- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

How Strong Q3 Results And Tech Efficiency Push At Devon Energy (DVN) Has Changed Its Investment Story

- In recent months, Devon Energy reported stronger-than-expected Q3 results, with revenue and adjusted EPS surpassing analyst estimates on the back of solid oil, gas, and NGL sales, while continuing to expand activity across major U.S. basins such as the Delaware, Eagle Ford, Anadarko, Williston, and Powder River.

- Investor attention has also been shaped by JP Morgan’s upgrade of Devon Energy and the company’s focus on technology-driven operational efficiencies, which together highlight how its shale portfolio and data-driven approach are influencing analyst views on its long-term role in the U.S. energy landscape.

- Building on this earnings beat and analyst upgrade, we’ll now explore how Devon’s technology-driven efficiency push may reshape its investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Devon Energy Investment Narrative Recap

To own Devon Energy, you need to believe in the durability of U.S. shale output, the company’s ability to offset natural decline rates with technology-driven efficiency, and disciplined capital returns. The latest earnings beat and JP Morgan upgrade support the near term catalyst of improved sentiment, but they do not materially change the biggest risk, which remains Devon’s exposure to volatile oil, gas, and NGL prices and the broader energy transition.

Among recent announcements, Devon’s consistent share repurchase activity stands out, with 92,672,000 shares bought back for US$4,149.68 million since 2021. For investors following catalysts like analyst upgrades and operational efficiency gains, this ongoing buyback program adds another layer to how the company is positioning itself while still operating within a commodity price driven business model.

Yet, while the story around technology and capital returns is compelling, investors should still be aware of how dependent Devon remains on future regulatory shifts around water management and environmental standards...

Read the full narrative on Devon Energy (it's free!)

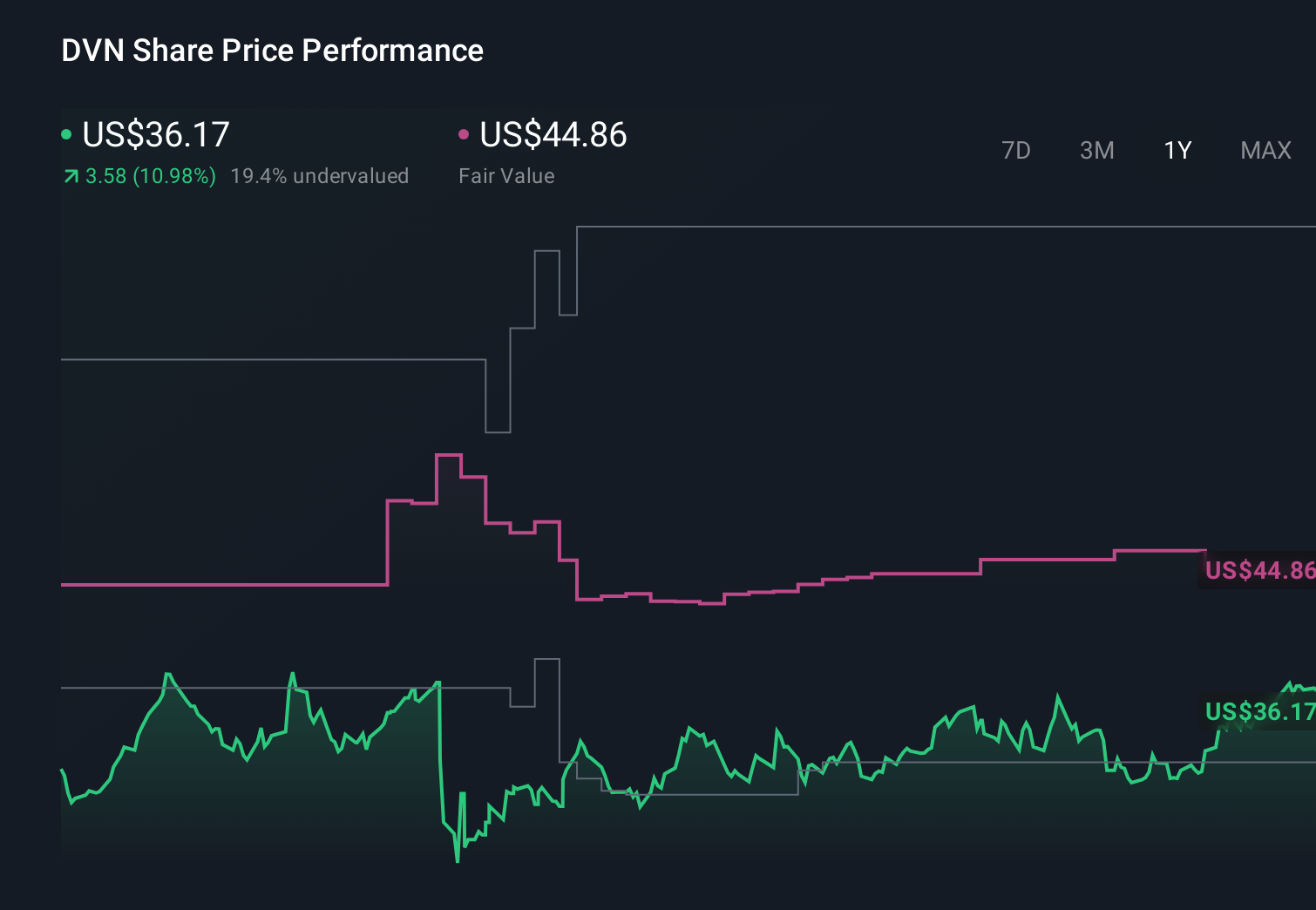

Devon Energy's narrative projects $19.3 billion revenue and $3.0 billion earnings by 2028.

Uncover how Devon Energy's forecasts yield a $44.86 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members offer 11 fair value views for Devon, ranging from US$30.95 to US$105.69, reflecting very different expectations. You can weigh these against the key risk that Devon’s cash flows remain tightly linked to unpredictable commodity prices and the pace of the global energy transition.

Explore 11 other fair value estimates on Devon Energy - why the stock might be worth over 2x more than the current price!

Build Your Own Devon Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Devon Energy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Devon Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Devon Energy's overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com