- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

What Boot Barn Holdings (BOOT)'s Bullish Goldman Sachs Coverage and Store Expansion Push Means For Shareholders

- Earlier this week, Goldman Sachs initiated coverage on Boot Barn Holdings with a positive rating and a US$225 price objective, highlighting the retailer’s expanded target for new store openings and its recent milestone of surpassing 500 locations across the United States.

- The firm’s view that Boot Barn could outperform sales expectations by accelerating store expansion underscores how brick‑and‑mortar growth remains central to the company’s trajectory despite broader retail shifts.

- We’ll now explore how this new bullish coverage, particularly its emphasis on accelerated store expansion, could influence Boot Barn’s existing investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Boot Barn Holdings Investment Narrative Recap

To own Boot Barn, you need to believe its store led model can keep driving growth as it pushes deeper into underpenetrated markets, while its Western and workwear focus stays relevant to customers. Goldman Sachs’ upbeat initiation leans into that story, but it does not change the core near term setup, where the key catalyst remains execution on new store productivity and the biggest risk is that aggressive expansion starts to dilute returns.

The recent opening of Boot Barn’s 500th store, spanning 49 states, sits right at the heart of this debate. It reinforces the idea that physical expansion is still the main engine behind revenue growth, but it also brings the risk that newer locations in less proven markets could see softer demand or cannibalize existing stores if the rollout outpaces sustainable customer demand.

Yet behind this growth story, investors should also be aware of the risk that rapid store expansion could...

Read the full narrative on Boot Barn Holdings (it's free!)

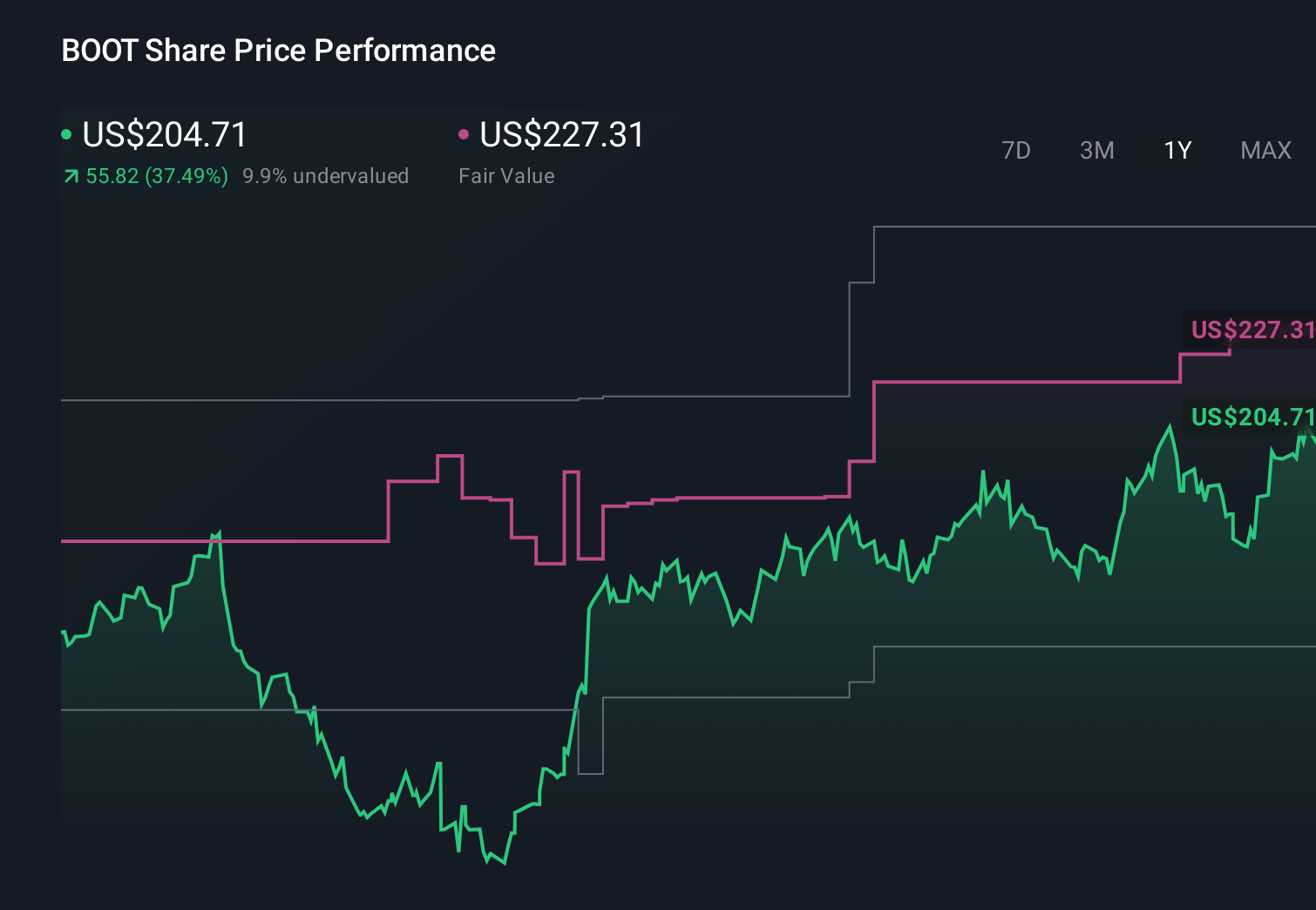

Boot Barn Holdings’ narrative projects $2.8 billion revenue and $264.7 million earnings by 2028.

Uncover how Boot Barn Holdings' forecasts yield a $227.14 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community range from about US$22.71 to US$227.14, showing just how far apart individual views can be. As you weigh those opinions, remember that much of the bullishness hinges on continued success of store expansion in new markets, which has important implications for Boot Barn’s long term sales mix and profitability.

Explore 6 other fair value estimates on Boot Barn Holdings - why the stock might be worth as much as 11% more than the current price!

Build Your Own Boot Barn Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Boot Barn Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Boot Barn Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boot Barn Holdings' overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com