- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Has the Market Already Priced In Antero Midstream’s Strong Multi Year Share Price Run?

- Wondering if Antero Midstream is still a good buy after its run up, or if most of the easy money has already been made? In this article, we break down what the market is really pricing in here.

- The stock has climbed to around $18.58, delivering roughly 4.6% over the last week, 4.9% over the past month, 20.0% year to date and 30.5% over the last year, with a 109.6% gain over three years and 235.0% over five years.

- Those moves have come as midstream energy names like Antero have benefited from a more constructive outlook on US natural gas infrastructure and investor demand for steady, fee based cash flows. At the same time, the broader shift toward income focused, lower volatility plays has pushed more attention onto pipeline and midstream operators.

- Right now, Antero Midstream scores a 4 out of 6 on our valuation checks, suggesting it looks undervalued on several important measures. The next sections walk through the main valuation approaches behind that score and then finish with a more intuitive way to think about what the market is really paying for in this stock.

Approach 1: Antero Midstream Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and discounting those cash flows back to today using an appropriate rate. For Antero Midstream, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in $.

The company generated roughly $616.6 Million in free cash flow over the last twelve months. Analyst forecasts and subsequent extrapolations by Simply Wall St suggest this could rise to about $1.15 Billion in annual free cash flow in 10 years, with interim projections steadily climbing from the $800 Million range in 2026. These cash flows are then discounted back to today, reflecting the time value of money and the risks of executing that growth path.

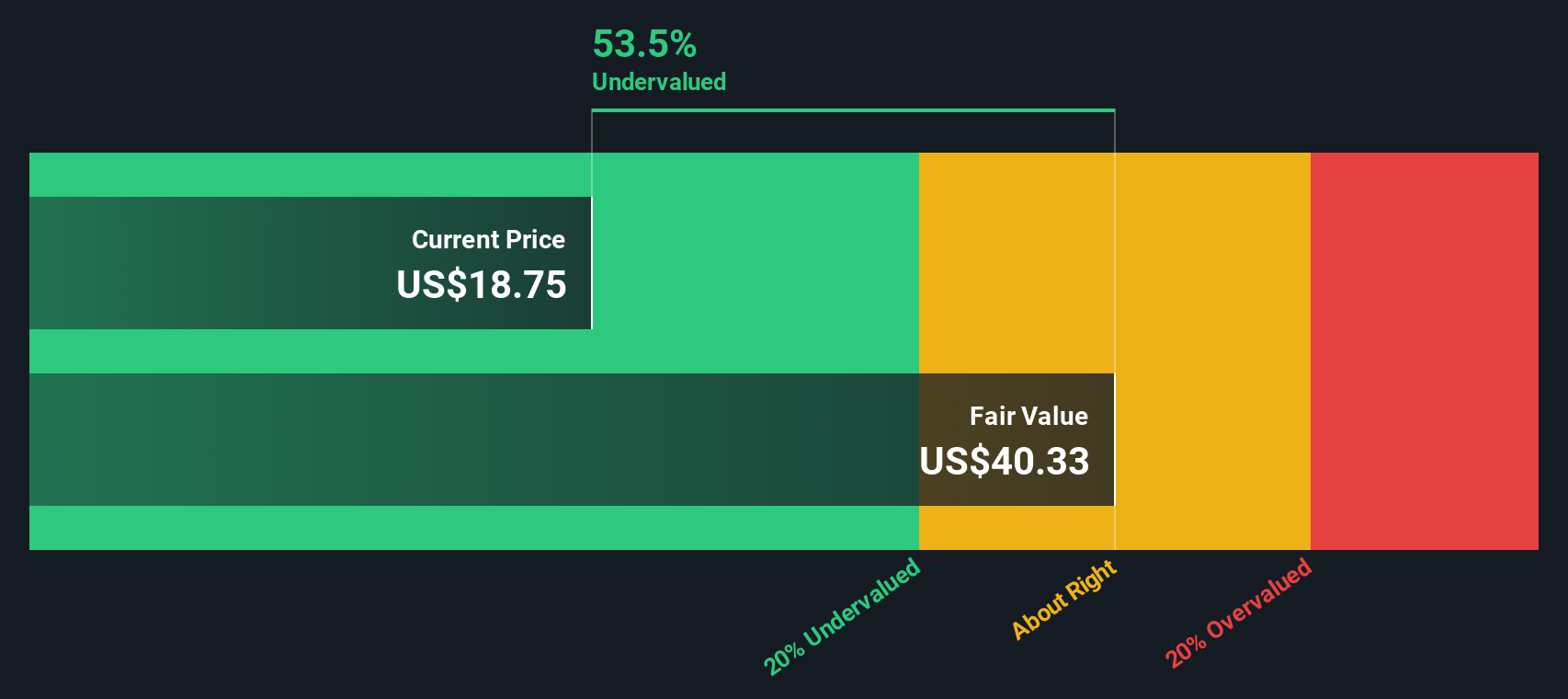

On this basis, the DCF model estimates an intrinsic value of about $48.41 per share, implying the stock is trading at a 61.6% discount to its fair value at the current price around $18.58. That indicates a materially undervalued name on cash flow fundamentals.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Antero Midstream is undervalued by 61.6%. Track this in your watchlist or portfolio, or discover 895 more undervalued stocks based on cash flows.

Approach 2: Antero Midstream Price vs Earnings

For a consistently profitable business like Antero Midstream, the price to earnings ratio is a useful way to gauge what investors are paying for each dollar of current earnings. In general, faster growth and lower perceived risk support a higher, or more generous, PE ratio, while slower growth or higher risk usually justify a lower one.

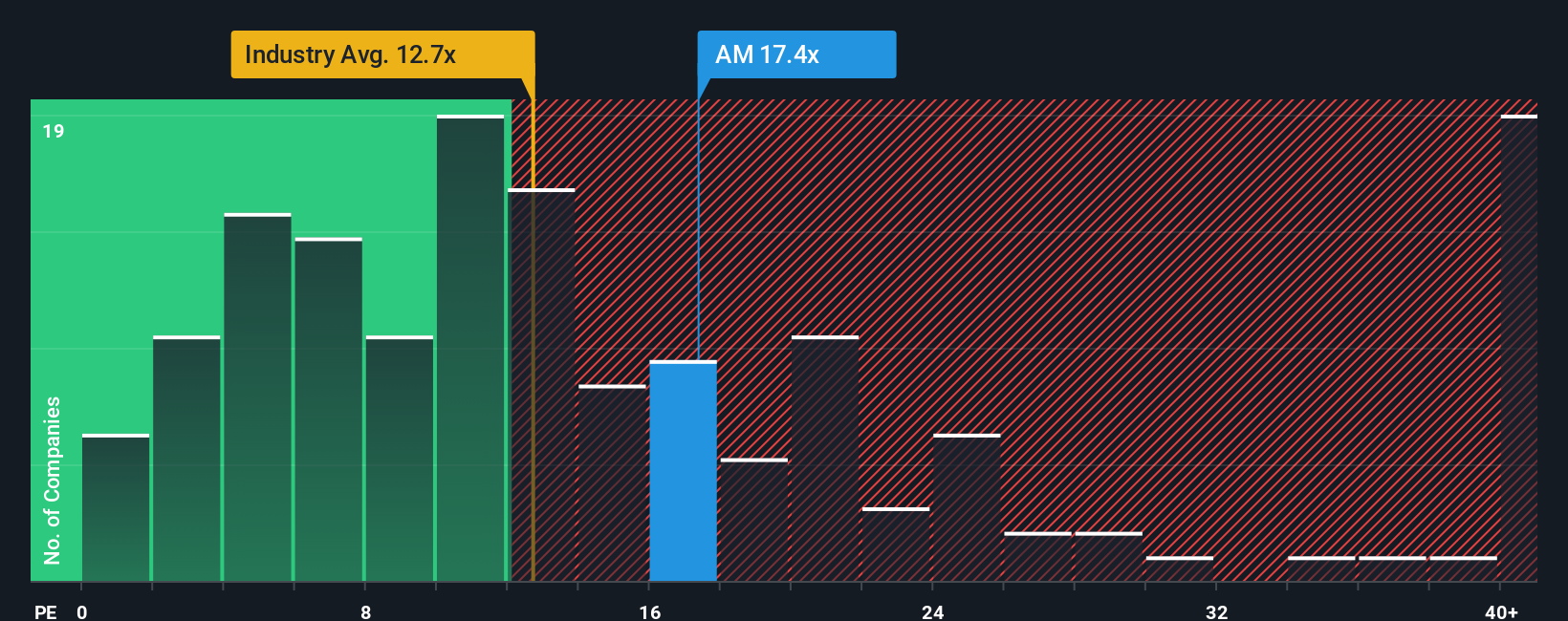

Right now, Antero Midstream trades on roughly 18.8x earnings, compared with about 13.5x for the broader Oil and Gas industry and roughly 40.0x for its peer group. Simply Wall St also calculates a proprietary Fair Ratio of 19.6x, which reflects what a reasonable PE might be once you factor in Antero Midstream’s specific earnings growth outlook, profitability, industry positioning, size and risk profile.

This Fair Ratio is more tailored than a simple comparison with peers or the sector because it adjusts for differences in growth, margins, risk and market cap that can distort headline multiples. With the stock at 18.8x compared with an indicated fair level of 19.6x, Antero Midstream appears modestly undervalued on earnings, rather than stretched after its recent run.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1450 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Antero Midstream Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework where you describe your view of a company, link it to a set of forecasts for revenue, earnings and margins, and end up with a clear estimate of fair value.

On Simply Wall St’s Community page, Narratives are easy to build and compare, because they connect a company’s story with a financial model that outputs a Fair Value you can set against today’s share price to decide whether it looks like a buy, a hold or a sell.

They are dynamic as well, automatically updating as new information like earnings reports, guidance changes or major news is incorporated, so your view stays grounded in the latest data without you having to rebuild everything from scratch.

For Antero Midstream, one investor might build a bullish Narrative around rising LNG demand, margin expansion toward the low 50s and disciplined buybacks that support a fair value above $19 per share. Another could focus on concentration risk, regulatory pressure and slower growth to justify a more cautious fair value closer to $16. Seeing both side by side helps you choose which story you find more compelling and how that might inform your own decision making.

Do you think there's more to the story for Antero Midstream? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com