- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Not Many Are Piling Into Transtema Group AB (STO:TRANS) Stock Yet As It Plummets 26%

To the annoyance of some shareholders, Transtema Group AB (STO:TRANS) shares are down a considerable 26% in the last month, which continues a horrid run for the company. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 45% share price drop.

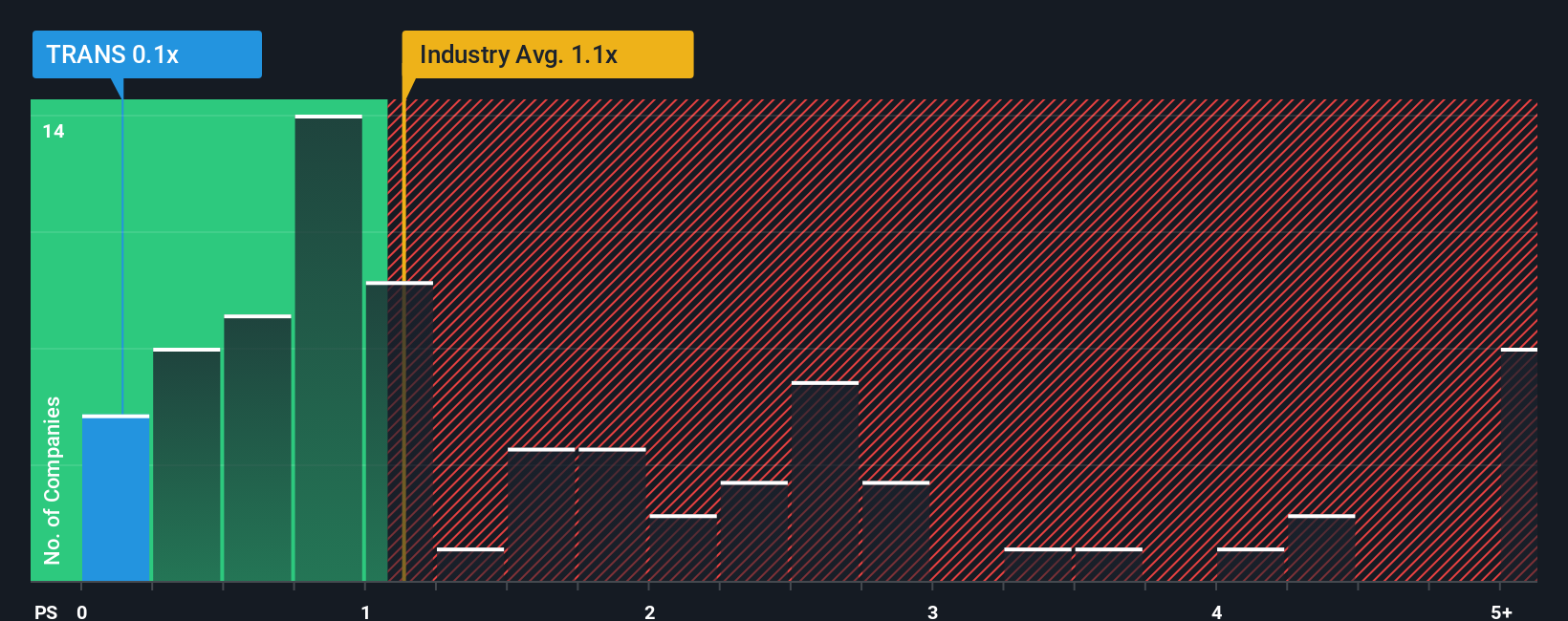

Although its price has dipped substantially, Transtema Group's price-to-sales (or "P/S") ratio of 0.1x might still make it look like a buy right now compared to the Telecom industry in Sweden, where around half of the companies have P/S ratios above 1.8x and even P/S above 5x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

See our latest analysis for Transtema Group

How Transtema Group Has Been Performing

Recent revenue growth for Transtema Group has been in line with the industry. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. Those who are bullish on Transtema Group will be hoping that this isn't the case.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Transtema Group.How Is Transtema Group's Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Transtema Group's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 10% last year. The solid recent performance means it was also able to grow revenue by 24% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Looking ahead now, revenue is anticipated to climb by 0.008% per annum during the coming three years according to the dual analysts following the company. That's shaping up to be similar to the 1.7% each year growth forecast for the broader industry.

With this in consideration, we find it intriguing that Transtema Group's P/S is lagging behind its industry peers. It may be that most investors are not convinced the company can achieve future growth expectations.

What We Can Learn From Transtema Group's P/S?

The southerly movements of Transtema Group's shares means its P/S is now sitting at a pretty low level. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our examination of Transtema Group's revealed that its P/S remains low despite analyst forecasts of revenue growth matching the wider industry. When we see middle-of-the-road revenue growth like this, we assume it must be the potential risks that are what is placing pressure on the P/S ratio. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

We don't want to rain on the parade too much, but we did also find 4 warning signs for Transtema Group (1 can't be ignored!) that you need to be mindful of.

If you're unsure about the strength of Transtema Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.