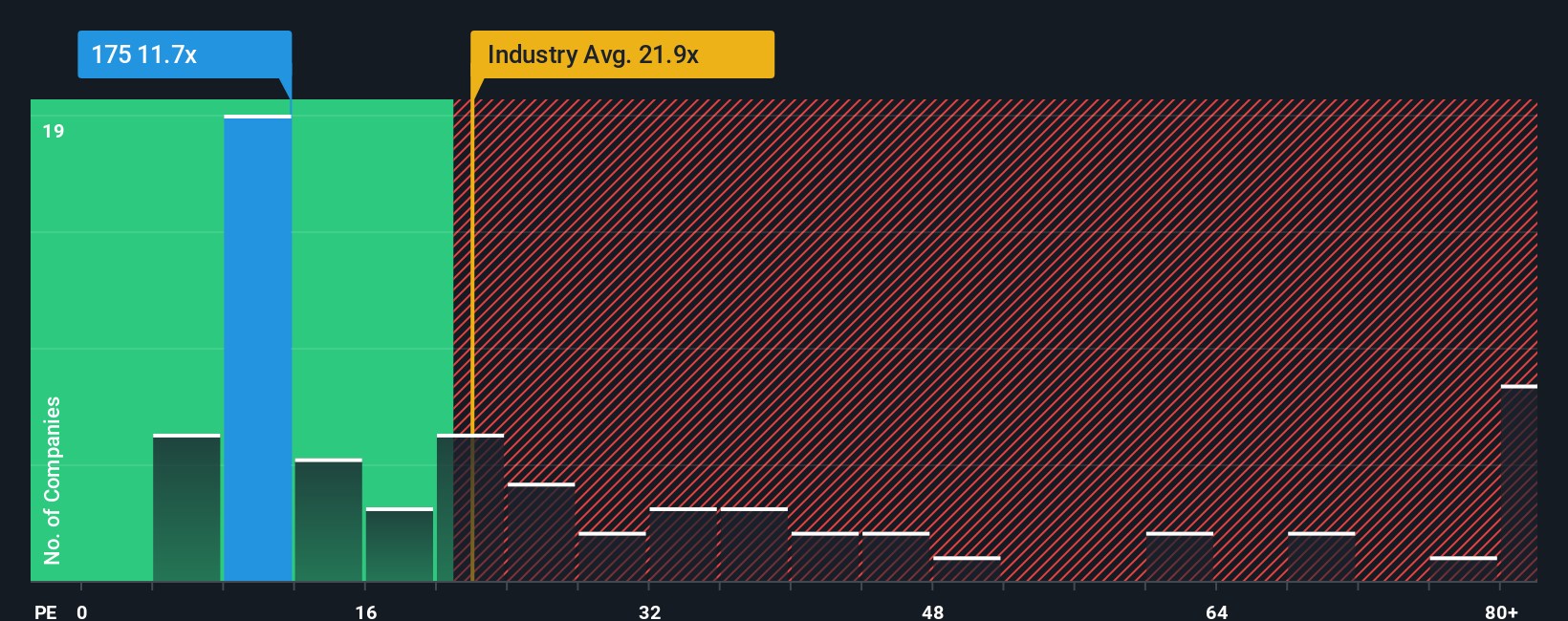

Approach 2: Geely Automobile Holdings Price vs Earnings

For a profitable business like Geely, the price to earnings ratio is a useful yardstick because it links what investors pay today to the profits the company is generating right now. In general, faster growing and lower risk businesses can justify a higher PE ratio, while slower growth or higher uncertainty typically deserves a lower multiple.

Geely currently trades at about 9.26x earnings. That sits below both the wider Auto industry average of roughly 18.38x and the peer group average of around 11.43x, suggesting the market is pricing Geely more cautiously than many of its competitors. To refine this view, Simply Wall St uses a proprietary Fair Ratio, which estimates what PE multiple would make sense for Geely given its earnings growth outlook, margins, industry positioning, market cap and specific risks. For Geely, this Fair Ratio is 12.35x.

Because the Fair Ratio blends company specific fundamentals with sector context, it is a more tailored benchmark than a simple comparison with peers or the industry. Versus this 12.35x Fair Ratio, Geely trading at 9.26x points to the shares still being undervalued on an earnings basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1462 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Geely Automobile Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply the stories investors tell about a company, backed by their own view of fair value and assumptions for future revenue, earnings and margins. A Narrative connects three things: what you believe about the business, how that belief translates into a financial forecast, and what price you think is fair for the stock today. On Simply Wall St, Narratives are an easy, interactive tool on the Community page, used by millions of investors to turn their views into numbers, then compare Fair Value to the current share price to decide whether to buy, hold or sell. As new information arrives, such as earnings, news or major announcements, Narratives can be updated in minutes so your fair value always reflects your latest thinking. For Geely Automobile Holdings, for example, one Narrative might lean bullish and land near the HK$42.17 high target, while another more cautious Narrative could sit closer to the HK$20.07 low target. Both can be explored, challenged and refined side by side.

Do you think there's more to the story for Geely Automobile Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com