- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Mastercard’s Blockchain Ambitions and New Security Products Might Change The Case For Investing In MA

- In the past week, Mastercard reported third quarter results showing sales of US$8.60 billion and net income of US$3.93 billion, both up from the previous year, and highlighted a 0.64% share repurchase alongside new product launches in payment security and cyber intelligence.

- Additionally, Mastercard is in late-stage talks to acquire stablecoin infrastructure provider Zero Hash for up to US$2 billion, signaling a further push into blockchain and digital assets amid increased competition and institutional interest in stablecoin payments.

- We'll now consider how Mastercard's continued investment in payment security and blockchain infrastructure may shape its broader investment outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Mastercard Investment Narrative Recap

To be a Mastercard shareholder today, you need to believe in the continued global shift to digital payments and the company's ability to stay ahead through technology, partnerships, and innovation. The recent Zero Hash acquisition talks and new product launches in payment security appear to have a limited impact on near-term results but could influence Mastercard’s positioning against emerging payment alternatives; the most important catalyst remains resilient payment volume growth, while competition from domestic payment systems is still the biggest long-term risk.

Among Mastercard’s announcements, the launch of its Threat Intelligence platform stands out as most relevant given the ongoing evolution of digital threats and the rising need for advanced fraud prevention. As Mastercard looks to reinforce its value-added services, developments like this directly tie into efforts to drive higher-margin, recurring revenues and defend its competitive edge, a key catalyst amid changing market dynamics.

Conversely, investors should keep in mind the revenue concentration risk tied to key banking partners and what could happen if...

Read the full narrative on Mastercard (it's free!)

Mastercard is projected to reach $42.6 billion in revenue and $19.9 billion in earnings by 2028. This outlook assumes a 12.1% annual revenue growth rate and a $6.3 billion increase in earnings from the current $13.6 billion.

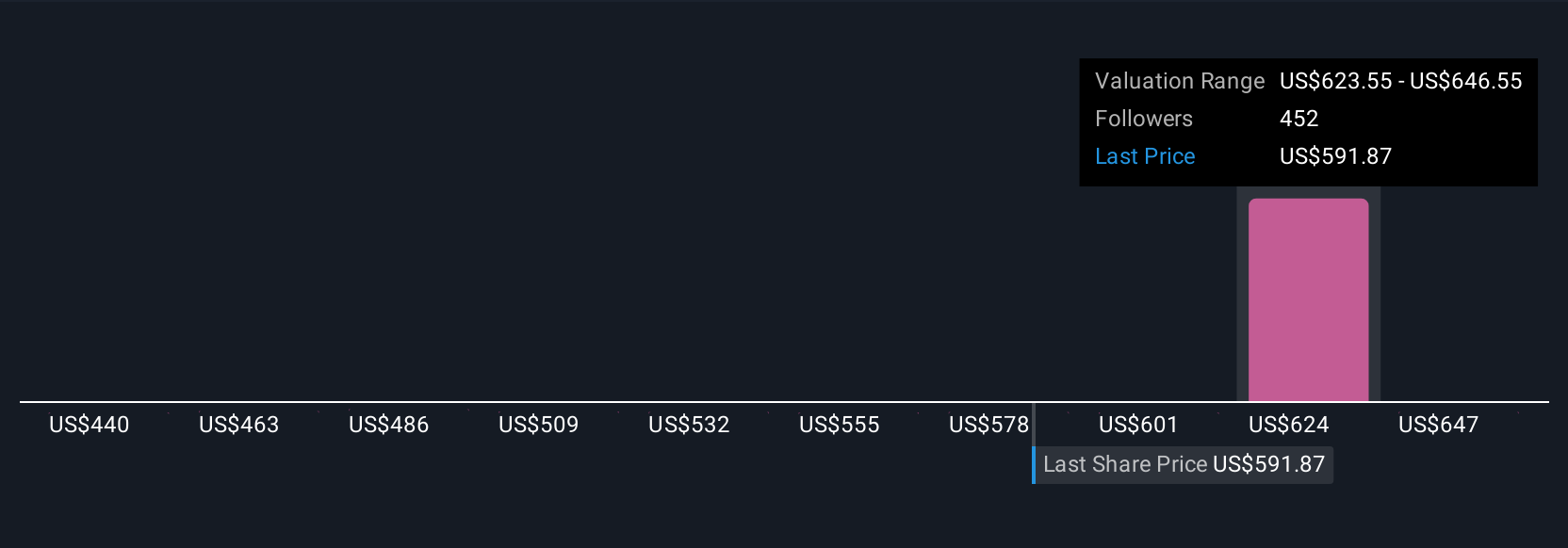

Uncover how Mastercard's forecasts yield a $650.98 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Fifteen private investors from the Simply Wall St Community valued Mastercard between US$500 and US$669.54 per share. While many expect payment volume growth to continue driving results, others see a risk in rising competition from local payment rails, reminding you to consider multiple viewpoints on the company’s future.

Explore 15 other fair value estimates on Mastercard - why the stock might be worth 9% less than the current price!

Build Your Own Mastercard Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Mastercard research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Mastercard research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mastercard's overall financial health at a glance.

No Opportunity In Mastercard?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com