- LIVE QUOTES

- LEARN

- HELP

EN

Undiscovered Gems in Asia to Explore This December 2025

As December 2025 unfolds, the Asian markets are capturing attention with their dynamic shifts, particularly as China's technology sector shows resilience despite broader economic challenges. Amidst these developments, investors are keenly observing small-cap stocks which often present unique opportunities in such fluctuating environments. Identifying a promising stock involves considering its potential for growth and adaptability within the current market conditions, making it essential to explore those companies that demonstrate robust fundamentals and innovative strategies.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Rectron | NA | 0.06% | -1.41% | ★★★★★★ |

| Daphne International Holdings | NA | -5.92% | 82.03% | ★★★★★★ |

| Tech Semiconductors | NA | -0.61% | 33.99% | ★★★★★★ |

| Uju Holding | 34.04% | 5.58% | -25.17% | ★★★★★★ |

| E J Holdings | 20.38% | 4.50% | 2.36% | ★★★★★☆ |

| Zhe Jiang Dayang Biotech Group | 31.27% | 6.28% | -5.17% | ★★★★★☆ |

| Poly Plastic Masterbatch (SuZhou)Ltd | 4.59% | 17.51% | 3.97% | ★★★★★☆ |

| Palasino Holdings | 8.57% | 4.07% | -18.45% | ★★★★★☆ |

| Huasi Holding | 6.89% | 4.80% | 41.72% | ★★★★★☆ |

| Lan Fa Textile | 32.29% | -13.25% | 6.51% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

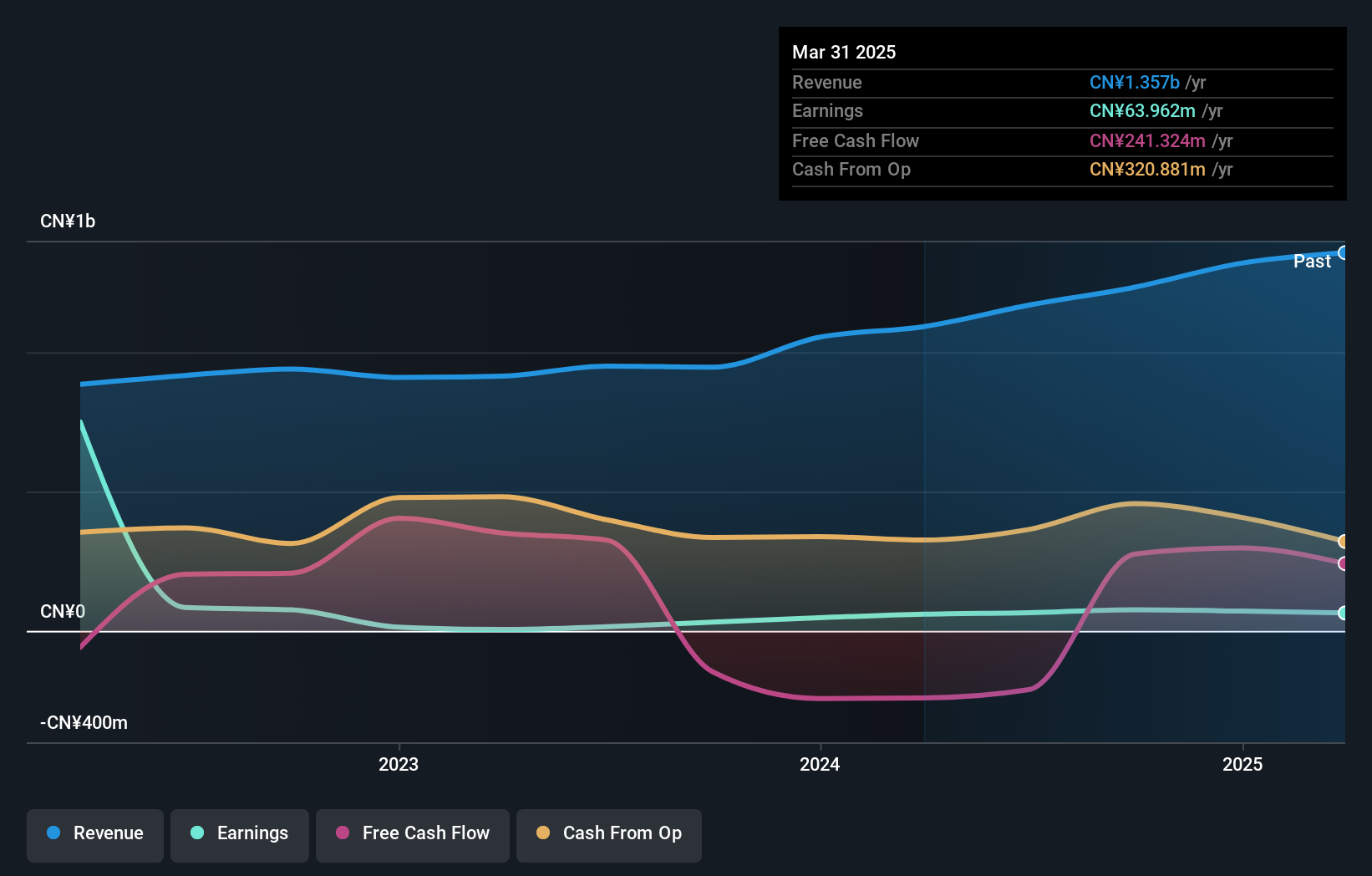

Sichuan Haite High-techLtd (SZSE:002023)

Simply Wall St Value Rating: ★★★★★★

Overview: Sichuan Haite High-tech Co., Ltd specializes in providing aircraft airborne equipment maintenance services in China and has a market cap of CN¥10.06 billion.

Operations: The company generates revenue primarily from its aircraft airborne equipment maintenance services. It has a market capitalization of CN¥10.06 billion, reflecting its significant presence in the industry. The financial performance is characterized by a focus on service-based revenue streams within China.

Sichuan Haite High-tech, a smaller player in the infrastructure sector, has shown impressive growth over the past year with earnings rising by 69.7%, outpacing the industry average of -0.7%. The company's debt situation seems manageable, with a net debt to equity ratio at 13.8%, which is considered satisfactory and has improved from 60.2% five years ago to 33.9%. Recently, their nine-month earnings report revealed sales of CNY 1.09 billion compared to CNY 911 million last year, and net income increased significantly from CNY 61.9 million to CNY 119 million, indicating robust financial performance despite previous challenges in earnings growth over five years.

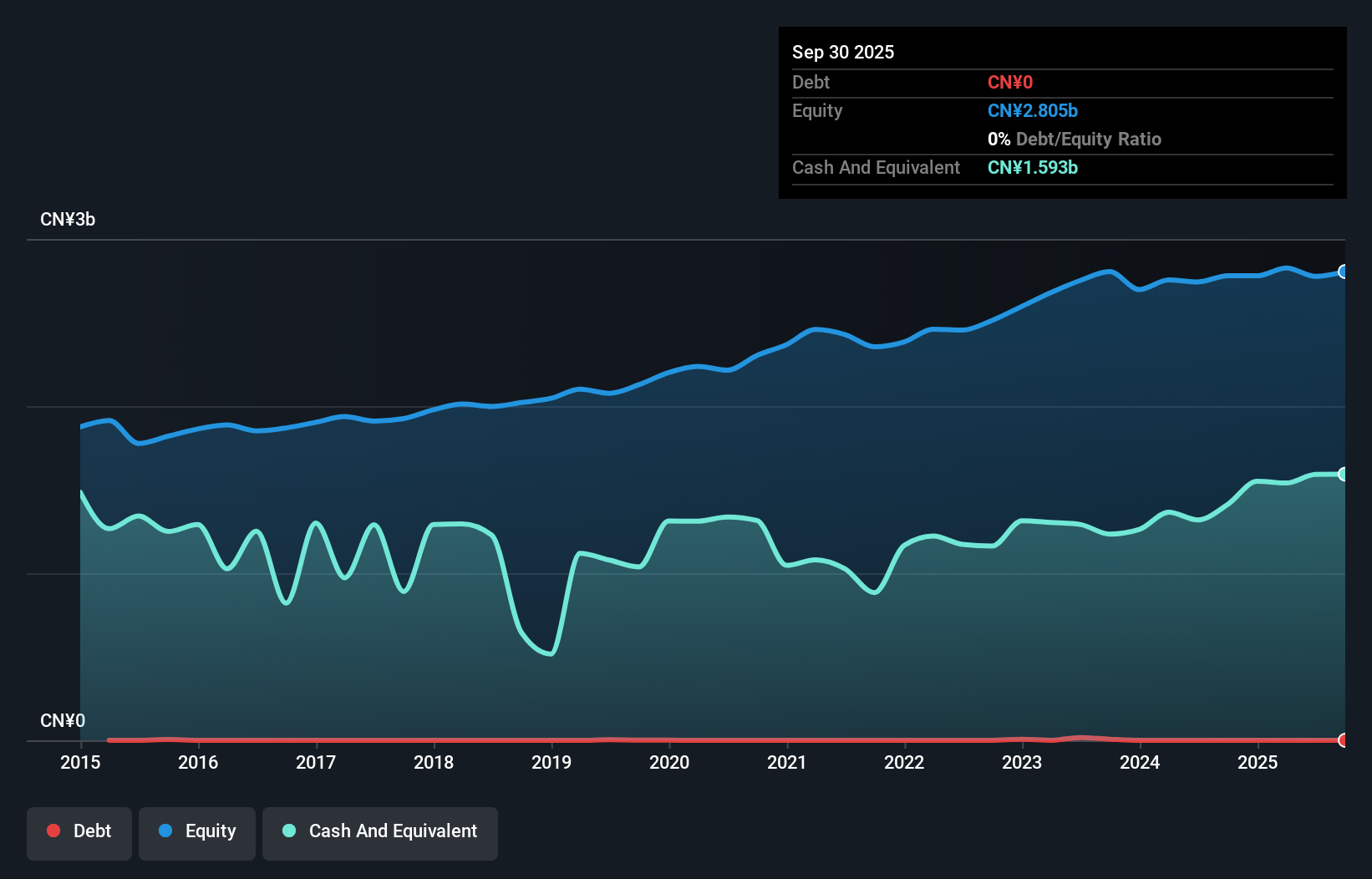

Chengdu Leejun Industrial (SZSE:002651)

Simply Wall St Value Rating: ★★★★★★

Overview: Chengdu Leejun Industrial Co., Ltd. specializes in the research, development, design, manufacturing, sales, and servicing of grinding process system equipment both within China and internationally, with a market cap of CN¥12.26 billion.

Operations: Chengdu Leejun Industrial generates revenue primarily through the sale and servicing of grinding process system equipment. The company's cost structure includes expenses related to research, development, manufacturing, and sales operations. Gross profit margin trends provide insight into the company's profitability dynamics over time.

Chengdu Leejun Industrial, a niche player in the machinery sector, has seen its earnings skyrocket by 516% over the past year, outpacing the industry's growth of 6%. Despite this impressive performance, revenue for the nine months ending September 2025 fell to CNY 487.5 million from CNY 549.99 million in the previous year, with net income also dropping to CNY 87.17 million from CNY 121.08 million. The company remains debt-free and boasts high-quality earnings but faces challenges with declining sales and net income amidst recent amendments to its corporate governance structure and credit line applications under consideration.

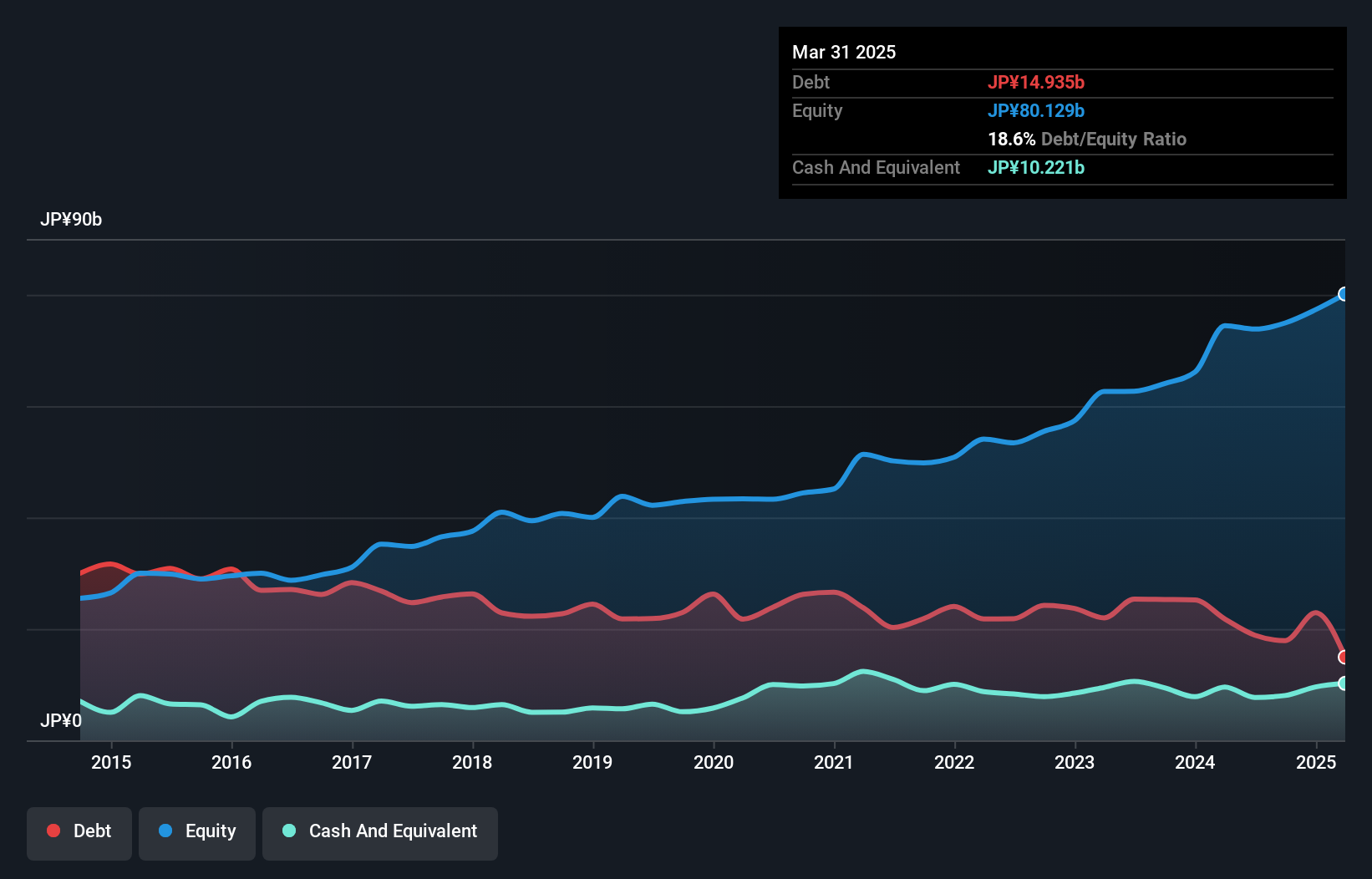

Sinfonia TechnologyLtd (TSE:6507)

Simply Wall St Value Rating: ★★★★★★

Overview: Sinfonia Technology Co., Ltd. engages in the manufacturing and sale of semiconductor, aerospace, automobile, mobility, and industrial electrical equipment with a market capitalization of ¥267.49 billion.

Operations: Sinfonia Technology generates revenue primarily from Motion Devices, Engineering & Services, Clean Conveyance System, and Power Electronics Equipment segments, with Motion Devices contributing ¥46.44 billion. The company focuses on these key areas to drive its financial performance.

Sinfonia Technology, a promising player in the electrical industry, has seen its earnings grow by 31% over the past year, outpacing the industry's 16% growth. The company boasts high-quality earnings and maintains a satisfactory net debt to equity ratio of 5.6%, reflecting sound financial management. Over five years, it has significantly reduced its debt to equity ratio from 59% to 17.6%. Despite recent share price volatility, Sinfonia remains profitable with positive free cash flow and robust interest coverage, indicating solid operational health and potential for continued growth at an anticipated annual rate of nearly 13%.

- Click here to discover the nuances of Sinfonia TechnologyLtd with our detailed analytical health report.

Explore historical data to track Sinfonia TechnologyLtd's performance over time in our Past section.

Taking Advantage

- Delve into our full catalog of 2502 Asian Undiscovered Gems With Strong Fundamentals here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com