- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

How UPS’s Margin-Focused Overhaul and Higher Debt Will Impact United Parcel Service (UPS) Investors

- In recent months, United Parcel Service has accelerated a major restructuring, cutting jobs, closing warehouses, and shifting away from low-margin Amazon deliveries while emphasizing higher-margin healthcare and small-business customers, even as package volumes have softened post-pandemic.

- An important angle for investors is that management is prioritizing margin improvement and dividend continuity, which may require higher net debt in the near term as cash flow feels the strain of the overhaul.

- Next, we’ll examine how UPS’s aggressive cost-cutting and pivot toward higher-margin healthcare and small-business clients shapes its broader investment narrative.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

United Parcel Service Investment Narrative Recap

To own UPS today, you need to believe its overhaul can turn a mature, volume-driven shipper into a leaner, higher-margin logistics platform, even as overall package demand stays muted. The recent restructuring news reinforces the key near term catalyst: whether cost cuts and mix shift can offset weaker volumes and Amazon pullback. The biggest current risk is that execution missteps and softer cash flow, including higher net debt to sustain the dividend, undermine that margin-focused plan.

Among recent announcements, the repeated affirmation of the quarterly US$1.64 dividend and guidance for about US$5.5 billion in 2025 payouts is most relevant here. It highlights management’s emphasis on income stability at a time when earnings and free cash flow are under pressure from network reconfiguration, making dividend funding and balance sheet flexibility central to the short term thesis around UPS’s restructuring.

But investors should also weigh how this commitment to the dividend could strain UPS if...

Read the full narrative on United Parcel Service (it's free!)

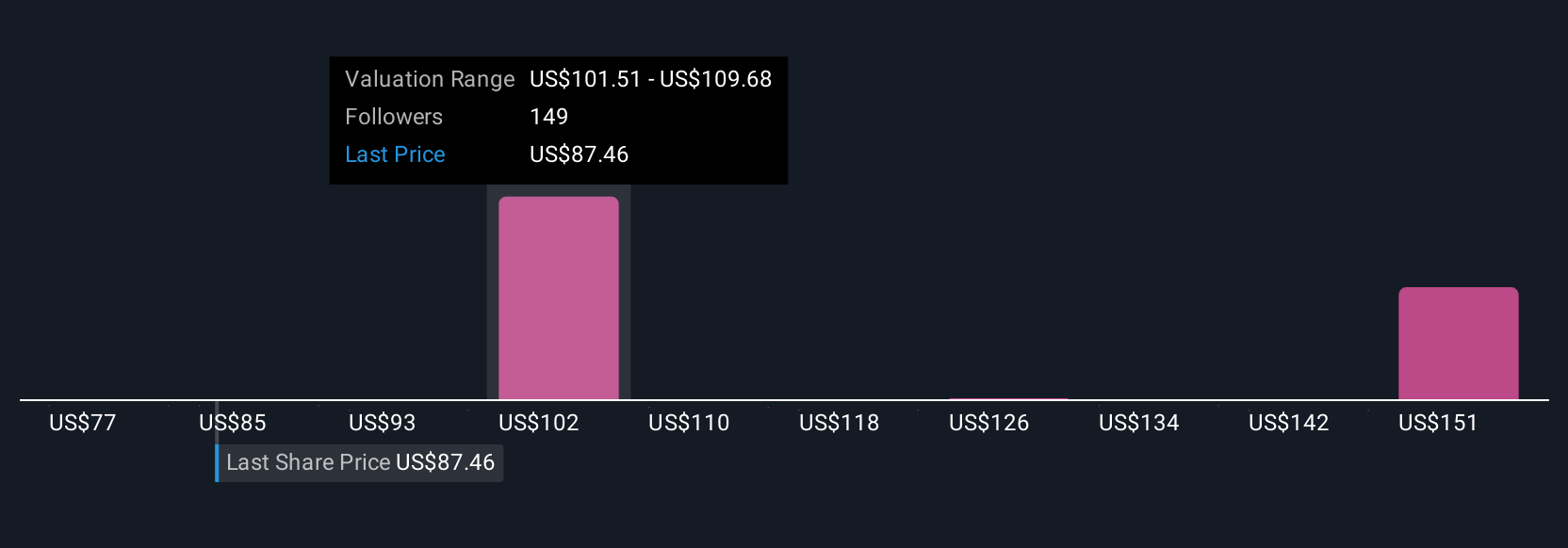

United Parcel Service's narrative projects $94.5 billion revenue and $7.1 billion earnings by 2028. This requires 1.5% yearly revenue growth and a $1.4 billion earnings increase from $5.7 billion today.

Uncover how United Parcel Service's forecasts yield a $100.50 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting UPS to lift earnings toward about US$8.0 billion by 2028, yet the latest restructuring news and rising competitive pressures suggest those upbeat margin and volume assumptions, including risks from tech-driven rivals and insourcing, may need a fresh look.

Explore 22 other fair value estimates on United Parcel Service - why the stock might be worth as much as 44% more than the current price!

Build Your Own United Parcel Service Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your United Parcel Service research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free United Parcel Service research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate United Parcel Service's overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com