- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Is Surgery Partners Mispriced After 42.3% Five Year Slide and Outpatient Expansion?

- If you are wondering whether Surgery Partners is a quietly mispriced opportunity or a value trap in the making, you are not alone. That is exactly what we are going to unpack here.

- The stock is down 4.9% over the last week and 22.4% year to date, but a 5.0% gain over the past month hints that sentiment may be starting to shift after a long 5 year slide of 42.3%.

- Recent headlines have focused on Surgery Partners expanding its network of ambulatory surgery centers and deepening relationships with physicians and payors. These moves can structurally improve margins and growth visibility. Analysts have also highlighted the broader shift of procedures from hospitals to outpatient settings, which positions the company to benefit if execution stays on track.

- Against that backdrop, Surgery Partners currently scores a solid 5 out of 6 on our valuation checks, suggesting the market may be underestimating its potential. Next we will walk through the different valuation methods behind that view, before finishing with an even more powerful way to think about what the stock is really worth.

Find out why Surgery Partners's -18.4% return over the last year is lagging behind its peers.

Approach 1: Surgery Partners Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and then discounting them back to today in dollar terms. For Surgery Partners, the model starts with last twelve month free cash flow of about $184 million and uses a two stage Free Cash Flow to Equity framework, with analyst forecasts for the next few years and then more gradual growth assumptions beyond that.

Under these projections, annual free cash flow is expected to rise to roughly $632 million by 2035, with interim years climbing steadily from $398 million in 2026 and $437 million in 2027. Simply Wall St extrapolates the later years once analyst coverage tapers off, then discounts each year’s cash flow to today and adds a terminal value.

This cash flow stream implies an intrinsic value of about $68.68 per share. Compared with the current market price, the DCF suggests the stock is trading at roughly a 75.9% discount, indicating investors are pricing in weaker outcomes than the model assumes.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Surgery Partners is undervalued by 75.9%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

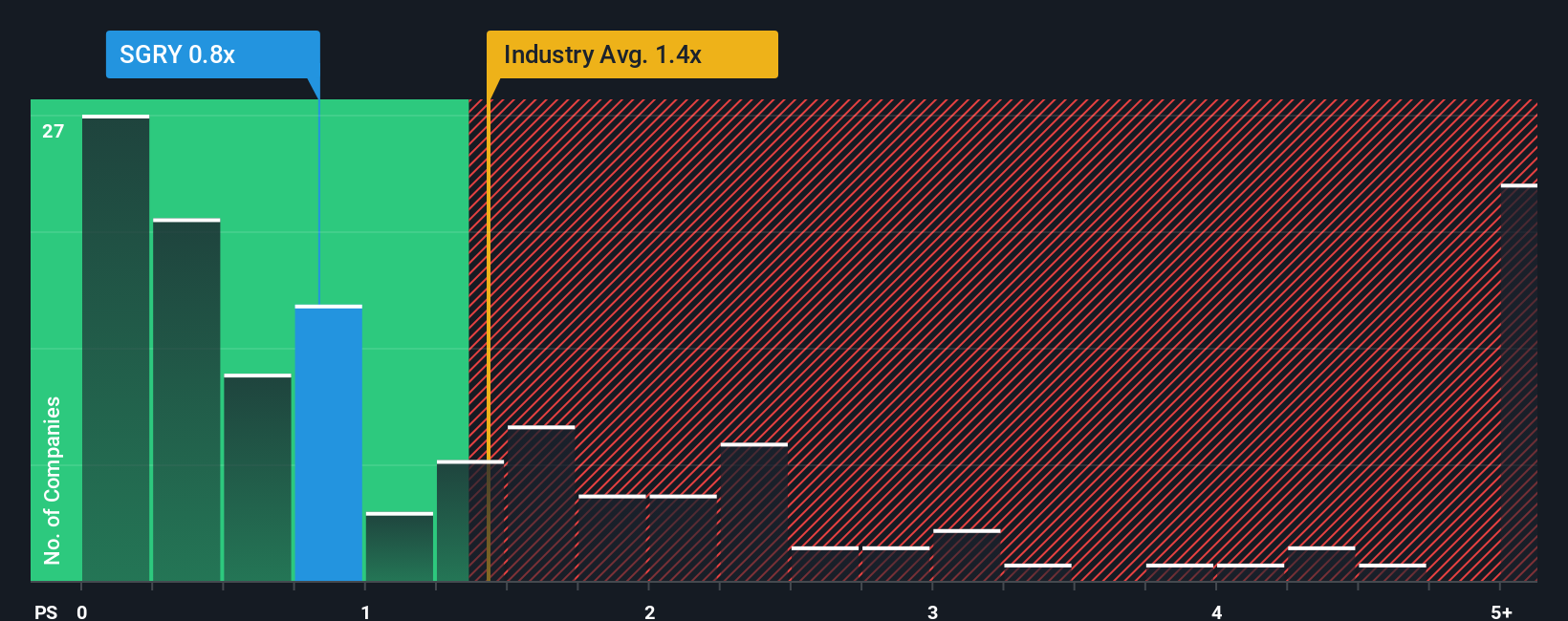

Approach 2: Surgery Partners Price vs Sales

For companies where profitability is still ramping up, the price to sales multiple is often a better yardstick than earnings based metrics. It focuses on how the market values every dollar of revenue regardless of near term margin noise. What investors are really weighing is how quickly those sales can grow and how risky that growth path looks, which together drive what a normal valuation range should be.

Surgery Partners currently trades on a price to sales ratio of about 0.65x. That is below both the broader Healthcare industry average of roughly 1.29x and a peer group average of around 0.95x, suggesting the market is applying a discount to its top line relative to comparable businesses.

Simply Wall St also calculates a Fair Ratio of 0.78x, a proprietary estimate of what the price to sales multiple should be given Surgery Partners specific growth profile, margins, risks, size and industry. This is more nuanced than a simple peer or sector comparison because it incorporates company level fundamentals rather than assuming all players deserve the same multiple. With the current 0.65x sitting below the 0.78x Fair Ratio, the price to sales lens points to the stock being modestly undervalued.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Surgery Partners Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Surgery Partners story with a financial forecast and a fair value estimate, all within the Simply Wall St Community page that millions of investors use. A Narrative is your own story behind the numbers, where you choose assumptions for future revenue, earnings and margins, and the platform turns those into a forecast and a Fair Value that you can compare with today’s share price to help inform whether you think the stock is a buy, hold or sell. Narratives update dynamically as new information like earnings results, guidance changes or major news comes in. This means your conclusions can evolve with the facts rather than staying locked to a static model. For example, one investor might build a more optimistic Surgery Partners Narrative that assumes long term revenue growth closer to 9.9%, margin expansion to around 3.8% and a higher future PE near 36x. Another may choose a more cautious view with slower growth, lower margins and a more conservative multiple, leading to very different Fair Values but all using the same intuitive framework.

Do you think there's more to the story for Surgery Partners? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com