- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Figma (FIG): Assessing the Company's Value After Significant Share Price Decline

Figma (FIG) shares have caught the attention of investors after recent trading activity pushed the stock further away from its earlier spring highs. The conversation now centers on how the company’s fundamentals align with evolving market sentiment.

See our latest analysis for Figma.

Figma's share price momentum has cooled considerably, with a sharp 30-day share price return of -37.75% and a steep year-to-date drop of -61.69%. These moves suggest that, despite the company’s earlier growth buzz, market confidence is fading and risks around future valuation are now weighing more heavily than before.

If Figma's shifting fortunes have you rethinking your strategy, this could be the perfect prompt to discover fast growing stocks with high insider ownership.

With shares trading far below analyst price targets, yet core metrics like revenue and net income still growing, investors have to wonder: is Figma now undervalued, or is the market accurately pricing in its future prospects?

Most Popular Narrative: 32.6% Undervalued

Figma’s most followed narrative suggests that its fair value could be considerably higher than the current share price. This indicates major upside according to its most vocal bulls. This perspective sees the company’s platform and expansion as key to justifying a premium in the market.

AI-driven product expansion: Buzz, Make, Sites, Slides, and Draw launched with AI features and deep integration. Enterprise adoption: 13M+ active users and approximately 95% of Fortune 500 companies use Figma.

Wondering what powers this eye-catching price target? It is not just growth. The narrative leans on improved margins and bold assumptions about where enterprise adoption and integration can take Figma next. Click through to unpack the surprising projections that drive this value call.

Result: Fair Value of $65.7 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slower growth or stronger competition in AI features could quickly dull Figma’s edge and challenge the optimistic outlook some analysts hold.

Find out about the key risks to this Figma narrative.

Another View: A Different Lens on Figma’s Value

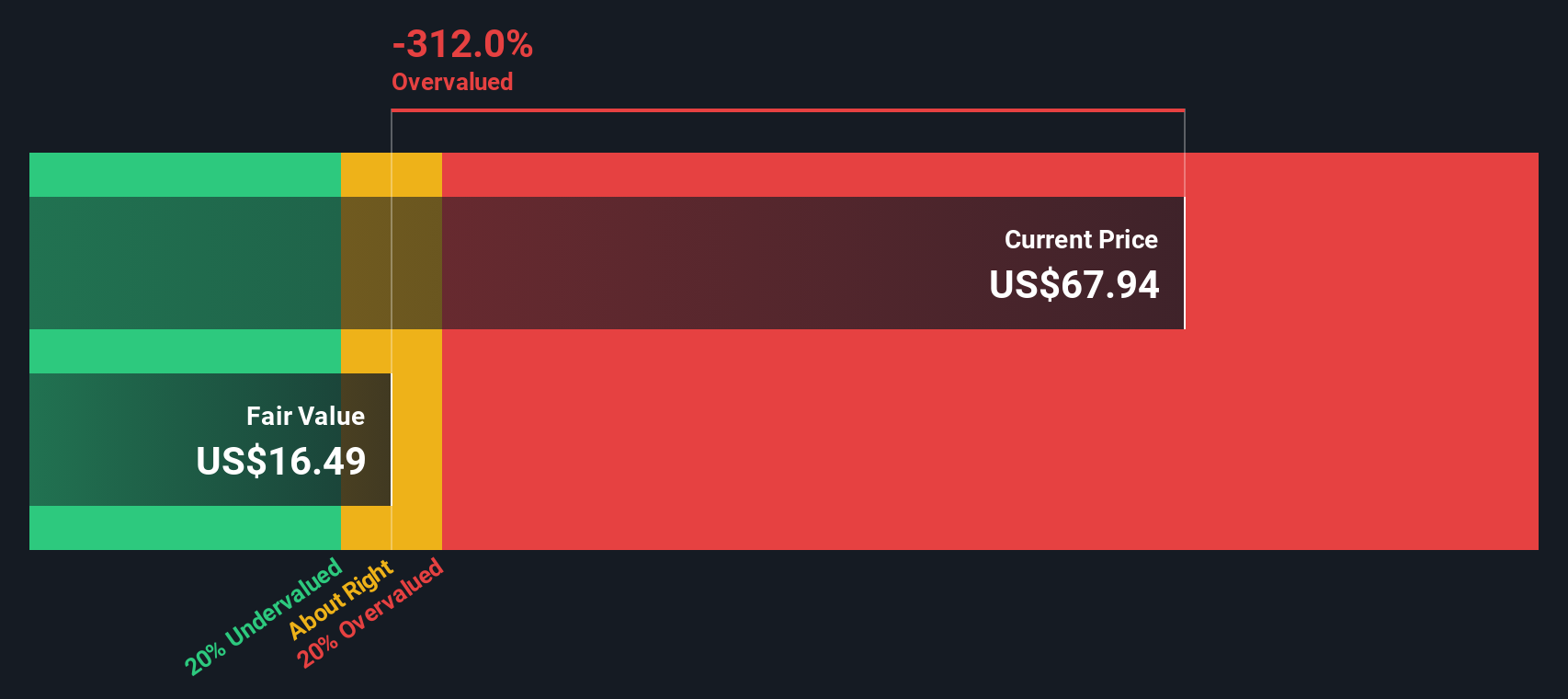

While the most popular narrative paints Figma as undervalued, our SWS DCF model arrives at a far less optimistic result. This approach puts Figma’s fair value at $16.73, which is considerably below the current share price. Could the crowd be overlooking real long-term risks?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Figma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Figma Narrative

If the analysis here does not match your perspective or you are keen to dive into the numbers yourself, you can shape your own narrative in just minutes. Start now: Do it your way.

A great starting point for your Figma research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Take your portfolio to the next level by seizing opportunities that others are missing. The next market leader could be just a click away.

- Boost your income potential by targeting companies rewarding shareholders and check out these 16 dividend stocks with yields > 3% with solid yields above 3%.

- Future-proof your investments by tapping into cutting-edge innovation through these 24 AI penny stocks leading advances in artificial intelligence.

- Capitalize on overlooked value by searching for businesses trading below their true worth among these 870 undervalued stocks based on cash flows powered by strong cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com