- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

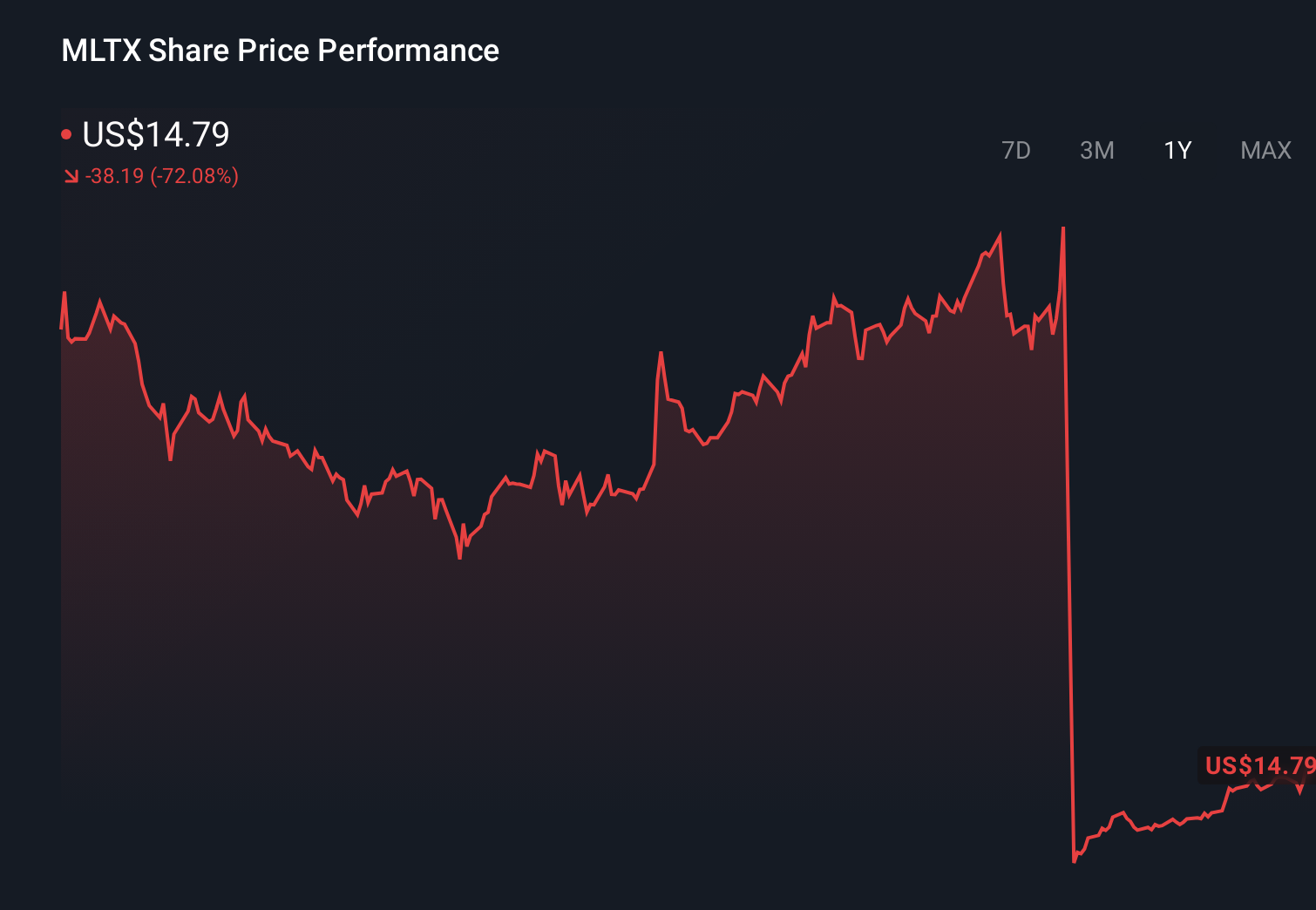

Phase 3 Miss and Fraud Suits Could Be A Game Changer For MoonLake Immunotherapeutics (MLTX)

- In late September 2025, MoonLake Immunotherapeutics revealed that its only drug candidate, sonelokimab, delivered disappointing Phase 3 results, leading to multiple securities class action lawsuits alleging the company misled investors about the drug’s efficacy and Nanobody advantages.

- The litigation centers on claims that MoonLake overstated sonelokimab’s superiority versus an existing treatment while allegedly not fully disclosing their similar biological targets and unproven clinical benefit.

- We’ll now examine how these Phase 3 shortcomings and fraud allegations reshape MoonLake’s investment narrative and risk profile for investors.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

What Is MoonLake Immunotherapeutics' Investment Narrative?

To own MoonLake now, you have to believe sonelokimab can still become a commercially relevant franchise despite its recent Phase 3 setback and the shock of a nearly 90% share price collapse. The short term story had been about regulatory progress in hidradenitis suppurativa (HS), a potential BLA path after the upcoming FDA Type B meeting, and advancing PPP into Phase 3, all funded by fresh equity. The disappointing Phase 3 data and the wave of securities class actions change that balance: the main catalyst is no longer just regulatory, it is whether the remaining HS and PPP data convince partners, regulators and investors that SLK has a real edge. At the same time, higher cash burn, legal overhang and governance questions now sit front and center.

However, the legal overhang and management credibility questions are information investors should not ignore. According our valuation report, there's an indication that MoonLake Immunotherapeutics' share price might be on the expensive side.Exploring Other Perspectives

The Simply Wall St Community currently shows 1 fair value view clustered at US$14.61 per share, underscoring how a single opinion can differ from recent market trading. Set that against MoonLake’s sole drug reliance, fresh legal risks and ongoing losses, and it is clear you are weighing contrasting stories about how much setback the business model can absorb.

Explore another fair value estimate on MoonLake Immunotherapeutics - why the stock might be worth just $14.61!

Build Your Own MoonLake Immunotherapeutics Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your MoonLake Immunotherapeutics research is our analysis highlighting 4 important warning signs that could impact your investment decision.

- Our free MoonLake Immunotherapeutics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MoonLake Immunotherapeutics' overall financial health at a glance.

No Opportunity In MoonLake Immunotherapeutics?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com