- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Fresh Look at Horace Mann Educators (HMN) Valuation Following Strong Earnings and Dividend Growth

Horace Mann Educators (HMN) delivered an earnings report that beat market forecasts for the third quarter, with both earnings per share and revenue outpacing estimates. Investors are also taking note of the company’s steady dividend track record.

See our latest analysis for Horace Mann Educators.

Horace Mann Educators’ strong quarterly results and unwavering dividend growth have helped reinforce positive sentiment. The share price has climbed 18.8% year-to-date and delivered a 17.3% total return over the past year. The momentum appears steady, especially as investors look for consistent performers in the insurance space.

If solid execution and reliable dividends appeal to you, this could be the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With such robust returns and a long-standing record of dividend growth, investors may wonder if Horace Mann Educators is still undervalued or if the recent share price rally means future growth is already reflected in the price.

Most Popular Narrative: 8.7% Undervalued

With Horace Mann Educators' most widely followed narrative placing fair value at $50.33, the current price of $45.95 suggests there is still room for the shares to run, even after a strong year. The stage is set for continued upside if the company can convert its strategic investments into persistent growth and margin expansion.

Ongoing expansion of digital engagement platforms and proprietary technology solutions (such as the Catalyst lead management system) are improving agent productivity and making it easier for educators to engage. This is likely to drive increased policy sales, higher customer conversion rates, and improved customer retention, positively impacting both revenue growth and net margins.

Want to know why this narrative favors higher value? Hint: it all comes down to the numbers behind bold growth bets, future profitability, and a forecast margin lift. What assumptions fuel these expectations? Follow the story to see the numbers that analysts believe could push this stock higher.

Result: Fair Value of $50.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy reliance on an aging educator base and increasing climate-related catastrophe risks could threaten Horace Mann's growth story in the coming years.

Find out about the key risks to this Horace Mann Educators narrative.

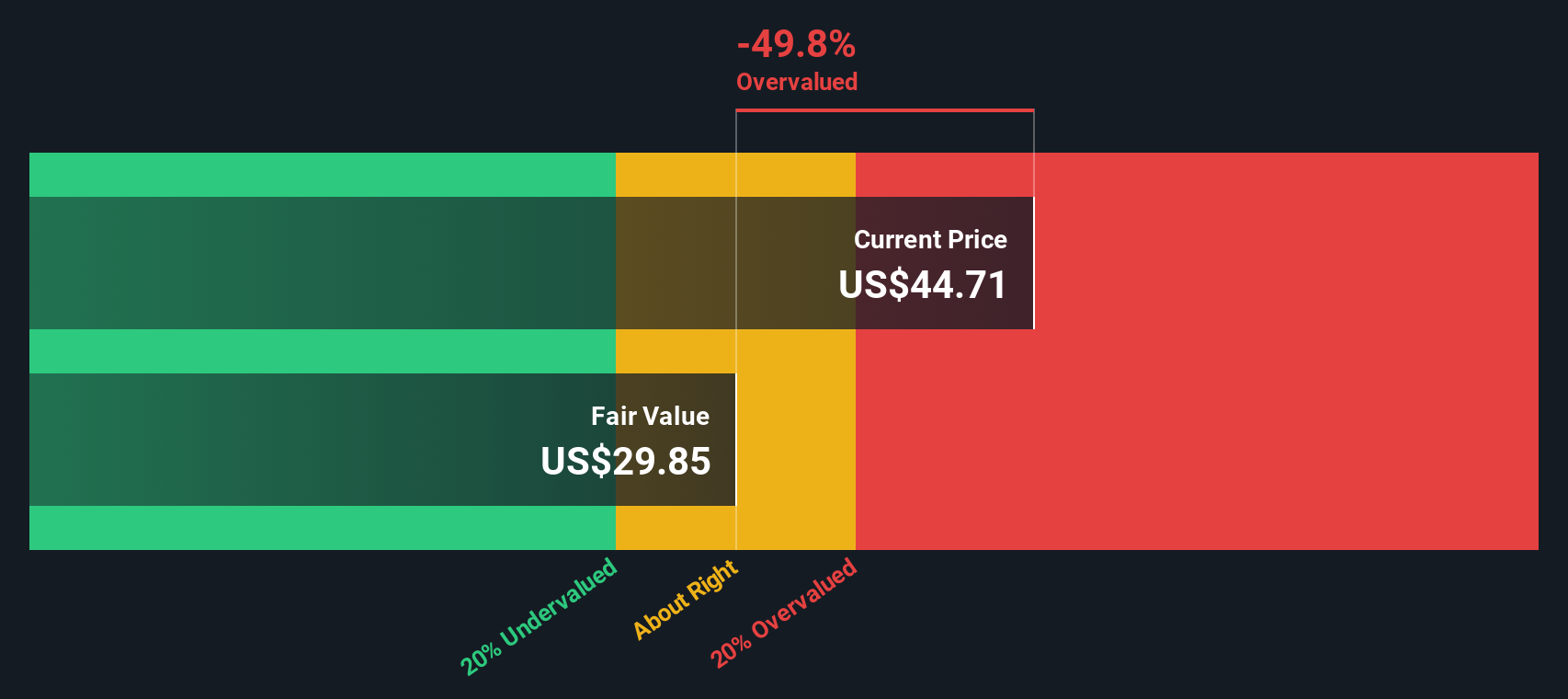

Another View: Our DCF Model Shows Less Upside

Taking a different approach, our DCF model values Horace Mann Educators at $33.30 per share. This is below the current market price. This method incorporates long-term cash flow forecasts, bringing a more conservative angle that suggests the stock may be priced a little ahead of its fundamentals.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Horace Mann Educators for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 907 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Horace Mann Educators Narrative

If you want a fresh perspective or wish to reach your own conclusions, you can dig into the data and shape your own story in just minutes, then Do it your way

A great starting point for your Horace Mann Educators research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors don't stop at a single opportunity, and neither should you. Uncover fresh companies and untapped trends with specialized stock screens right now.

- Uncover companies with robust cash flows and low market expectations by checking out these 907 undervalued stocks based on cash flows for stocks priced below their true value.

- Expand your exposure to cutting-edge technologies by reviewing these 27 AI penny stocks. These focus on artificial intelligence, automation, and data technology breakthroughs.

- Strengthen your portfolio with reliable income by targeting these 18 dividend stocks with yields > 3%, which features companies offering yields over 3% and a history of rewarding shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com