- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Glimpse of PotlatchDeltic's Earnings Potential

PotlatchDeltic (NASDAQ:PCH) is gearing up to announce its quarterly earnings on Monday, 2025-11-03. Here's a quick overview of what investors should know before the release.

Analysts are estimating that PotlatchDeltic will report an earnings per share (EPS) of $0.18.

The market awaits PotlatchDeltic's announcement, with hopes high for news of surpassing estimates and providing upbeat guidance for the next quarter.

It's important for new investors to understand that guidance can be a significant driver of stock prices.

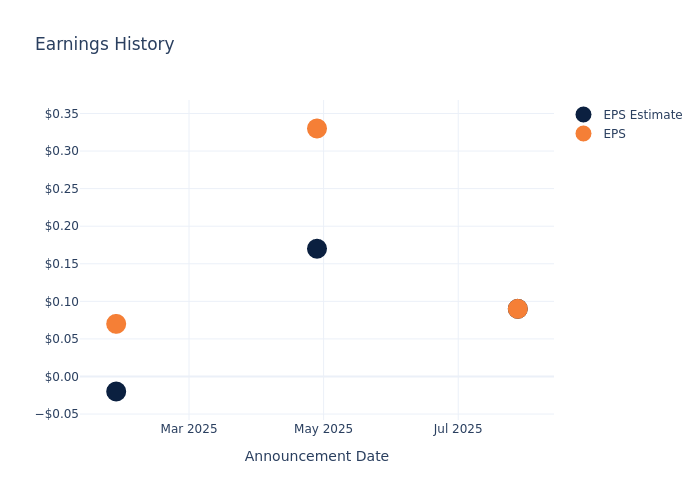

Performance in Previous Earnings

During the last quarter, the company reported an EPS missed by $0.00, leading to a 2.69% increase in the share price on the subsequent day.

Here's a look at PotlatchDeltic's past performance and the resulting price change:

| Quarter | Q2 2025 | Q1 2025 | Q4 2024 | Q3 2024 |

|---|---|---|---|---|

| EPS Estimate | 0.09 | 0.17 | -0.02 | -0.06 |

| EPS Actual | 0.09 | 0.33 | 0.07 | 0.04 |

| Price Change % | 3.00 | -2.00 | -1.00 | -4.00 |

Stock Performance

Shares of PotlatchDeltic were trading at $40.51 as of October 30. Over the last 52-week period, shares are down 6.07%. Given that these returns are generally negative, long-term shareholders are likely upset going into this earnings release.

Insights Shared by Analysts on PotlatchDeltic

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding PotlatchDeltic.

Analysts have provided PotlatchDeltic with 2 ratings, resulting in a consensus rating of Buy. The average one-year price target stands at $48.0, suggesting a potential 18.49% upside.

Peer Ratings Comparison

The analysis below examines the analyst ratings and average 1-year price targets of Outfront Media, Rayonier and Four Corners Property Tr, three significant industry players, providing valuable insights into their relative performance expectations and market positioning.

- Analysts currently favor an Outperform trajectory for Outfront Media, with an average 1-year price target of $20.5, suggesting a potential 49.4% downside.

- Analysts currently favor an Neutral trajectory for Rayonier, with an average 1-year price target of $27.0, suggesting a potential 33.35% downside.

- Analysts currently favor an Neutral trajectory for Four Corners Property Tr, with an average 1-year price target of $28.8, suggesting a potential 28.91% downside.

Summary of Peers Analysis

In the peer analysis summary, key metrics for Outfront Media, Rayonier and Four Corners Property Tr are highlighted, providing an understanding of their respective standings within the industry and offering insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| PotlatchDeltic | Buy | -14.25% | $35.65M | 0.37% |

| Outfront Media | Outperform | -3.58% | $228.70M | 3.13% |

| Rayonier | Neutral | 6.92% | $31.63M | 19.38% |

| Four Corners Property Tr | Neutral | 11.02% | $63.24M | 1.91% |

Key Takeaway:

PotlatchDeltic ranks at the bottom for Revenue Growth and Gross Profit, while it is in the middle for Return on Equity.

About PotlatchDeltic

PotlatchDeltic Corp is a REIT that owns and manages forestland in Alabama, Arkansas, Idaho, Minnesota, and Mississippi. Potlach operates in three segments. The timberlands segment covers the planting and harvesting of trees, as well as the construction and maintenance of roads. The wood products segment manufactures and distributes lumber, plywood, and other wood products. The real estate segment covers the sales generated from company-owned timberlands, as well as commercial and residential properties. The timberlands and the wood product segments combined drive the majority of the company's revenue.

Financial Milestones: PotlatchDeltic's Journey

Market Capitalization Analysis: Falling below industry benchmarks, the company's market capitalization reflects a reduced size compared to peers. This positioning may be influenced by factors such as growth expectations or operational capacity.

Revenue Challenges: PotlatchDeltic's revenue growth over 3 months faced difficulties. As of 30 June, 2025, the company experienced a decline of approximately -14.25%. This indicates a decrease in top-line earnings. In comparison to its industry peers, the company trails behind with a growth rate lower than the average among peers in the Real Estate sector.

Net Margin: PotlatchDeltic's net margin is below industry averages, indicating potential challenges in maintaining strong profitability. With a net margin of 2.67%, the company may face hurdles in effective cost management.

Return on Equity (ROE): PotlatchDeltic's ROE is below industry standards, pointing towards difficulties in efficiently utilizing equity capital. With an ROE of 0.37%, the company may encounter challenges in delivering satisfactory returns for shareholders.

Return on Assets (ROA): PotlatchDeltic's ROA is below industry standards, pointing towards difficulties in efficiently utilizing assets. With an ROA of 0.23%, the company may encounter challenges in delivering satisfactory returns from its assets.

Debt Management: PotlatchDeltic's debt-to-equity ratio is below industry norms, indicating a sound financial structure with a ratio of 0.54.

To track all earnings releases for PotlatchDeltic visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.