- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

The Bull Case For Ivanhoe Electric (IE) Could Change Following Santa Cruz Progress And Ranking Boost – Learn Why

- Ivanhoe Electric recently presented at the Mines and Money @ Resourcing Tomorrow conference in London, where Vice President of Investor Relations & Business Development Mike Patterson outlined the company’s latest progress to a global mining audience.

- The company’s recognition in the November Global Mining Power Rankings, supported by advances at the US-based Santa Cruz copper project and a technology-driven exploration platform, has reinforced its profile in critical minerals and US supply chains.

- We’ll now examine how this combination of conference visibility and progress at the Santa Cruz copper project shapes Ivanhoe Electric’s investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

What Is Ivanhoe Electric's Investment Narrative?

To own Ivanhoe Electric, you have to believe in the long-term value of US-focused copper and critical minerals, backed by its Santa Cruz project and a technology-heavy exploration model, despite very limited revenue and continuing losses. The recent conference appearance and small-cap recognition do not change the hard numbers, but they do support near-term catalysts around funding access, partnerships and potential permitting momentum, especially after the recent US$150,000,000 equity raise and a strong share price run this year. On the flip side, the same visibility may sharpen scrutiny of valuation, future dilution risk and the gap between project potential and current earnings, particularly with the stock already trading on a rich price-to-book multiple and no path to profitability in consensus forecasts.

However, that long runway before any clear route to profitability is something investors should understand. The valuation report we've compiled suggests that Ivanhoe Electric's current price could be inflated.Exploring Other Perspectives

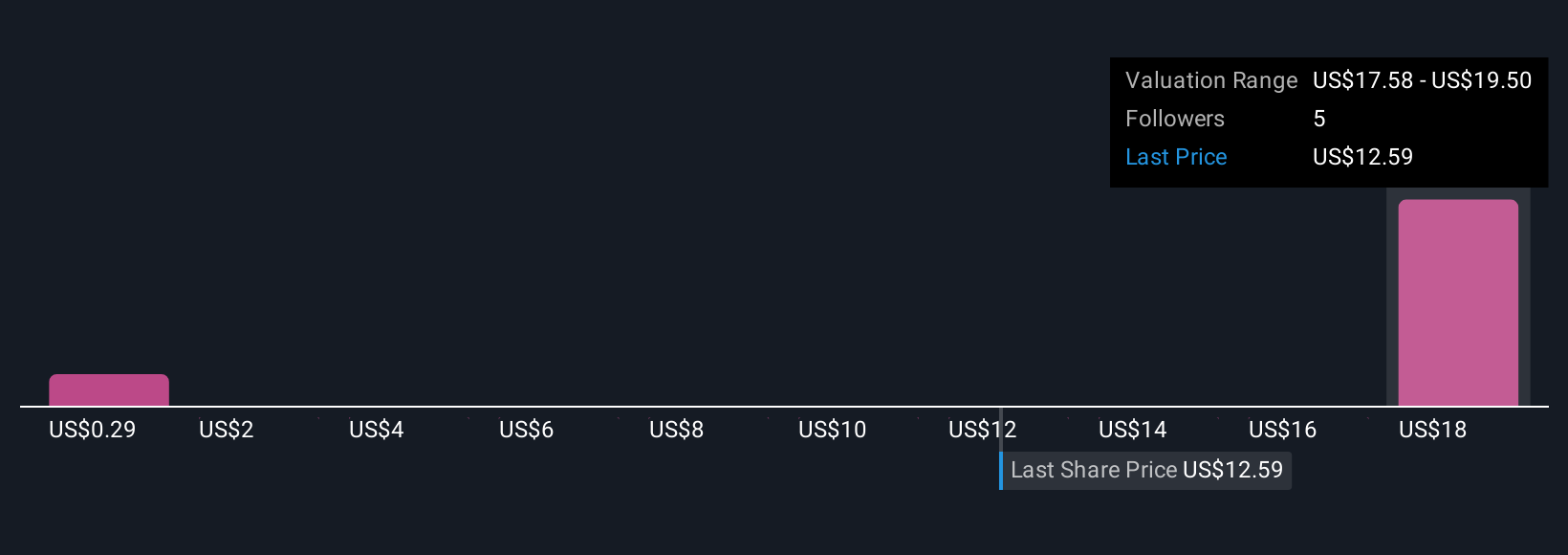

Three fair value estimates from the Simply Wall St Community span from just US$0.29 to US$19.50 per share, underlining how far apart views can be on Ivanhoe Electric. Set against a company that is still loss-making and reliant on fresh capital to advance Santa Cruz, this spread of opinions highlights why it helps to weigh several viewpoints before deciding how its story might fit into your portfolio.

Explore 3 other fair value estimates on Ivanhoe Electric - why the stock might be worth less than half the current price!

Build Your Own Ivanhoe Electric Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ivanhoe Electric research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

- Our free Ivanhoe Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ivanhoe Electric's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com