- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Are Wayfair’s (W) Efficiency Gains Enough to Offset International Headwinds?

- Wayfair recently reported third-quarter 2025 earnings, posting net revenue of US$3.12 billion and confirming mid-single-digit year-over-year growth projections for the upcoming quarter despite the closure of its German operations.

- This performance, driven by the adoption of AI-powered tools, accelerated delivery logistics, and a growing loyalty program, is attributed to Wayfair’s internal business improvements rather than broader market conditions.

- We’ll explore how this operational momentum for revenue growth and efficiency may affect Wayfair's investment narrative moving forward.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Wayfair Investment Narrative Recap

To be a Wayfair shareholder right now, you need to believe the company's operational improvements, such as its use of AI-powered tools, strengthening logistics, and loyalty program expansion, can drive revenue growth and margin improvement, even as the housing market and macro environment remain uncertain. The recent news, highlighting solid revenue growth and new guidance despite closing German operations, is in line with the company's core catalyst of driving efficiencies and expanding customer engagement; it does not significantly change the main short-term catalyst or its biggest immediate risk.

Among recent announcements, management's confirmation of mid-single-digit year-over-year revenue growth for the fourth quarter, despite a roughly 100 basis point drag from exiting Germany, stands out. This guidance, which incorporates the headwind from international retrenchment, reinforces the importance of operational execution as management focuses on driving top-line growth through internal improvements, matching key catalysts investors are watching closely.

Yet, despite the positive revenue signals, investors should still be aware that heavy spending on advertising and technology, especially if consumer demand does not follow suit, could pressure margins and overall financial health...

Read the full narrative on Wayfair (it's free!)

Wayfair's narrative projects $13.9 billion revenue and $124.7 million earnings by 2028. This requires 4.9% yearly revenue growth and a $424.7 million increase in earnings from -$300.0 million currently.

Uncover how Wayfair's forecasts yield a $112.31 fair value, a 13% upside to its current price.

Exploring Other Perspectives

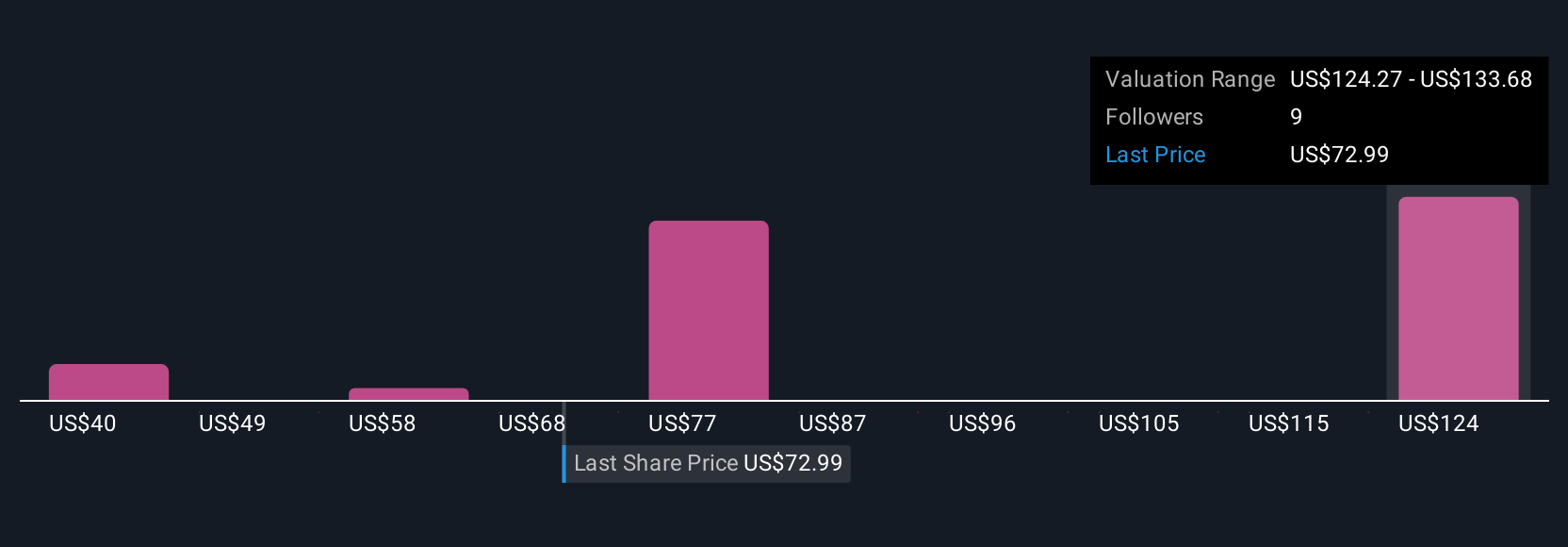

Community-sourced fair value estimates for Wayfair span from US$39.54 to US$202.77 based on five unique perspectives within the Simply Wall St Community. With mixed views on the benefits and timing of heavy tech and logistics investments, you should explore several alternative viewpoints to better inform your assessment.

Explore 5 other fair value estimates on Wayfair - why the stock might be worth over 2x more than the current price!

Build Your Own Wayfair Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Wayfair research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wayfair research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wayfair's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 38 companies in the world exploring or producing it. Find the list for free.

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com