- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Is Now The Time To Put Limbach Holdings (NASDAQ:LMB) On Your Watchlist?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Limbach Holdings (NASDAQ:LMB). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Limbach Holdings with the means to add long-term value to shareholders.

Limbach Holdings' Improving Profits

In the last three years Limbach Holdings' earnings per share took off; so much so that it's a bit disingenuous to use these figures to try and deduce long term estimates. So it would be better to isolate the growth rate over the last year for our analysis. To the delight of shareholders, Limbach Holdings' EPS soared from US$2.35 to US$3.15, over the last year. That's a commendable gain of 34%.

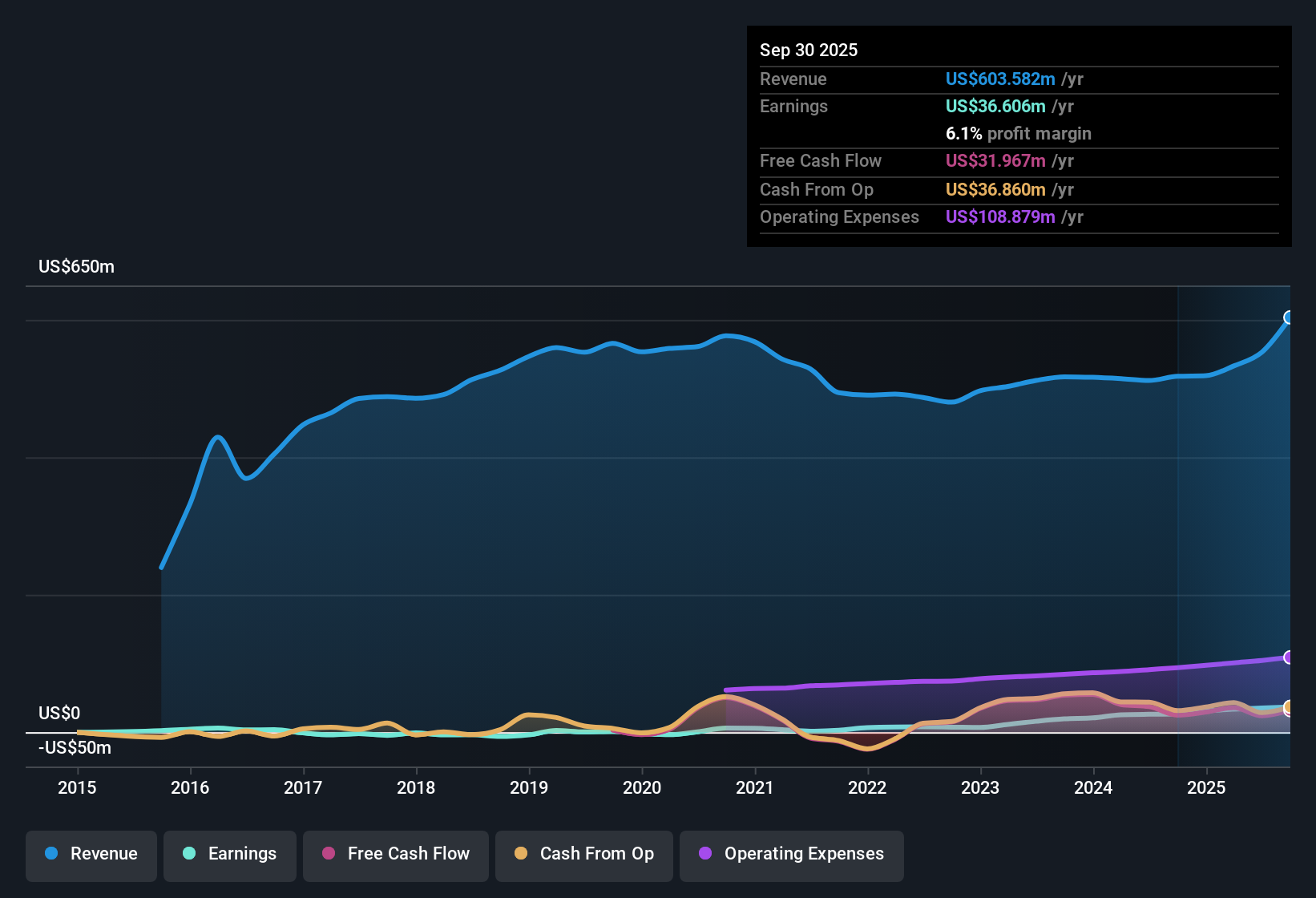

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. EBIT margins for Limbach Holdings remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 17% to US$604m. That's progress.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

Check out our latest analysis for Limbach Holdings

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Limbach Holdings' forecast profits?

Are Limbach Holdings Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

With strong conviction, Limbach Holdings insiders have stood united by refusing to sell shares over the last year. But more importantly, Independent Director David Gaboury spent US$148k acquiring shares, doing so at an average price of US$106. Purchases like this clue us in to the to the faith management has in the business' future.

On top of the insider buying, it's good to see that Limbach Holdings insiders have a valuable investment in the business. Given insiders own a significant chunk of shares, currently valued at US$58m, they have plenty of motivation to push the business to succeed. That's certainly enough to let shareholders know that management will be very focussed on long term growth.

While insiders are apparently happy to hold and accumulate shares, that is just part of the big picture. That's because on our analysis the CEO, Mike McCann, is paid less than the median for similar sized companies. The median total compensation for CEOs of companies similar in size to Limbach Holdings, with market caps between US$400m and US$1.6b, is around US$3.5m.

Limbach Holdings' CEO took home a total compensation package worth US$2.8m in the year leading up to December 2024. That is actually below the median for CEO's of similarly sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of good governance, more generally.

Is Limbach Holdings Worth Keeping An Eye On?

You can't deny that Limbach Holdings has grown its earnings per share at a very impressive rate. That's attractive. On top of that, insiders own a significant piece of the pie when it comes to the company's stock, and one has been buying more. Astute investors will want to keep this stock on watch. Of course, just because Limbach Holdings is growing does not mean it is undervalued. If you're wondering about the valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Limbach Holdings, you'll probably love this curated collection of companies in the US that have an attractive valuation alongside insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.