- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Should Asahi’s Cyberattack‑Driven FY2025 Earnings Delay Require Action From Asahi Group Holdings (TSE:2502) Investors?

- In late November 2025, Asahi Group Holdings announced it was postponing the release of its FY2025 financial results after an October cyberattack disrupted its systems and delayed year‑end closing procedures and audits.

- This delay highlights how operational resilience and cybersecurity preparedness can become central issues for investors assessing a consumer staples group’s risk profile and disclosure reliability.

- We’ll now explore how the cyberattack‑driven postponement of Asahi’s earnings release may reshape the company’s investment narrative and perceived risk.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

What Is Asahi Group Holdings' Investment Narrative?

To be comfortable as an Asahi shareholder, you really need to believe in the long-term durability of its global beer and beverage franchises, steady (if modest) earnings growth and a consistent dividend, even if returns are not spectacular. Before the cyberattack, near-term catalysts were fairly straightforward: delivery against 2025 guidance, execution on the sizeable share buyback authorization and continued progress on integrating past acquisitions while managing a high debt load. The results delay now puts more weight on operational resilience and internal controls, at least in the short run, and raises questions about whether management will keep to its original capital return timetable, given the buyback had barely started. For many investors, the incident will be less about immediate financial damage and more about confidence in risk management.

However, there is a separate operational risk that investors should have on their radar. Despite retreating, Asahi Group Holdings' shares might still be trading above their fair value and there could be some more downside. Discover how much.Exploring Other Perspectives

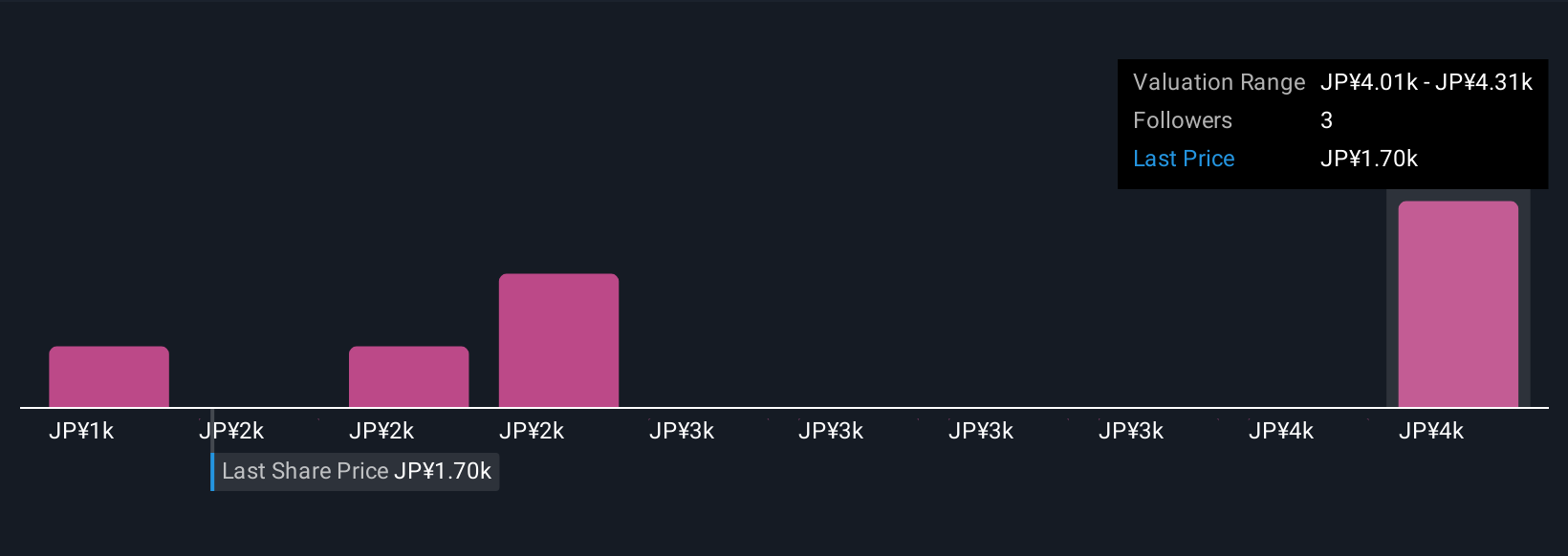

Four fair value estimates from the Simply Wall St Community span roughly ¥1,330 to nearly ¥4,616, highlighting how differently private investors view Asahi’s prospects. Set that alongside the recent cyberattack, which pulls operational risk and disclosure timing into sharper focus, and you have a company where both perceived upside and execution questions are front of mind for many market participants.

Explore 4 other fair value estimates on Asahi Group Holdings - why the stock might be worth over 2x more than the current price!

Build Your Own Asahi Group Holdings Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Asahi Group Holdings research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Asahi Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Asahi Group Holdings' overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com