- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Did AmeriServ Alliance Just Shift Federated Hermes' (FHI) Distribution Strategy and Investment Narrative?

- AmeriServ Financial Bank recently announced a new alliance with Federated Hermes, giving AmeriServ’s wealth management clients access to Federated Hermes’ full suite of investment research, portfolio construction tools, and products across Western Pennsylvania.

- Alongside this partnership, Federated Hermes’ strong profitability metrics and evolving leadership structure highlight how the firm is positioning its platform and people to support broader client demand.

- Now we’ll explore how this expanded AmeriServ access to Federated Hermes products may influence the company’s investment narrative and growth outlook.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Federated Hermes Investment Narrative Recap

To own Federated Hermes, you need to believe its active management, money market scale, and distribution reach can offset fee pressure and competition from passive products. The AmeriServ alliance supports this distribution-focused story, but its near term financial impact looks modest relative to the larger risk that ongoing fee compression and product commoditization could weigh on margins more meaningfully than investors expect.

Among recent updates, the upcoming leadership transition that will put Paul Uhlman in charge of global investment teams and Bryan Burke over distribution looks most relevant. For investors focused on catalysts, this reshaping of senior roles sits alongside partnerships like AmeriServ as part of how Federated Hermes tries to deepen client relationships while confronting fee pressure, regulatory complexity, and slower forecast revenue growth.

Yet even as partnerships expand access to Federated Hermes products, investors should still be alert to the risk that persistent fee compression could...

Read the full narrative on Federated Hermes (it's free!)

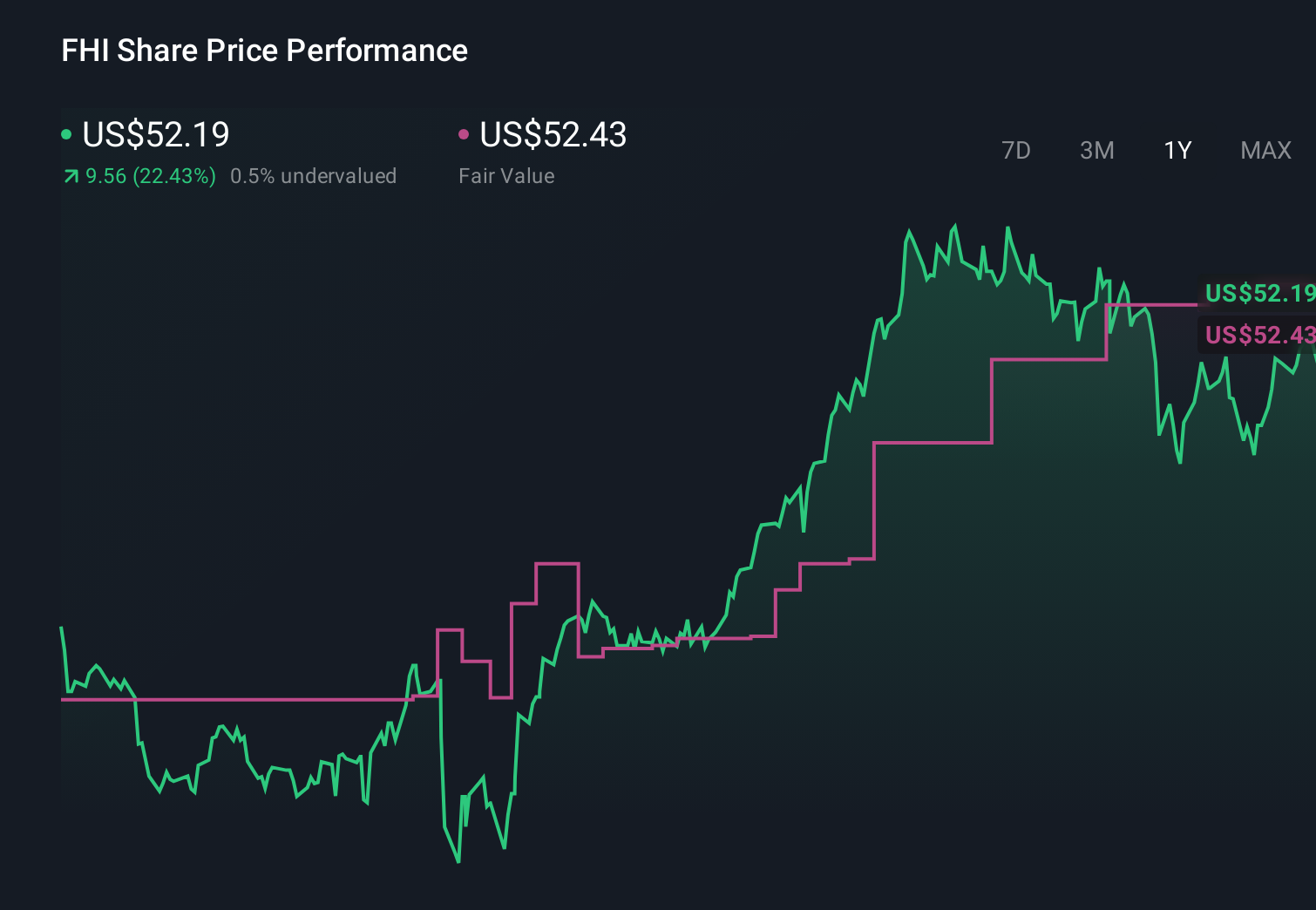

Federated Hermes' narrative projects $1.9 billion revenue and $379.7 million earnings by 2028. This requires 3.3% yearly revenue growth and about a $29.8 million earnings increase from $349.9 million today.

Uncover how Federated Hermes' forecasts yield a $52.43 fair value, in line with its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community value Federated Hermes between US$52.35 and US$58.69, showing a tight but varied band of expectations. Against that, concerns about fee compression and competition in active management hint that different views on long term profitability may be driving these gaps, so you may want to compare several of these perspectives before forming your own stance.

Explore 4 other fair value estimates on Federated Hermes - why the stock might be worth as much as 12% more than the current price!

Build Your Own Federated Hermes Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Federated Hermes research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Federated Hermes research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Federated Hermes' overall financial health at a glance.

No Opportunity In Federated Hermes?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com