- LIVE QUOTES

- LEARN

- HELP

EN

A Fresh Look at TSMC’s (NYSE:TSM) Valuation as Share Price Momentum Cools

See our latest analysis for Taiwan Semiconductor Manufacturing.

While Taiwan Semiconductor Manufacturing’s share price has cooled a little this month, momentum remains strong in the bigger picture. The stock has delivered a robust 90-day share price return of nearly 18 percent and an exceptional 54.8 percent total shareholder return over the past year, highlighting ongoing optimism about both growth potential and long-term valuation.

If the current wave of semiconductor innovation has you looking for more, this is the perfect moment to check out the See the full list for free..

But with its share price surge and soaring returns, does Taiwan Semiconductor Manufacturing still have room to run, or are investors already paying a premium for its projected future growth?

Most Popular Narrative: 8.1% Undervalued

Taiwan Semiconductor Manufacturing’s last close at $284.82 is well below the narrative’s fair value, which stands at $310. According to oscargarcia, this price gap reflects optimism around AI-driven momentum. However, it depends on the company’s ability to execute at scale as it expands into new markets and aims to sustain growth.

TSMC is the central pillar of the global semiconductor ecosystem, powering the AI revolution with unmatched scale, cutting-edge process technology, and disciplined execution. With record profits, a dominant client base, and massive expansion underway in Taiwan and abroad, it is seen as a low-risk way to gain exposure to AI infrastructure. Although geopolitical and trade risks are present, TSMC's moat, margins, and market position provide a rare combination of growth, profitability, and stability.

Ever wondered what numbers justify this valuation edge? The narrative highlights expectations for strong margins, next-generation revenue growth, and confidence in structural industry leadership. Want the details that drive this bold upside call? Delve into the full narrative for the key assumptions behind that price target.

Result: Fair Value of $310 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, elevated valuations and rising geopolitical tensions could quickly shift sentiment and present real challenges for Taiwan Semiconductor Manufacturing’s bullish narrative.

Find out about the key risks to this Taiwan Semiconductor Manufacturing narrative.

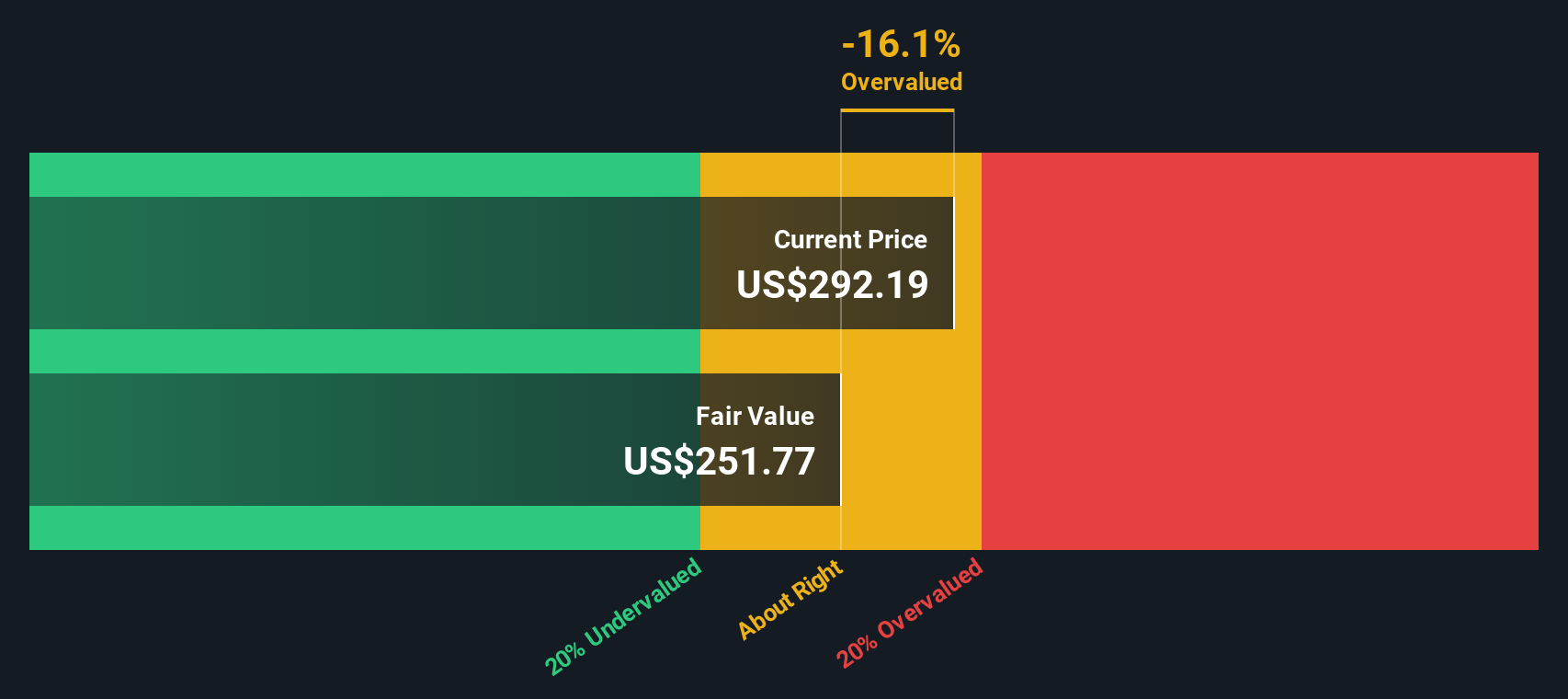

Another View: DCF Points to Overvaluation

Taking a different perspective, our DCF model currently suggests Taiwan Semiconductor Manufacturing could be trading above its fair value estimate. This is based on a more conservative forecast of future cash flows and presents a challenge to the bullish narrative from multiples, especially if growth expectations soften.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Taiwan Semiconductor Manufacturing for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 886 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Taiwan Semiconductor Manufacturing Narrative

If you see things differently or want to dig into the numbers yourself, it takes less than three minutes to put together your own story. Do it your way.

A great starting point for your Taiwan Semiconductor Manufacturing research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don't let opportunity pass you by. Turn your curiosity into smarter investing by checking out stocks that match unique growth, value, and innovation angles right now.

- Capitalize on tomorrow’s game-changers by targeting these 25 AI penny stocks poised to benefit from AI’s explosive growth and shape the digital future.

- Maximize your portfolio’s upside by uncovering these 886 undervalued stocks based on cash flows that trade for less than their cash flow potential suggests. This approach can give you an edge in spotting value.

- Supercharge your returns with these 16 dividend stocks with yields > 3% offering yields above 3 percent, ideal for investors seeking a strong foundation of reliable passive income.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com