- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Is It Too Late to Consider Ulta Beauty After Its Strong 2025 Share Price Rally?

- Wondering if Ulta Beauty at around $591 a share is still worth buying, or if the big gains are already behind it? Let us unpack what the current price really implies about future returns.

- The stock has barely moved in the last week, but it is up 11.7% over the past month, 37.8% year to date, and 39.2% over the last year, with a 120.5% gain over five years that has rewarded long term holders.

- Those gains reflect growing confidence in Ulta's position as a go to beauty retailer, from its expanding store footprint to its increasingly important partnerships with major brands. Investors are also watching how Ulta balances growth investments with maintaining its strong profitability, which can shift sentiment quickly.

- Despite all that strength, Ulta Beauty only scores 1/6 on our valuation checks, which means most of our metrics do not flag it as clearly undervalued yet. Next, we will walk through the standard valuation approaches behind that score, and then dig into a more powerful way of thinking about what Ulta is really worth by the end of the article.

Ulta Beauty scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

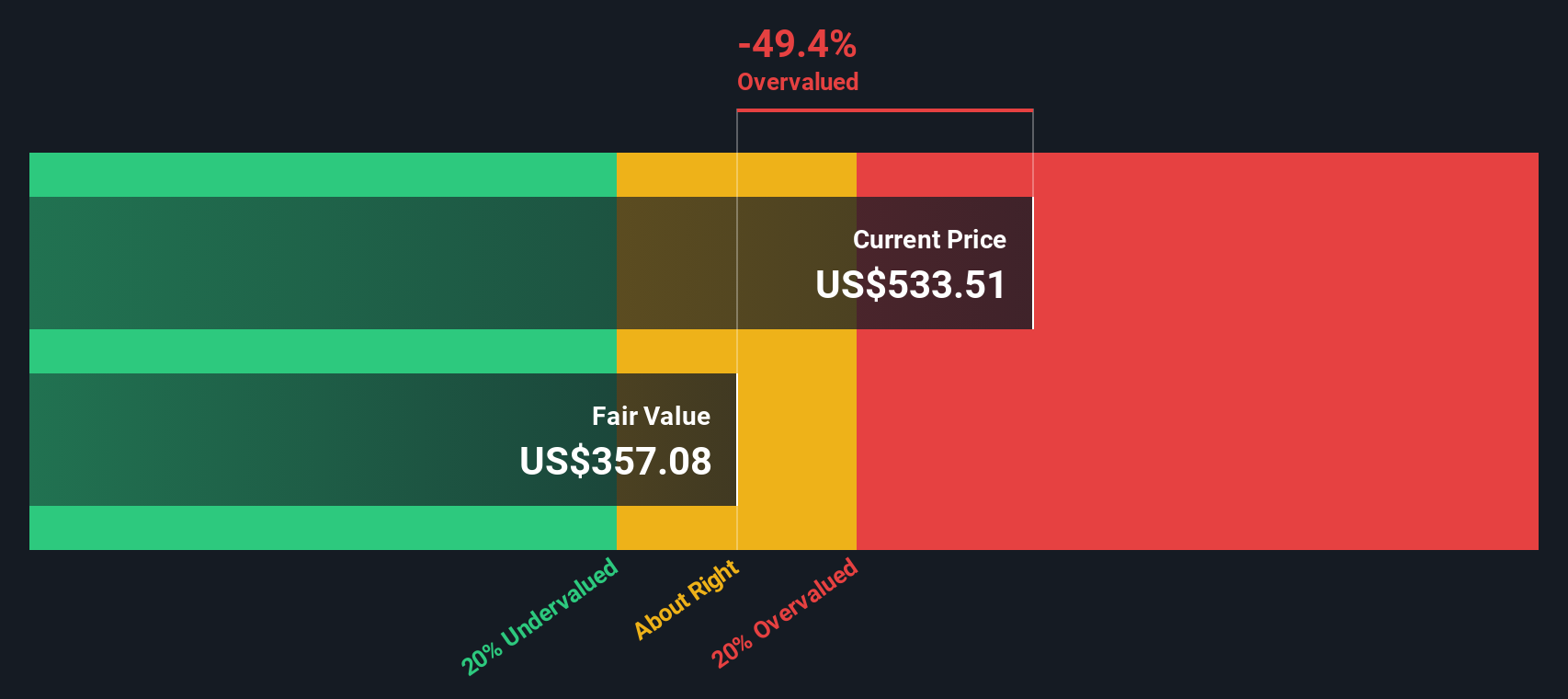

Approach 1: Ulta Beauty Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future free cash flows and discounting them back to today, to account for risk and the time value of money.

Ulta Beauty generated about $952.2 Million in free cash flow over the last twelve months in $. Analysts expect this to grow modestly, with projections of around $1,011.2 Million by early 2027 and extrapolated estimates reaching roughly $1.20 Billion by 2035. Simply Wall St uses a 2 Stage Free Cash Flow to Equity model, combining analyst forecasts for the first few years with slower, extrapolated growth thereafter.

When all those future cash flows are discounted to today, the intrinsic value comes out at about $380.74 per share. Compared with a current share price around $591, the DCF suggests Ulta Beauty is roughly 55.3% overvalued on this model.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Ulta Beauty may be overvalued by 55.3%. Discover 908 undervalued stocks or create your own screener to find better value opportunities.

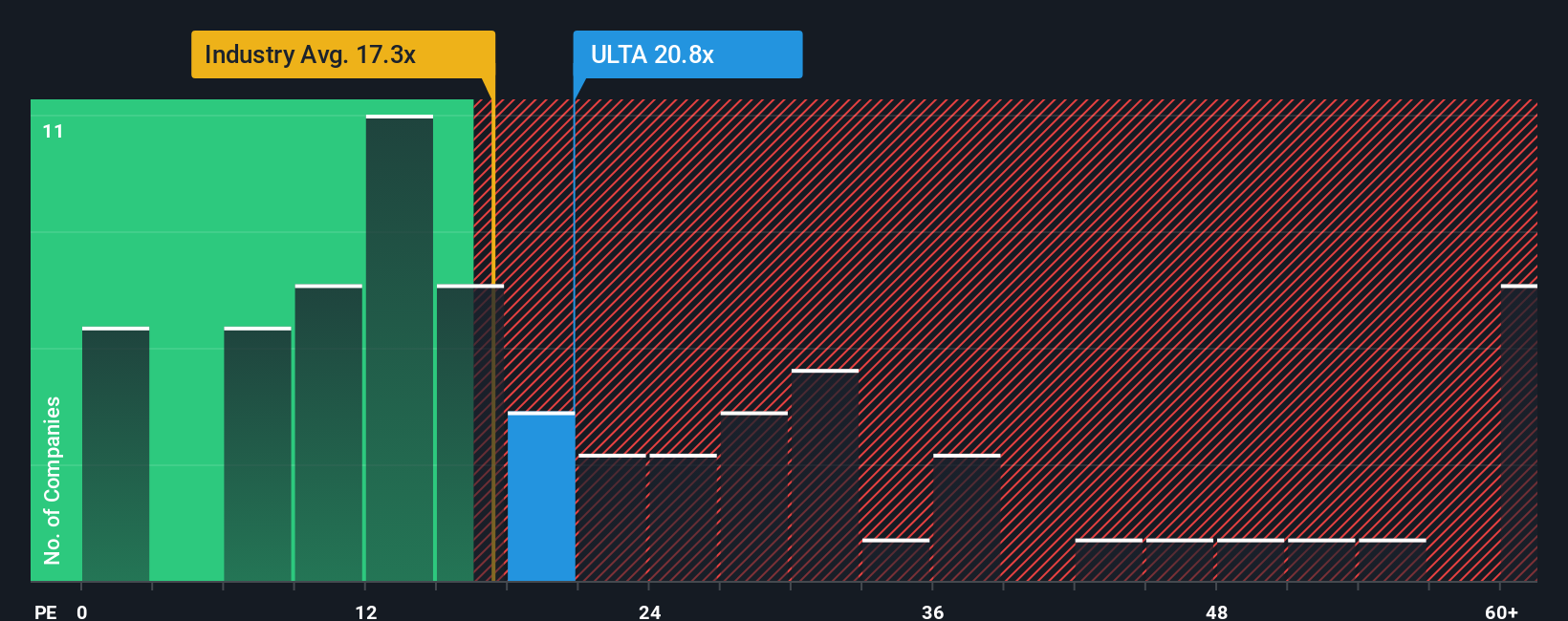

Approach 2: Ulta Beauty Price vs Earnings

For profitable companies like Ulta Beauty, the price to earnings, or PE, ratio is a natural starting point because it links what investors pay today to the profits the business is already generating. In general, higher expected growth and lower perceived risk justify a higher PE, while slower growth or more uncertainty usually means the market assigns a lower multiple.

Ulta currently trades on a PE of about 22.0x, which is slightly above the Specialty Retail industry average of roughly 20.3x, but well below the broader peer group average of around 35.8x. Simply Wall St also calculates a Fair Ratio of 18.0x, which is the PE we would expect Ulta to trade at once we factor in its earnings growth outlook, margins, industry, market cap and risk profile.

This Fair Ratio offers a more tailored benchmark than simple peer or industry comparisons, because it adjusts for Ulta specific strengths and risks rather than assuming all retailers deserve the same multiple. With the market currently valuing Ulta at 22.0x versus a Fair Ratio of 18.0x, the shares look somewhat expensive on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Ulta Beauty Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you tell the story behind your numbers by linking your view of Ulta’s business (its growth drivers, risks, and margins) to a concrete financial forecast and then to a fair value estimate, which is dynamically updated as new earnings or news arrive. This allows you to easily compare that Fair Value with today’s share price to decide whether to buy, hold, or sell, and see how your perspective stacks up against others. For example, a more bullish Ulta Narrative might lean into wellness, digital, and international expansion to justify a fair value closer to the top analyst target near $680, whereas a more cautious view might focus on cost pressures, competition, and the Target partnership loss to arrive at something nearer the low end around $405.

Do you think there's more to the story for Ulta Beauty? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com