- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

NRB Inc.'s (KOSDAQ:475230) most bullish insider, CEO Keon Woo Kang must be pleased with the recent 14% gain

Key Insights

- Significant insider control over NRB implies vested interests in company growth

- A total of 3 investors have a majority stake in the company with 52% ownership

- Ownership research, combined with past performance data can help provide a good understanding of opportunities in a stock

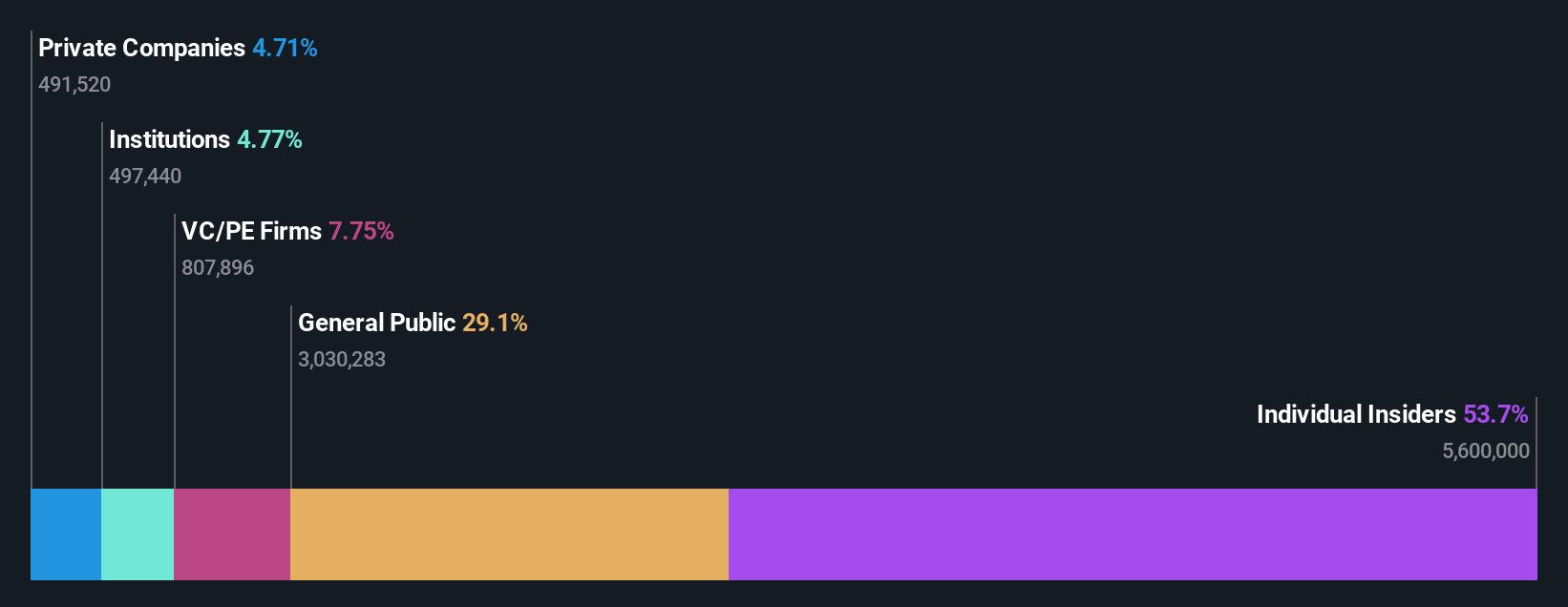

A look at the shareholders of NRB Inc. (KOSDAQ:475230) can tell us which group is most powerful. The group holding the most number of shares in the company, around 54% to be precise, is individual insiders. Put another way, the group faces the maximum upside potential (or downside risk).

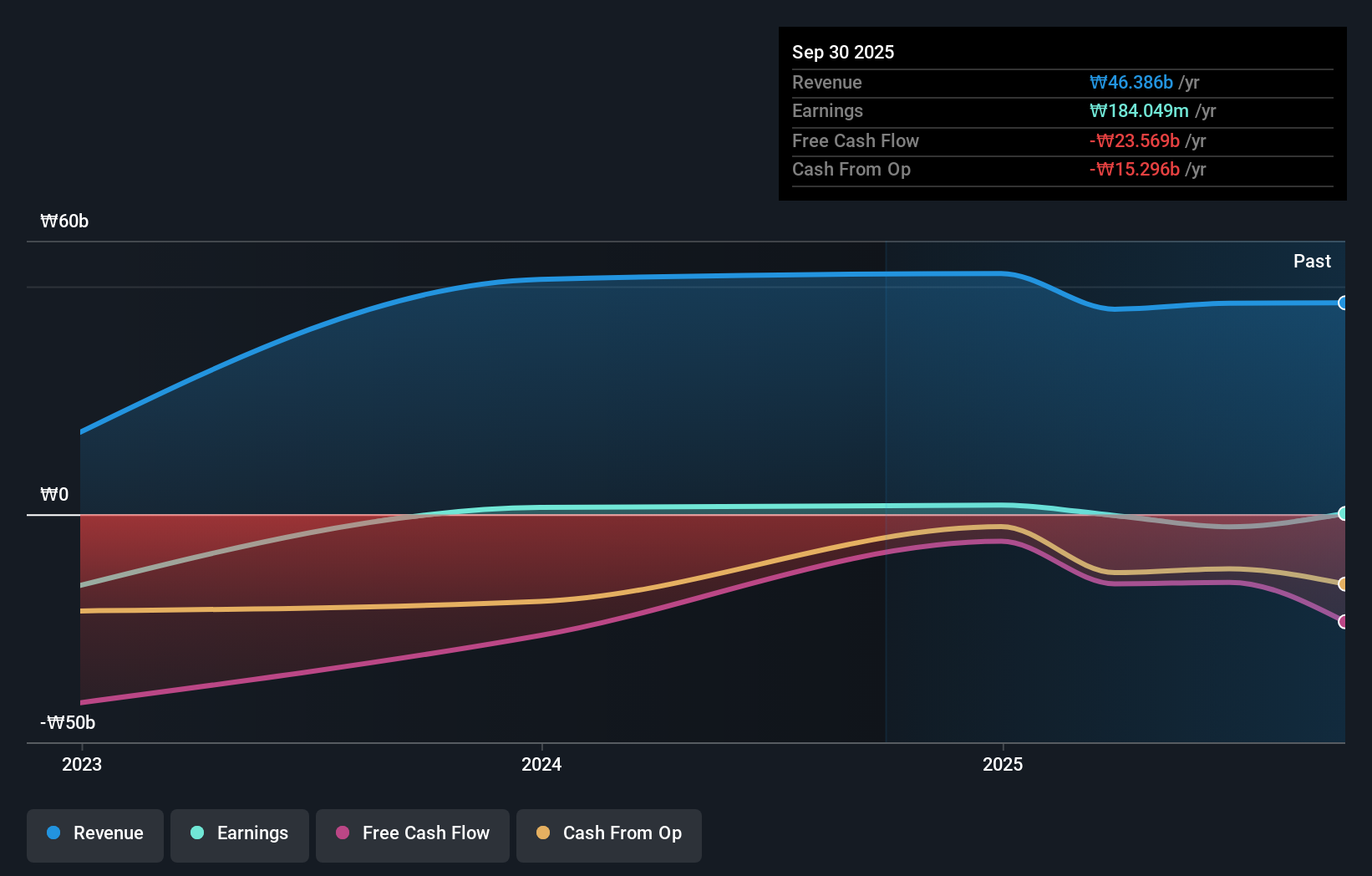

Clearly, insiders benefitted the most after the company's market cap rose by ₩19b last week.

Let's take a closer look to see what the different types of shareholders can tell us about NRB.

Check out our latest analysis for NRB

What Does The Institutional Ownership Tell Us About NRB?

Many institutions measure their performance against an index that approximates the local market. So they usually pay more attention to companies that are included in major indices.

Since institutions own only a small portion of NRB, many may not have spent much time considering the stock. But it's clear that some have; and they liked it enough to buy in. If the company is growing earnings, that may indicate that it is just beginning to catch the attention of these deep-pocketed investors. When multiple institutional investors want to buy shares, we often see a rising share price. The past revenue trajectory (shown below) can be an indication of future growth, but there are no guarantees.

NRB is not owned by hedge funds. Looking at our data, we can see that the largest shareholder is the CEO Keon Woo Kang with 33% of shares outstanding. Meanwhile, the second and third largest shareholders, hold 11% and 7.7%, of the shares outstanding, respectively. Interestingly, the second-largest shareholder, Dong-Woo KIm is also Senior Key Executive, again, pointing towards strong insider ownership amongst the company's top shareholders.

A more detailed study of the shareholder registry showed us that 3 of the top shareholders have a considerable amount of ownership in the company, via their 52% stake.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock's expected performance. As far as we can tell there isn't analyst coverage of the company, so it is probably flying under the radar.

Insider Ownership Of NRB

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

Our most recent data indicates that insiders own the majority of NRB Inc.. This means they can collectively make decisions for the company. Given it has a market cap of ₩159b, that means they have ₩86b worth of shares. It is good to see this level of investment. You can check here to see if those insiders have been buying recently.

General Public Ownership

With a 29% ownership, the general public, mostly comprising of individual investors, have some degree of sway over NRB. This size of ownership, while considerable, may not be enough to change company policy if the decision is not in sync with other large shareholders.

Private Equity Ownership

With an ownership of 7.7%, private equity firms are in a position to play a role in shaping corporate strategy with a focus on value creation. Some investors might be encouraged by this, since private equity are sometimes able to encourage strategies that help the market see the value in the company. Alternatively, those holders might be exiting the investment after taking it public.

Private Company Ownership

It seems that Private Companies own 4.7%, of the NRB stock. It's hard to draw any conclusions from this fact alone, so its worth looking into who owns those private companies. Sometimes insiders or other related parties have an interest in shares in a public company through a separate private company.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. Be aware that NRB is showing 3 warning signs in our investment analysis , and 2 of those are potentially serious...

Of course this may not be the best stock to buy. So take a peek at this free free list of interesting companies.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.