- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Has Coupang’s Recent Rally Left More Room For Long Term Growth In 2025?

- Investors may be wondering whether Coupang is still a smart place to put money after its big run over the last few years, or if most of the upside has already been priced in.

- The stock is up 50.7% over the past 3 years and 16.9% year to date, even though it has slipped 1.9% in the last week and 9.9% over the past month. This pattern often signals shifting sentiment rather than a broken story.

- Recently, investors have been paying closer attention to Coupang's ongoing expansion of its logistics network and newer services like Wow membership and food delivery, which strengthen its ecosystem and can support long term growth. At the same time, the market has been reassessing high growth e commerce names more broadly as interest rate expectations and risk appetite change, and Coupang has been pulled into that narrative.

- Based on our checks, Coupang scores a 3/6 valuation score, suggesting the market may only be partially pricing in its fundamentals. Next, we will unpack what different valuation approaches say about the stock, and then finish with a more holistic way to think about its worth beyond the usual models.

Approach 1: Coupang Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model projects a company’s future cash flows and then discounts them back to today’s dollars to estimate what the business is worth right now.

For Coupang, the model starts with last twelve month Free Cash Flow of about $1.27 billion and uses analyst forecasts for the next few years, then extrapolates further using Simply Wall St assumptions. By 2027, Coupang’s Free Cash Flow is projected to reach roughly $2.52 billion, and the extended 10 year forecast continues to climb from there as the business scales and margins improve.

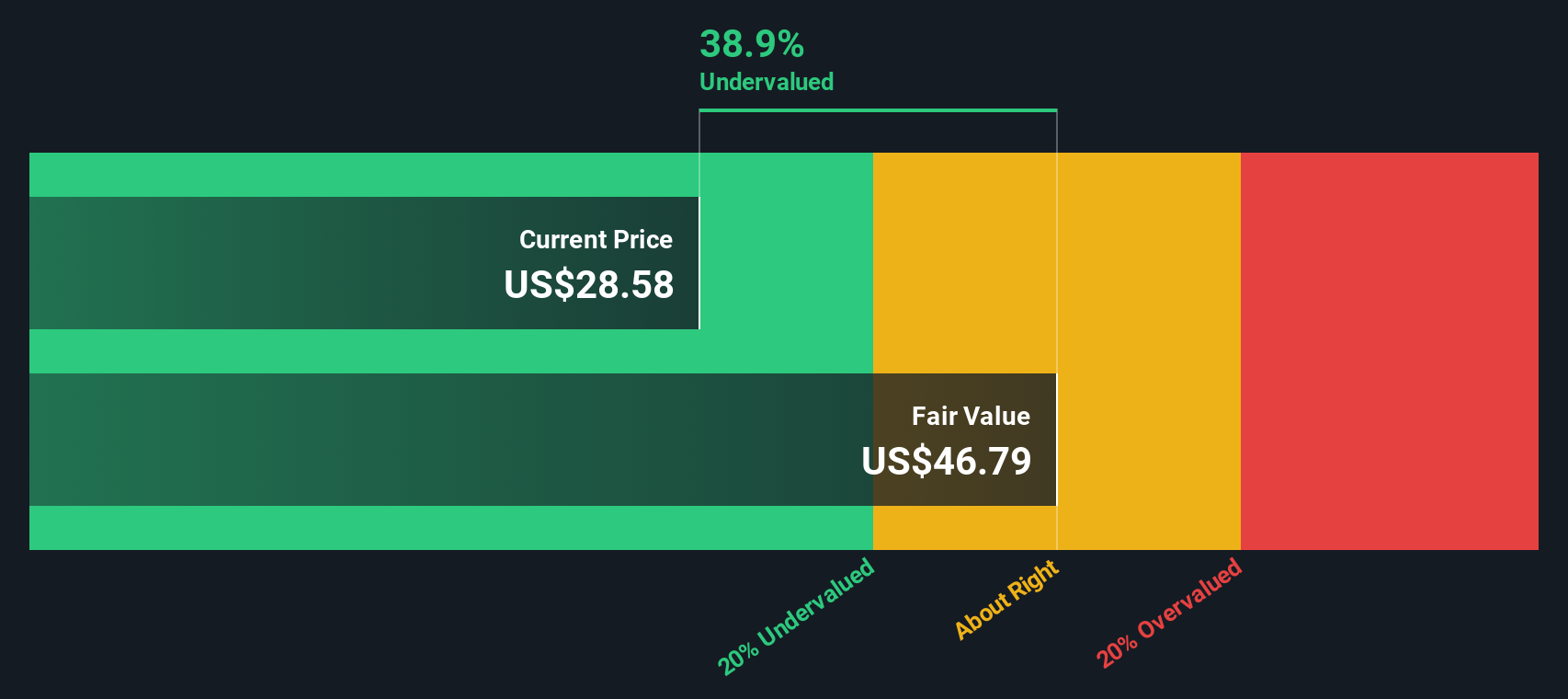

When all of those projected cash flows are discounted back to the present, the DCF model estimates an intrinsic value of about $38.78 per share. This implies the stock is trading at roughly a 32.8% discount to its calculated fair value, which indicates that the market is still cautious about how durable Coupang’s growth and profitability will be.

Overall, the DCF view presents Coupang as a growth story that the market may not be fully crediting yet.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Coupang is undervalued by 32.8%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

Approach 2: Coupang Price vs Earnings

For companies that are already profitable, the Price to Earnings ratio is a practical way to gauge valuation because it ties the share price directly to the earnings power that investors ultimately rely on. A higher or lower PE is not good or bad on its own; it should reflect how fast earnings are expected to grow and how risky those earnings are.

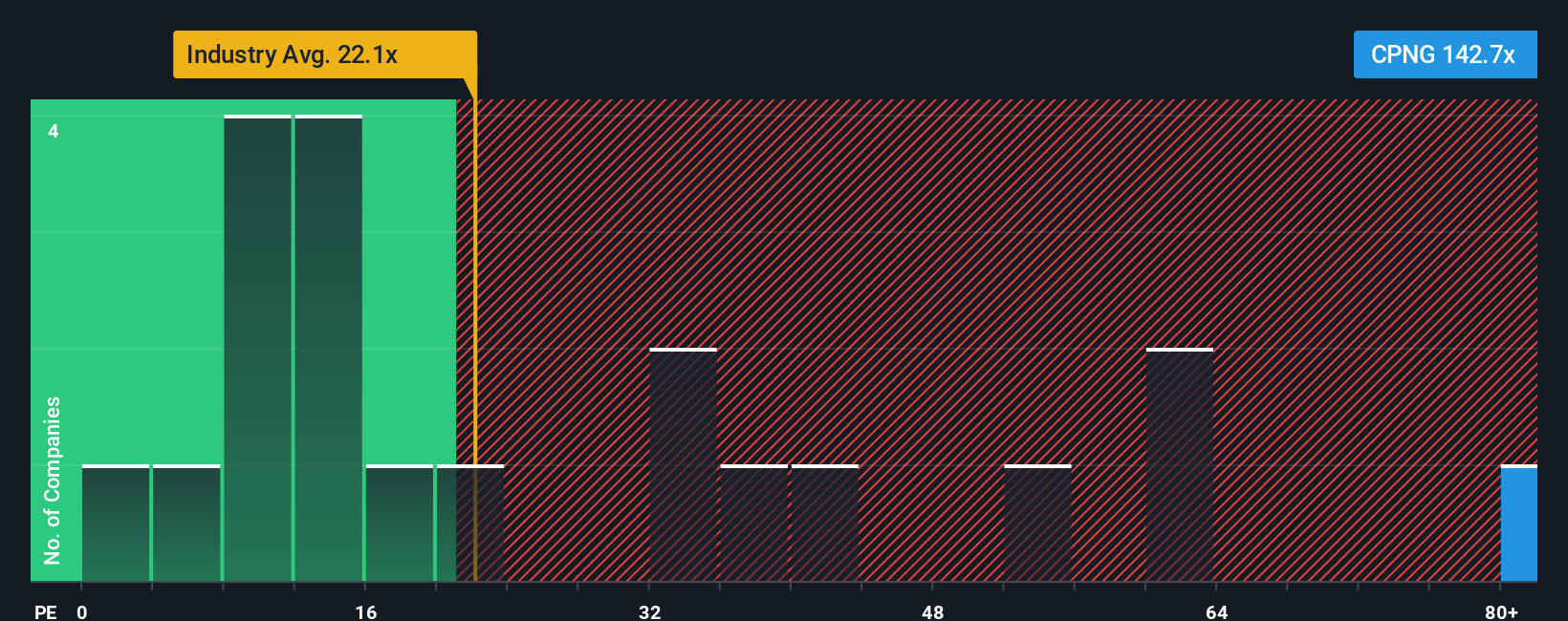

Coupang currently trades on a PE of about 122.1x, which is far richer than both the Multiline Retail industry average of roughly 19.9x and the broader peer group average of around 31.6x. To move beyond simple comparisons, Simply Wall St uses a proprietary Fair Ratio, which estimates what a reasonable PE should be given factors like Coupang's earnings growth outlook, margins, industry, market cap and risk profile.

This Fair Ratio for Coupang is 43.5x, well below the current 122.1x. Because the Fair Ratio adjusts for growth and risk in a more systematic way than blunt peer or industry averages, it offers a more tailored benchmark for the stock. On this basis, Coupang screens as significantly overvalued on earnings.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Coupang Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, a simple way to connect your view of Coupang's future to actual numbers like revenue, earnings, margins and a fair value estimate.

A Narrative is the story you believe about a company, translated into a structured forecast that spells out how fast you expect sales to grow, how profitable the business can become and what that should make the stock worth today.

On Simply Wall St, Narratives live in the Community page and are designed to be accessible, so you do not need to build a full model yourself. The platform helps you move from story, to forecast, to Fair Value, then compares that against the current share price so you can see how your view of Coupang aligns with different valuation scenarios.

These Narratives update dynamically as new information comes in, like earnings results, changes in analyst forecasts or major news, and you can see how other investors differ. For example, one Narrative might assume a fair value of about $27 per share while a more optimistic one might land closer to $36, reflecting different expectations for Coupang's growth and profitability.

Do you think there's more to the story for Coupang? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com