- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Does Surging Overseas Growth Signal a New Chapter for FinVolution Group (FINV)?

- In the past quarter, Acadian Asset Management LLC reduced its stake in FinVolution Group by 7.1% through selling 394,293 shares, while the company reported a very large 96% increase in international customers, mainly from Indonesia and the Philippines.

- This significant growth in overseas users stands out as FinVolution continues to expand beyond its core Chinese market, countering concerns about regulatory or de-listing risks which analysts currently view as minimal.

- We will explore how the sharp rise in international customer numbers may influence FinVolution Group's growth outlook and investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

FinVolution Group Investment Narrative Recap

To be a shareholder in FinVolution Group today, you need to believe in the company’s ongoing ability to grow internationally and offset any regulatory headwinds in China. The recent stake reduction by Acadian Asset Management is not likely to materially impact the short-term catalyst, which remains the scalability of FinVolution’s overseas customer base, while regulatory and geopolitical risks remain the primary concerns to monitor.

One of the most relevant recent announcements was FinVolution’s continued share buyback activity, with nearly 3.3 million shares repurchased last quarter. This supports the investment narrative of sustained capital returns and growing confidence in the company’s financial position, particularly as it leverages international customer growth to bolster earnings and maintain guidance for double-digit revenue expansion in 2025.

Yet, in contrast to this growth, investors should remain alert to...

Read the full narrative on FinVolution Group (it's free!)

FinVolution Group's narrative projects CN¥18.1 billion revenue and CN¥3.7 billion earnings by 2028. This requires 9.5% yearly revenue growth and a CN¥0.9 billion earnings increase from CN¥2.8 billion.

Uncover how FinVolution Group's forecasts yield a $11.34 fair value, a 57% upside to its current price.

Exploring Other Perspectives

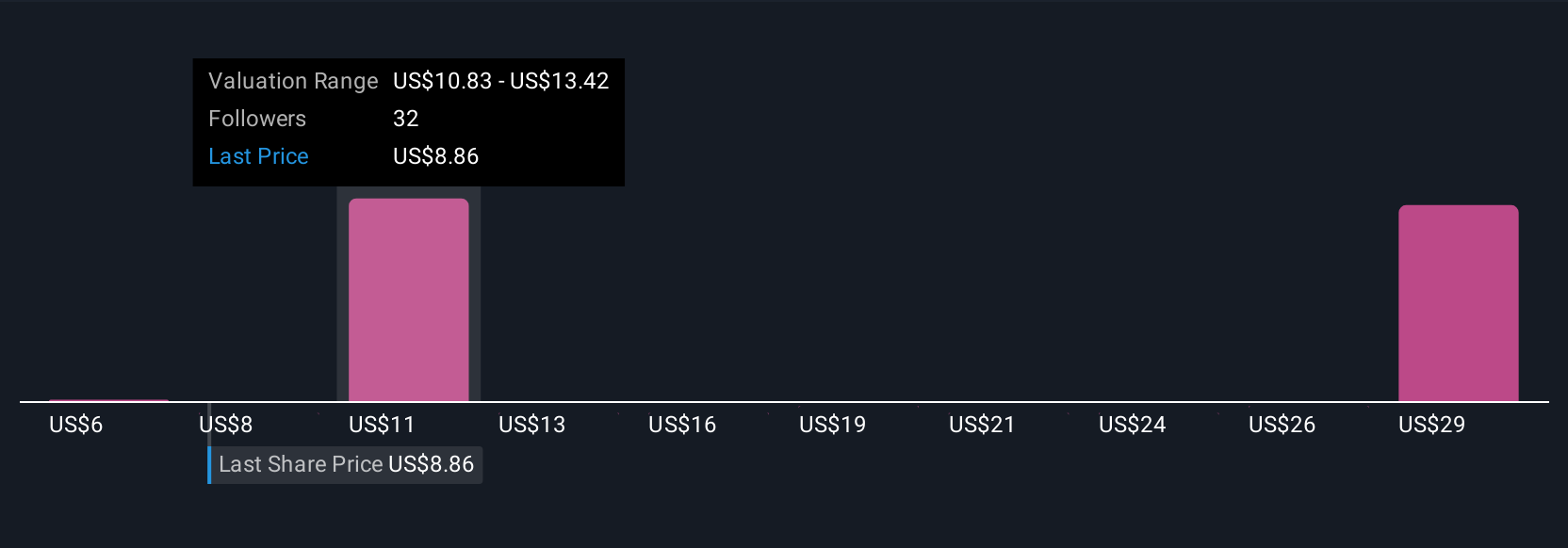

Simply Wall St Community members submitted 11 distinct fair value estimates for FinVolution Group, ranging from US$8.91 to US$28.14 per share. While many see deep value, the company’s rapid growth in Indonesia and the Philippines points to evolving revenue sources that may reshape long-term outcomes, see how other investors are thinking about future risks and opportunities.

Explore 11 other fair value estimates on FinVolution Group - why the stock might be worth over 3x more than the current price!

Build Your Own FinVolution Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your FinVolution Group research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free FinVolution Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FinVolution Group's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com