- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

The Bull Case For General Mills (GIS) Could Change Following Rising Scrutiny Of Its Food Pricing Practices

- Earlier this week, packaged foods maker General Mills came under increased government scrutiny over food pricing practices, amid concerns that it has leaned on price hikes to offset two years of declining unit sales and faces added pressure from expanded tariff quotas on key ingredients such as sugar.

- This combination of weaker volumes and rising regulatory focus on how food companies set prices has put a spotlight on the resilience and flexibility of General Mills’ current business model.

- Next, we’ll explore how rising government scrutiny of food pricing could influence General Mills’ existing investment narrative and risk profile.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

General Mills Investment Narrative Recap

To own General Mills, you need to believe its core brands and marketing investments can offset soft volumes and a value focused consumer. The latest pricing scrutiny and tariff quota changes mainly reinforce an existing key risk that margin support from price increases could be harder to sustain, but they do not fundamentally alter the near term catalyst of heavier reinvestment in marketing and innovation to stabilize volumes.

The most relevant recent update is management’s plan for at least 5% Holistic Margin Management savings and an extra US$100 million of cost savings in fiscal 2026. Against a backdrop of regulatory attention on pricing, this efficiency push matters because it gives General Mills more room to adjust promotions and price points while still funding product innovation, even if it delays visible improvement in reported margins.

Yet investors should be aware that if regulatory and consumer pressures limit pricing flexibility, the company’s ability to fund its marketing led volume recovery strategy could...

Read the full narrative on General Mills (it's free!)

General Mills' narrative projects $19.0 billion revenue and $2.1 billion earnings by 2028. This implies a 0.8% yearly revenue decline and a $0.2 billion earnings decrease from $2.3 billion today.

Uncover how General Mills' forecasts yield a $53.89 fair value, a 17% upside to its current price.

Exploring Other Perspectives

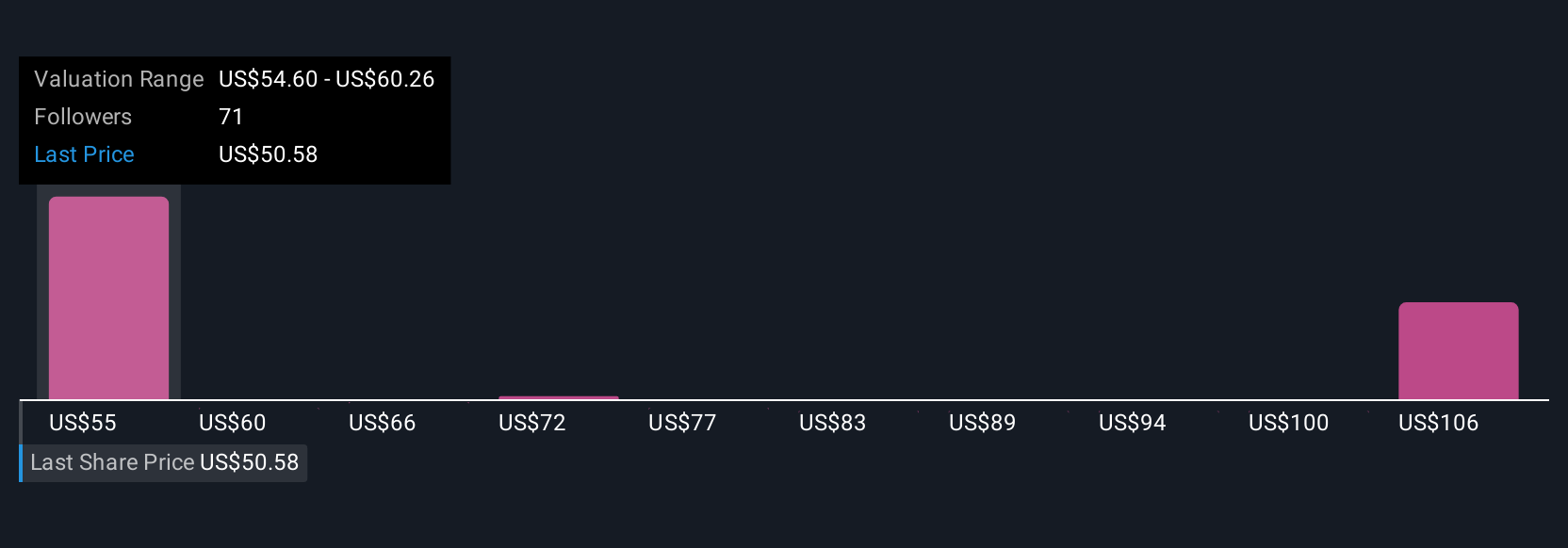

Six fair value estimates from the Simply Wall St Community span about US$53 to US$104 per share, highlighting how differently individual investors assess General Mills. You can weigh those views against the risk that tighter scrutiny of food pricing could constrain the company’s ability to use price increases to support earnings, with important implications for how resilient its current business model really is.

Explore 6 other fair value estimates on General Mills - why the stock might be worth over 2x more than the current price!

Build Your Own General Mills Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your General Mills research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free General Mills research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Mills' overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com