- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

How Investors May Respond To Siemens Healthineers (XTRA:SHL) Licensing ALZpath Assay And Confirming Dividend

- Siemens Healthineers AG previously announced an annual dividend of €1.00 per share, payable on February 10, 2026, with an ex-dividend date of February 6, 2026 and a record date of February 9, 2026.

- ALZpath, Inc. has licensed its proprietary pTau217 antibody to Siemens Healthineers, enabling development of an Alzheimer's diagnostic assay for Atellica systems that could expand the company’s higher-value in vitro testing portfolio.

- We’ll now examine how adding an ALZpath-powered Alzheimer’s assay to Atellica could influence Siemens Healthineers’ long-term diagnostics-focused investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Siemens Healthineers Investment Narrative Recap

To own Siemens Healthineers, you need to believe in long term demand for advanced imaging and diagnostics, supported by solid innovation and a growing installed base. The ALZpath pTau217 deal fits that story by deepening higher value testing, but it does not change the near term picture where tariff exposure, foreign exchange headwinds and a fragile China recovery remain the key swing factors for earnings.

Of the recent news, the proposed increase in the annual dividend to €1.00 per share for 2025 stands out alongside the ALZpath agreement. For many shareholders, a rising payout can signal confidence in cash generation as the company continues to invest in areas like Alzheimer’s testing that tie directly into aging population trends and higher recurring diagnostics usage.

Yet investors should also be aware that ongoing restructuring in Diagnostics could...

Read the full narrative on Siemens Healthineers (it's free!)

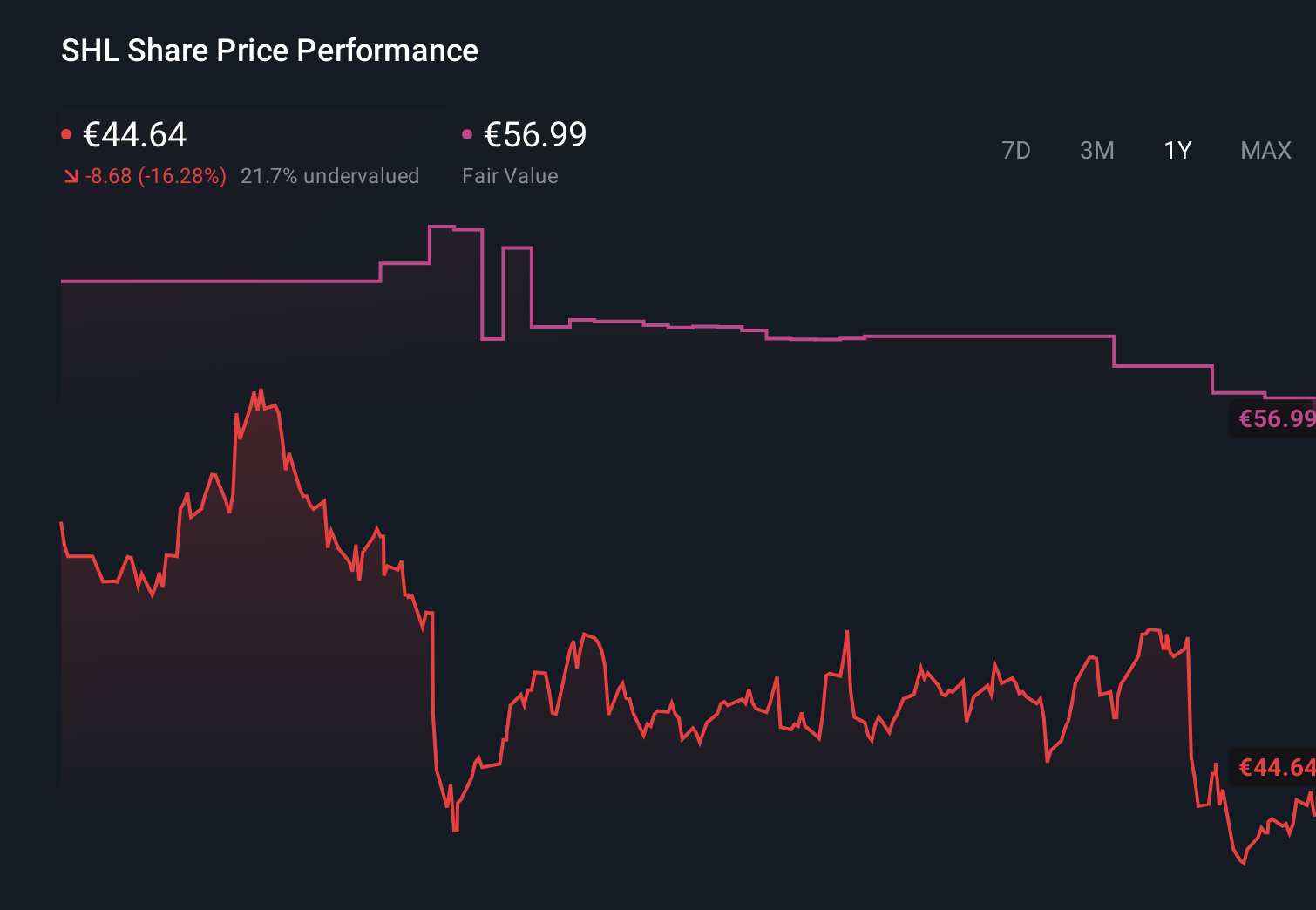

Siemens Healthineers' narrative projects €27.4 billion revenue and €3.2 billion earnings by 2028. This requires 5.4% yearly revenue growth and about a €1.0 billion earnings increase from €2.2 billion today.

Uncover how Siemens Healthineers' forecasts yield a €56.99 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community range from €36.77 to €55,409.70, underlining how far apart individual views can be. Set against this, concerns about China pricing pressure and tariffs remind you to weigh optimistic growth assumptions against tangible margin risks when you compare these perspectives.

Explore 6 other fair value estimates on Siemens Healthineers - why the stock might be worth 17% less than the current price!

Build Your Own Siemens Healthineers Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Siemens Healthineers research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Siemens Healthineers research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Siemens Healthineers' overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com