- LIVE QUOTES

- LEARN

- HELP

EN

Builders FirstSource (BLDR): Assessing Valuation Following Disappointing Revenue and Guidance Update

Builders FirstSource (BLDR) just posted a quarterly revenue drop of 5% year over year, falling short on both its revenue numbers and annual outlook. Leadership attributed the results to persistent market challenges and revised their full-year guidance to a lower range.

See our latest analysis for Builders FirstSource.

Following the disappointing quarterly update, Builders FirstSource’s 1-year total shareholder return stands at -31.4%, a sharp reversal after robust multi-year gains that saw total returns rise over 100% for three years and 309% across five. Momentum has clearly faded, as investors weigh the impact of softer sales and a cautious new outlook.

If recent volatility has you rethinking your watchlist, this is a prime moment to broaden your search and discover fast growing stocks with high insider ownership

The question facing investors now is whether Builders FirstSource’s recent pullback creates an undervalued opportunity or if the stock’s current price already reflects the company’s slower growth outlook and competitive pressures.

Most Popular Narrative: 11.6% Undervalued

With a fair value set at $140.32 versus a recent close of $124.06, the prevailing narrative points to notable upside based on long-term catalysts and future earnings. The market’s current caution provides the backdrop for a deeper dive into key drivers shaping analyst consensus.

The company is investing heavily in digital transformation and value-added solutions (e.g., digital tools, ERP integration, prefabricated components). These investments are expected to drive higher-margin growth, increase operating efficiency, and strengthen customer relationships as the market recovers, improving both future revenue and net margins.

Want to know which bold financial moves and digital initiatives underpin this value call? The real twist is in future margin targets and a profit multiple more often seen in tech, not building stocks. Tap in to find the full blueprint. Are you ready for the numbers behind the narrative?

Result: Fair Value of $140.32 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent housing market weakness and ongoing pressure from commodity price volatility could challenge Builders FirstSource's growth story and near-term margin outlook.

Find out about the key risks to this Builders FirstSource narrative.

Another View: Market Multiples Tell a Different Story

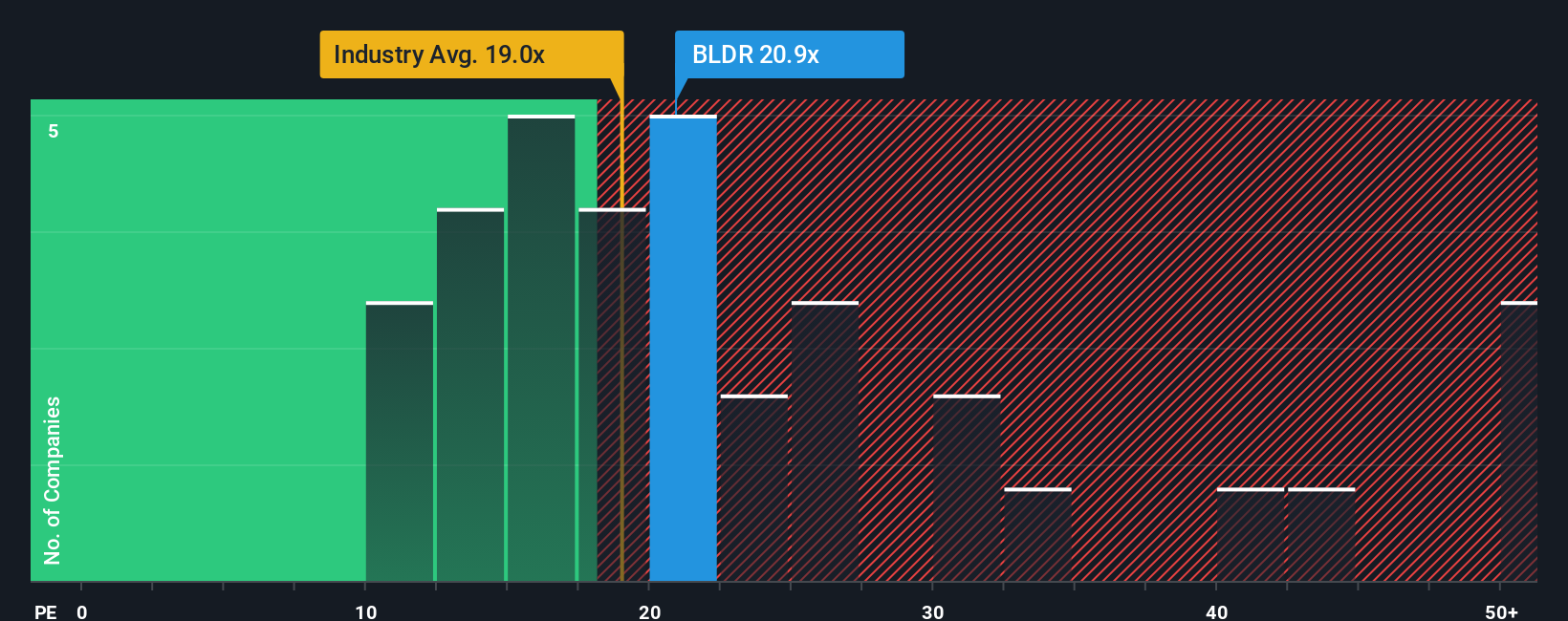

Looking at Builders FirstSource through the lens of its price-to-earnings ratio, the company trades at 18.1x, which is below both the industry average of 19.8x and its peer average of 21x. Notably, the fair ratio sits much higher at 24.4x, marking a visible gap. This metric suggests investors might be discounting the stock’s earnings potential, or perhaps bracing for more turbulence ahead. Could this caution signal upside, or is the market right to stay reserved?

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Builders FirstSource for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Builders FirstSource Narrative

If this outlook does not quite fit with your view or you would rather dive into the numbers yourself, you can build a personalized story in just a few minutes. Do it your way

A great starting point for your Builders FirstSource research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Get ahead of the curve by checking out other handpicked stock lists using the Simply Wall Street Screener. The next opportunity could be waiting for you, so why let it pass by?

- Uncover unmatched value stocks powered by strong future cash flows by starting with these 876 undervalued stocks based on cash flows.

- Tap into the explosive potential of AI-driven businesses positioned for tomorrow’s growth with these 27 AI penny stocks.

- Maximize your long-term income and stability with a line-up of market leaders offering impressive yields, all found at these 17 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com