- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Does Regulatory Tailwinds and User Growth Shift the Bull Case for Rush Street Interactive (RSI)?

- Rush Street Interactive recently reported its twelfth consecutive quarter of surpassing revenue and EBITDA expectations, driven by expanding its user base and entering new markets, notably in Latin America.

- New regulatory developments, such as the anticipated removal of VAT in Colombia and the introduction of iGaming in Alberta, are set to provide meaningful growth catalysts for the company.

- Next, we will explore how these regulatory changes and sustained user growth could affect Rush Street Interactive's investment narrative.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Rush Street Interactive Investment Narrative Recap

To be a shareholder in Rush Street Interactive, you need to believe the company can maintain high user growth and capitalize on online casino expansion amid ongoing regulatory change. The recent earnings beat underlines current momentum, especially in Latin America, but near-term revenue and profit are still largely tied to effective executions in key new markets and the risk of sudden regulatory changes that could impact margins. While strong quarterly results help affirm management's outlook, the risk of renewed taxes or shifting regulations remains a material consideration for the business.

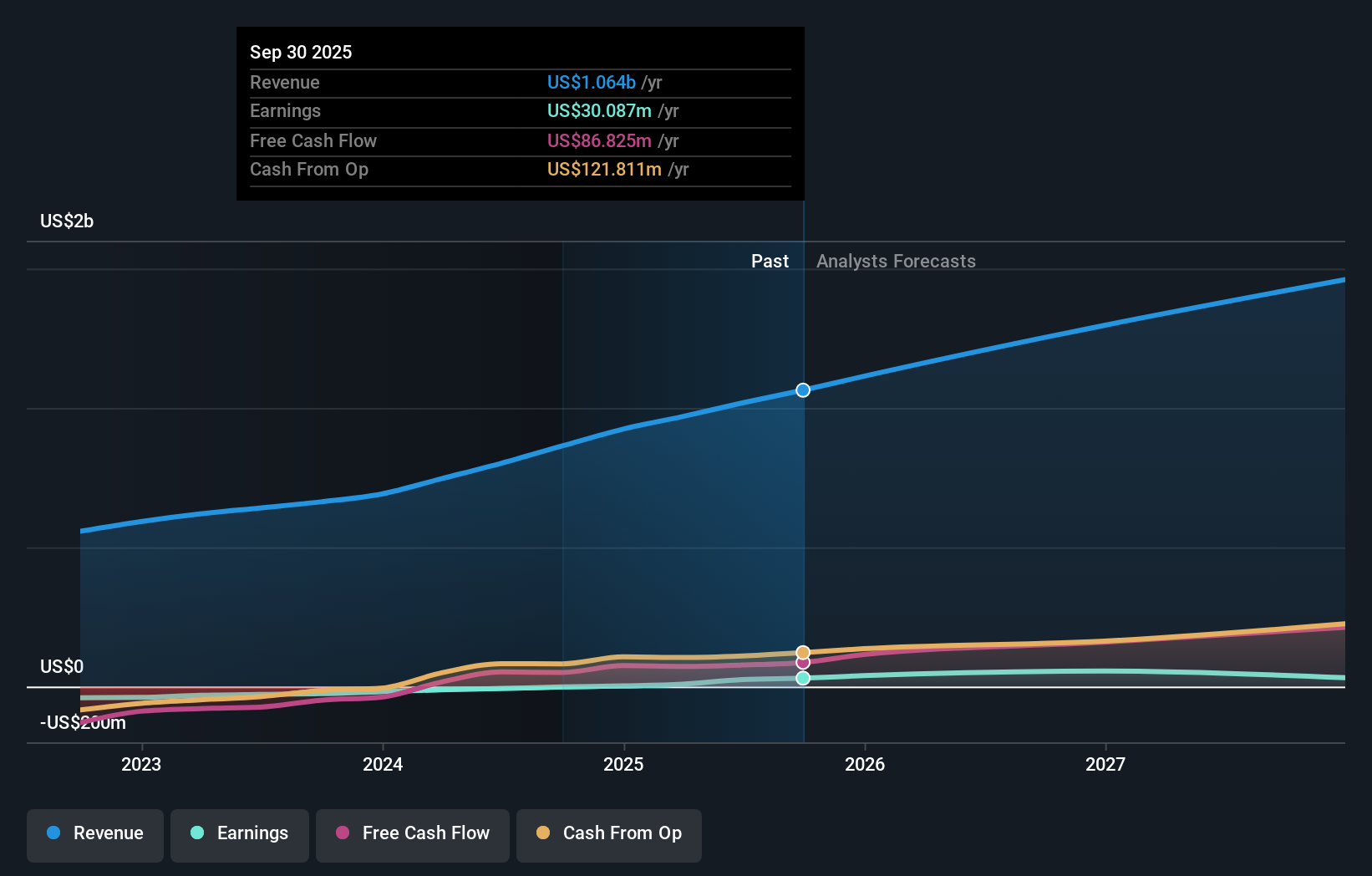

The most relevant company announcement to recent developments is the raised 2025 revenue guidance to US$1,100 to US$1,120 million, reflecting management’s confidence in continued expansion and the anticipated impact of catalysts like the removal of Colombia's VAT. This improvement in outlook sets expectations for future quarters, but much depends on consistent user acquisition and stable regulatory frameworks in major geographies.

However, investors should also be aware that if renewed tax measures or regulatory reversals occur, especially in growing markets like Colombia, the company’s margin expansion story may face...

Read the full narrative on Rush Street Interactive (it's free!)

Rush Street Interactive's narrative projects $1.5 billion in revenue and $44.7 million in earnings by 2028. This requires 13.2% yearly revenue growth and a $19.5 million earnings increase from $25.2 million.

Uncover how Rush Street Interactive's forecasts yield a $22.86 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Fair value estimates from two members of the Simply Wall St Community range from US$22.86 to US$27.07 per share, highlighting varied personal outlooks on future growth. In light of ongoing regulatory shifts in core markets, you may want to explore these different perspectives and see how they could shape the future for Rush Street Interactive.

Explore 2 other fair value estimates on Rush Street Interactive - why the stock might be worth as much as 57% more than the current price!

Build Your Own Rush Street Interactive Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Rush Street Interactive research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Rush Street Interactive research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Rush Street Interactive's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com