- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Curbline Properties (CURB) Valuation Check After KeyBanc Upgrade and Double-Digit AFFO Growth Outlook

KeyBanc’s upgrade of Curbline Properties (CURB) is drawing fresh attention, as the firm points to double digit AFFO growth, high occupancy, and lower capital spending needs that could support steadier cash flows.

See our latest analysis for Curbline Properties.

Even with the latest share price sitting at $23.65, Curbline’s roughly 3% 3 month share price return and modest 1 year total shareholder return suggest momentum is picking up rather than fading as investors reassess its cash flow potential.

If KeyBanc’s upgrade has you rethinking this corner of real estate, it could be a good moment to broaden your search and discover fast growing stocks with high insider ownership.

With shares still trading at a notable discount to analyst targets despite brisk revenue growth and high occupancy, should investors view Curbline as quietly undervalued or assume the market is already pricing in its next leg of growth?

Price-to-Earnings of 60.7x: Is it justified?

Curbline Properties screens as significantly overvalued on traditional earnings metrics, with a 60.7x price-to-earnings ratio at the last close of $23.65.

The price-to-earnings multiple compares what investors pay today for each dollar of current earnings, a key yardstick for REITs where recurring profit is closely watched. At 60.7x, the market is effectively placing a steep premium on Curbline's current earnings power, implying that investors expect either sustained growth or structurally higher profitability than history suggests.

That premium looks stretched when set against several benchmarks. The SWS fair price-to-earnings ratio for Curbline is 30.7x, meaning the current multiple is roughly double the level our fair ratio analysis points to as more reasonable. It is also higher than both the peer average of 57.3x and the broader US Retail REITs industry average of 26.6x, underscoring that the market is pricing in much richer earnings expectations for Curbline than for its typical sector peer.

Explore the SWS fair ratio for Curbline Properties

Result: Price-to-Earnings of 60.7x (OVERVALUED)

However, softer net income trends, combined with a still rich valuation, leave little margin for error if revenue momentum stalls or leasing conditions tighten.

Find out about the key risks to this Curbline Properties narrative.

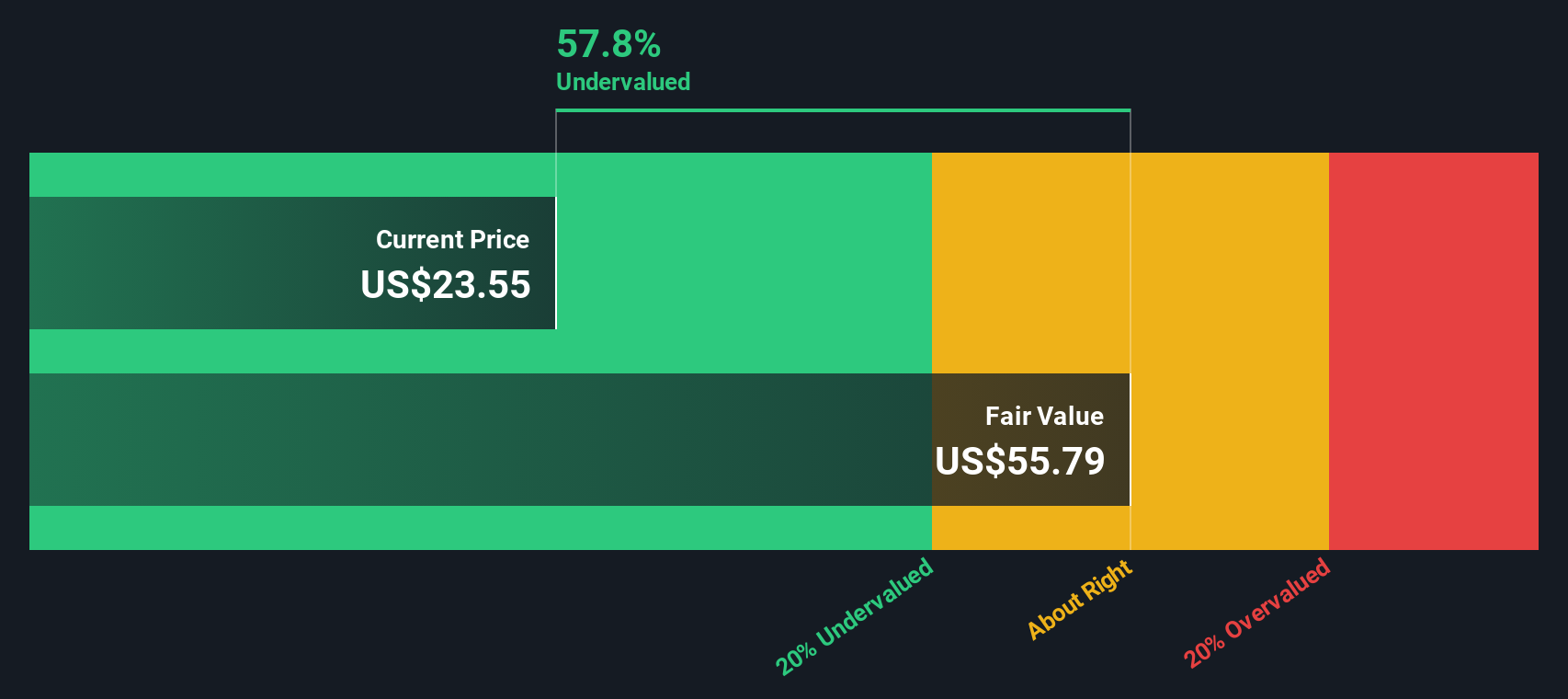

Another View: DCF Points to Deep Value

Our DCF model tells a very different story, suggesting fair value near $56.64 versus today’s $23.65 share price. That implies Curbline could be trading at a steep discount, even as earnings are expected to edge lower. Is the market being too cautious about future cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Curbline Properties for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 909 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Curbline Properties Narrative

If our take does not quite match your own view, dive into the numbers yourself and craft a customized storyline in just minutes, Do it your way.

A great starting point for your Curbline Properties research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Do not stop at Curbline when the rest of the market is full of overlooked opportunities. Let Simply Wall St’s screener surface your next high conviction idea.

- Capture potential growth stories early by using these 3572 penny stocks with strong financials that pair smaller market caps with solid fundamentals.

- Position yourself within the AI trend with these 26 AI penny stocks targeting companies building the next generation of intelligent technology.

- Explore value opportunities before they become widely followed through these 909 undervalued stocks based on cash flows that highlight cash flow profiles trading at compelling prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com