- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Has The Easy Money Already Been Made In Blackstone After Its Recent Share Price Rebound?

- Wondering if Blackstone at around $151 a share is still worth buying, or if the easy money has already been made? In this article, we walk through what the current price might really be telling us about future returns.

- Despite being down 12.9% year to date and 16.6% over the past year, the stock has bounced 4.5% in the last week and 6.0% over the past month, while still sitting on gains of 109.7% over 3 years and 186.3% over 5 years.

- Recent moves have been driven by a mix of macro headlines around interest rates, shifting expectations for private market returns, and ongoing investor appetite for alternative asset managers. At the same time, updates on fundraising pipelines and deal activity have kept Blackstone front of mind as a bellwether for the broader alternatives space.

- Yet on our framework Blackstone scores just 0/6 on undervaluation checks. This raises the question of whether traditional metrics are capturing the full story. Next, we will dig into different valuation approaches and, by the end, consider a more powerful way to judge what this stock is really worth.

Blackstone scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Blackstone Excess Returns Analysis

The Excess Returns model looks at how much profit a company can earn above its cost of equity and then projects how long those superior returns can last before fading toward a more normal level.

For Blackstone, the starting point is a Book Value of $10.72 per share and a Stable EPS of $2.80 per share, based on weighted future Return on Equity estimates from six analysts. With an Average Return on Equity of 46.20% and a Stable Book Value of $6.07 per share, the model assumes Blackstone can continue to generate strong profitability on each dollar of equity it retains.

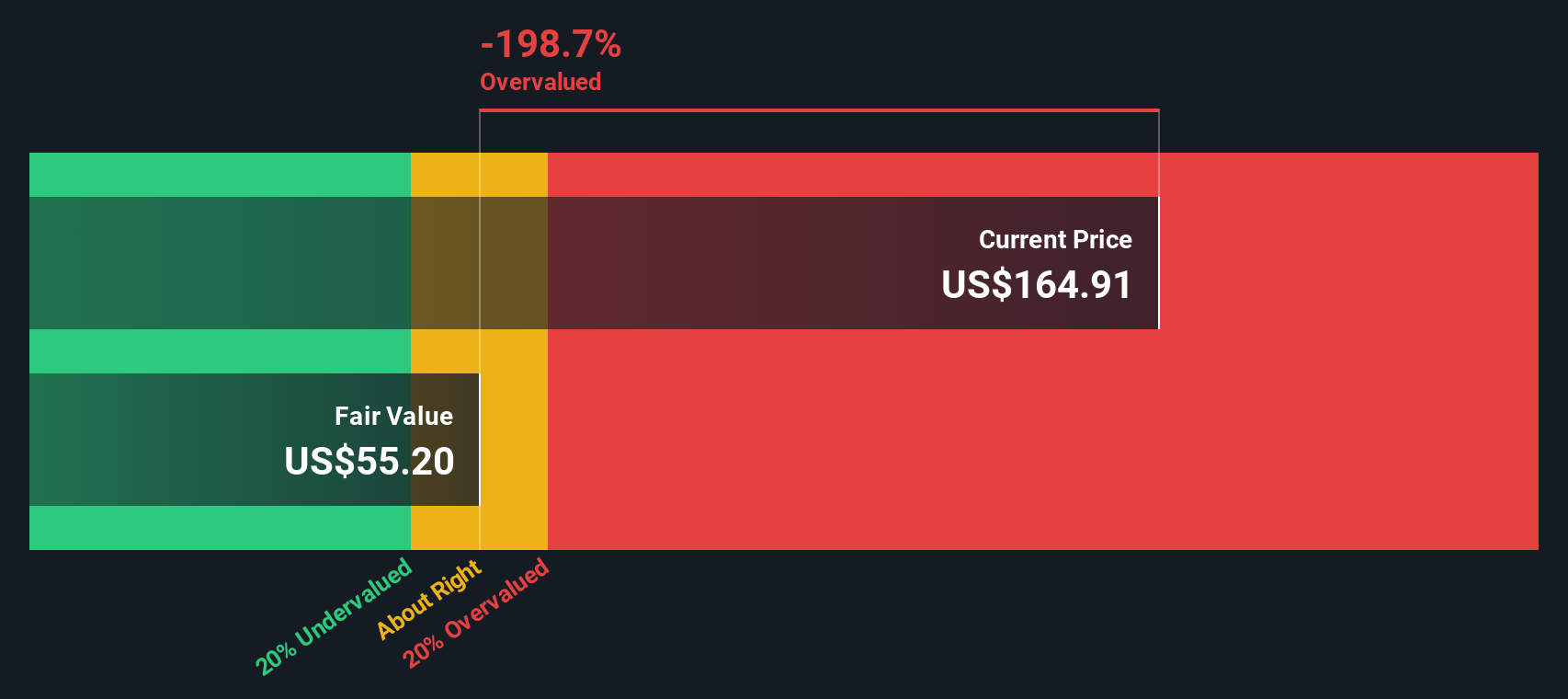

After subtracting a Cost of Equity of roughly $0.50 per share, the remaining Excess Return is about $2.30 per share. Capitalizing those excess profits over time leads to an estimated intrinsic value of roughly $51.64 per share under this framework.

Compared with the current share price near $151, the Excess Returns valuation suggests Blackstone is about 193.2% overvalued, indicating that the market is paying a steep premium for continued high returns.

Result: OVERVALUED

Our Excess Returns analysis suggests Blackstone may be overvalued by 193.2%. Discover 913 undervalued stocks or create your own screener to find better value opportunities.

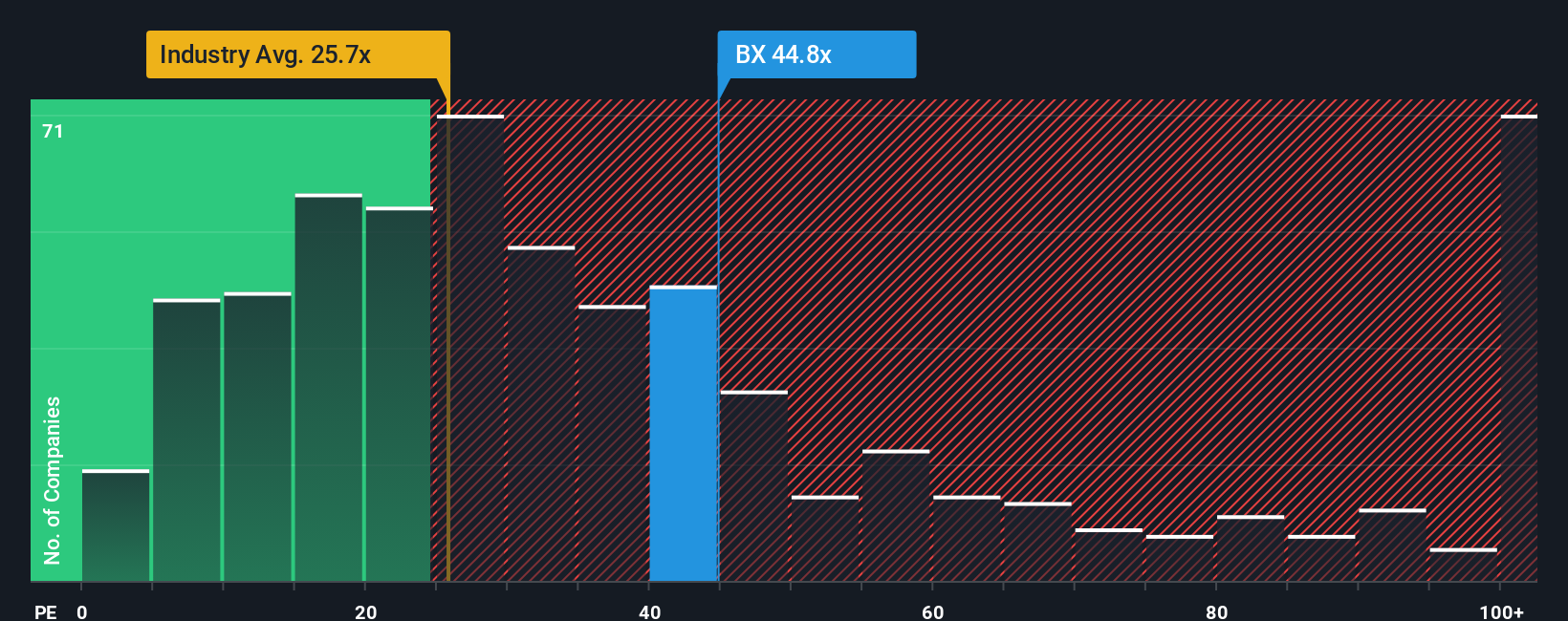

Approach 2: Blackstone Price vs Earnings

For established, profitable businesses like Blackstone, the price to earnings (PE) ratio is a useful shorthand for how much investors are willing to pay for each dollar of current earnings. It ties today’s share price directly to the company’s ability to generate profits, which ultimately funds dividends and reinvestment.

What counts as a “normal” PE largely depends on how fast earnings are expected to grow and how risky those earnings are. Faster, more predictable growth can justify a higher multiple, while cyclicality or uncertainty should pull it lower. Today, Blackstone trades at about 43.76x earnings, well above both the Capital Markets industry average of roughly 24.00x and the peer average near 37.46x.

Simply Wall St’s proprietary Fair Ratio for Blackstone is 24.41x. This estimates the multiple the stock should command after considering its earnings growth outlook, profitability, risk profile, industry and market cap. This tailored benchmark is more informative than a simple comparison with peers or the sector because it adjusts for Blackstone’s specific strengths and risk factors. With the current PE sitting far above the 24.41x Fair Ratio, the shares screen as materially overvalued on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Blackstone Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach your story about Blackstone to the key numbers like future revenue, earnings, margins and the fair value you think is reasonable.

A Narrative on Simply Wall St links three things together: the business story you believe, the financial forecast that flows from that story, and the resulting fair value that lets you compare your view with the current share price.

Because Narratives live on the Community page of Simply Wall St and are already used by millions of investors, they are easy to create and update. The platform automatically refreshes the forecasts and fair values when new information such as earnings reports or major news hits the market.

This means you can quickly see how your Narrative’s fair value for Blackstone compares to today’s share price, and you can also see how other investors’ Narratives range from more bullish fair values around $193 per share to more cautious ones closer to $125 per share.

For Blackstone however we will make it really easy for you with previews of two leading Blackstone Narratives:

Fair value: $179.78 per share

Upside versus last close: 15.8% below fair value

Forecast revenue growth: 19.67% per year

- Assumes strong fundraising momentum, with tens of billions in new inflows and over $170 billion in dry powder supporting long term deployment into undervalued assets.

- Leans on growth in private credit and private wealth channels, where strategic alliances and product innovation are expected to expand margins and diversify revenue.

- Sees near term macro and geopolitical risks as manageable, with analysts expecting revenue, earnings and margins to rise enough to justify a modest premium PE multiple by 2028.

Fair value: $124.55 per share

Downside versus last close: 21.5% above fair value

Forecast revenue growth: 15.85% per year

- Highlights execution and efficiency risks as Blackstone scales infrastructure and private wealth, where upfront costs and complexity could squeeze future profitability.

- Assumes fewer attractive large scale deals and heightened sensitivity to interest rates, inflation and real estate cycles, leading to a lower justified PE multiple.

- Recognizes that the underlying businesses can still grow earnings meaningfully, but argues that today’s price already embeds overly optimistic expectations for 2028.

Do you think there's more to the story for Blackstone? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com