- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Is It Too Late To Consider KKR After Its Strong Multi Year Share Price Run?

- If you are wondering whether KKR is still a smart buy at today’s price, or if the easy money has already been made, this breakdown will help you size up the opportunity with a valuation lens.

- After an impressive long term climb, with the stock up about 200% over 3 years and 255% over 5 years, recent moves have been choppier, including a 12.4% rise over the last month but a 13.2% drop over the past year.

- Some of the recent share price action has come as investors digest KKR’s growing role in private credit and infrastructure, along with its higher profile deals in areas like insurance and alternative assets. Those shifts can change how the market thinks about KKR’s growth runway and risk profile, even when headline numbers do not move in a straight line.

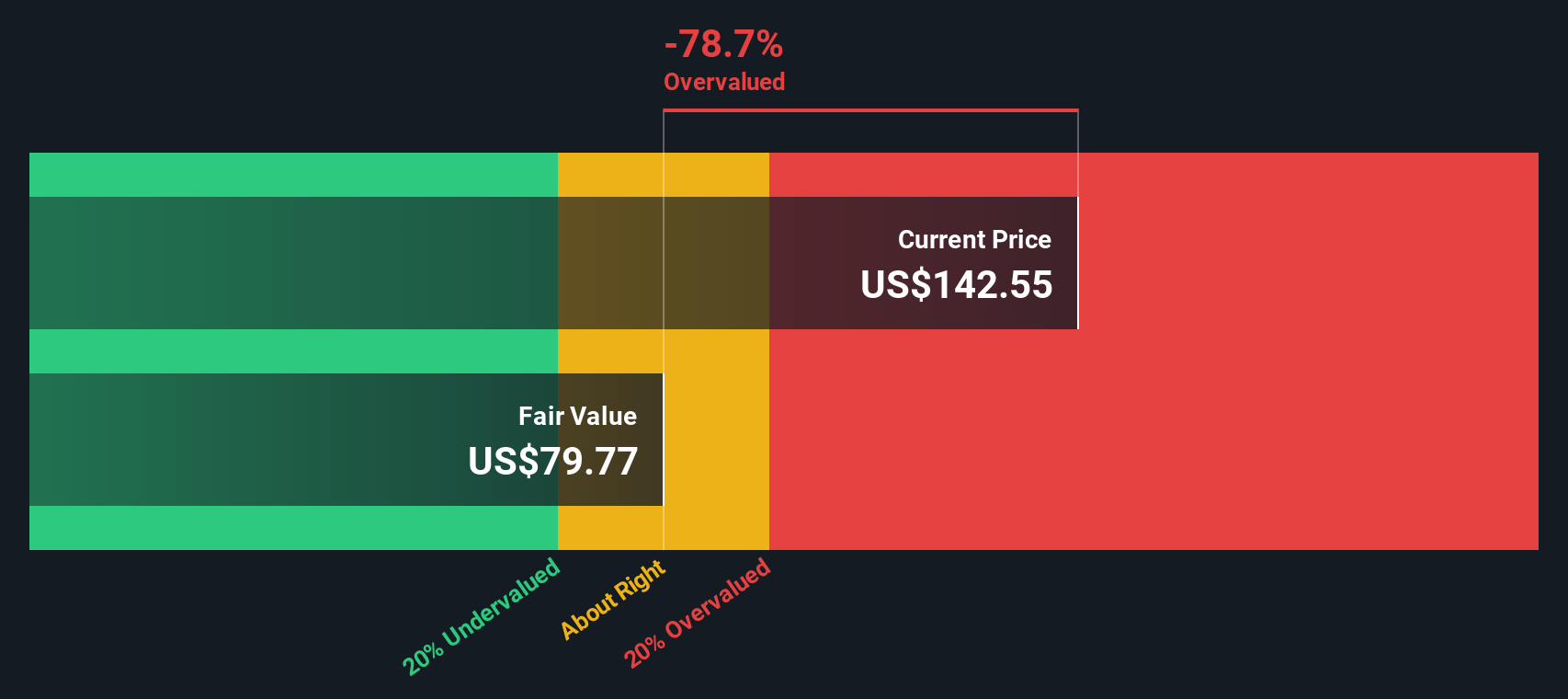

- Despite the market’s excitement around its long term track record, our simple valuation framework currently gives KKR a value score of 0/6, which seems harsh at first glance. Next we will walk through the main valuation approaches, then circle back at the end with a more nuanced way to think about what KKR is really worth.

KKR scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: KKR Excess Returns Analysis

The Excess Returns model looks at how much profit KKR can generate above the return that investors demand on its equity, then capitalizes those surplus profits into an intrinsic value per share.

In this framework, KKR starts with a Book Value of $30.54 per share and an expected Stable EPS of $5.44 per share, based on weighted future Return on Equity estimates from 6 analysts. That implies an Average Return on Equity of 11.12%, a healthy level for a capital markets business.

The model also factors in a Cost of Equity of $4.54 per share. This leads to an estimated Excess Return of $0.90 per share and a Stable Book Value of $48.89 per share, based on future book value estimates from 2 analysts. When these excess returns are projected and discounted, the Excess Returns valuation implies KKR is about 111.1% overvalued relative to its current share price.

This suggests the market is paying well ahead of what KKR’s forecast returns on equity and balance sheet growth currently justify.

Result: OVERVALUED

Our Excess Returns analysis suggests KKR may be overvalued by 111.1%. Discover 906 undervalued stocks or create your own screener to find better value opportunities.

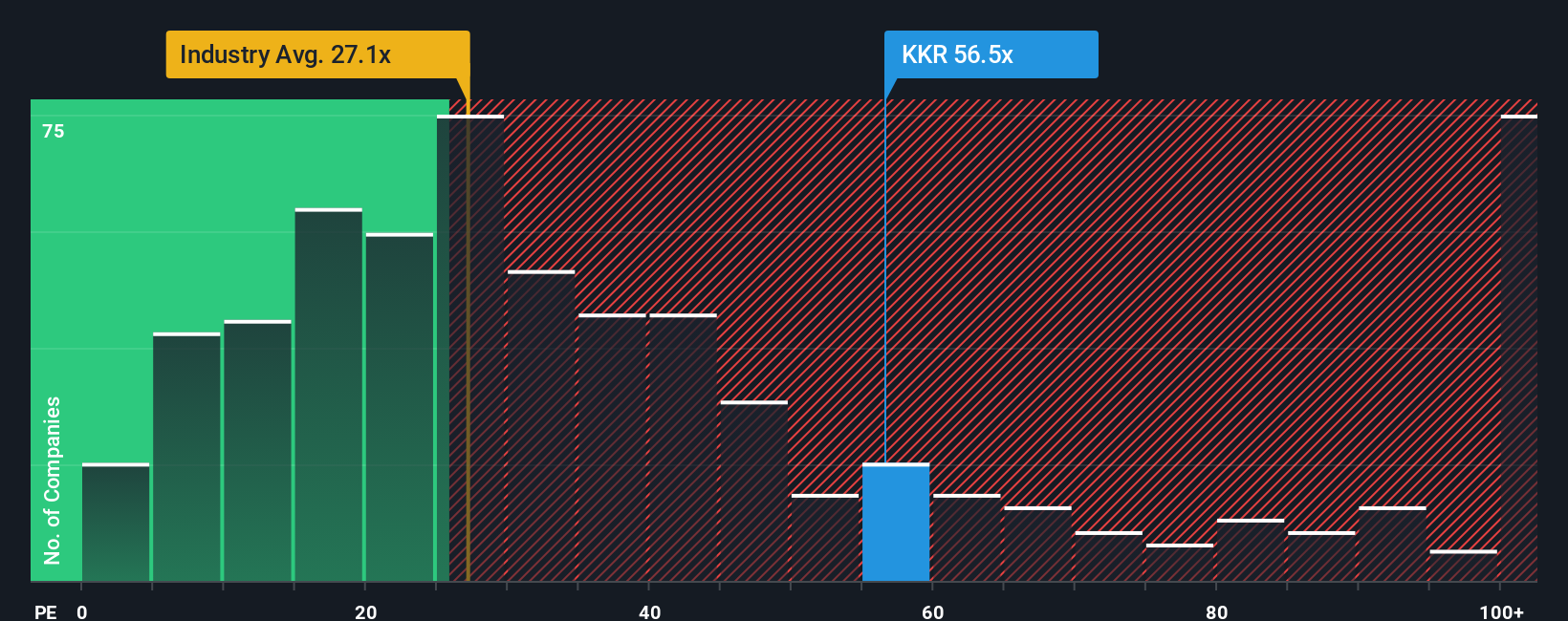

Approach 2: KKR Price vs Earnings

For a profitable business like KKR, the price to earnings multiple is a straightforward way to gauge how much investors are willing to pay today for each dollar of current earnings. It effectively bundles together expectations for future growth, perceived risk, and the quality and durability of those earnings into a single number.

In general, faster growing and less risky companies can justify a higher PE ratio, while slower growing or more volatile businesses deserve a lower one. KKR currently trades on a PE of about 52.89x, which is well above both the broader Capital Markets industry average of around 25.02x and the peer group average of roughly 37.01x. That indicates the market is assigning KKR a premium valuation versus its sector.

Simply Wall St’s Fair Ratio framework sharpens this view by estimating what PE multiple KKR should trade on, given its earnings growth outlook, margins, industry, market cap and risk profile. This produces a Fair Ratio of 26.91x, suggesting the stock’s current multiple is meaningfully higher than what those fundamentals alone would support. On this lens, KKR appears priced for very strong execution from here.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1449 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your KKR Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page that lets you connect your view of KKR’s story to explicit assumptions about its future revenue, earnings and margins. It then rolls those into a Fair Value you can compare to today’s price to help you think about whether to buy, hold or sell. That Fair Value automatically updates as new news or earnings arrive and allows for very different perspectives. For example, one investor might focus on KKR’s expanding private credit and fee streams and arrive at a Fair Value closer to the bullish end of analyst targets around $187. Another might focus on competition, regulatory risk and cyclicality and anchor nearer the $135 bear case, all within the same dynamic, easy to use tool.

Do you think there's more to the story for KKR? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com