- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

How Investors May Respond To HCA Healthcare (HCA) Expanding Evidence-Based Stroke Care Across Its Network

- In recent weeks, HCA Healthcare announced the expansion of its evidence-based stroke care initiative from 10 to 43 hospitals, aiming to enhance diagnosis, targeted treatment, and prevention across its network through teamwork, education, and collaboration with the American Heart Association.

- This move highlights HCA Healthcare's ongoing commitment to clinical leadership and patient outcomes, alongside continued operational improvements and investments in digital innovation and care quality.

- We'll now explore how this expanded stroke care initiative may shape HCA Healthcare's investment narrative and outlook for future growth.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

HCA Healthcare Investment Narrative Recap

Owning HCA Healthcare stock means believing in the company’s ability to maintain volume growth in core hospital services while managing cost pressures and policy risks. The recent stroke care initiative expansion reflects HCA’s focus on clinical quality, but does not meaningfully alter the short-term catalyst of margin improvement or the key risk tied to potential policy shifts affecting reimbursement and Medicaid revenue.

A related recent update is HCA’s inclusion in the Russell 1000 Growth-Defensive and Value-Defensive Indexes, which affirms market recognition of its stable earnings and consistent performance, factors that further shape investor views on near-term revenue growth.

Yet, in contrast, investors should also be aware of the ongoing uncertainty surrounding federal healthcare policy and how this could...

Read the full narrative on HCA Healthcare (it's free!)

HCA Healthcare's narrative projects $85.4 billion revenue and $6.9 billion earnings by 2028. This requires 5.5% yearly revenue growth and a $0.9 billion earnings increase from $6.0 billion currently.

Uncover how HCA Healthcare's forecasts yield a $403.81 fair value, a 5% downside to its current price.

Exploring Other Perspectives

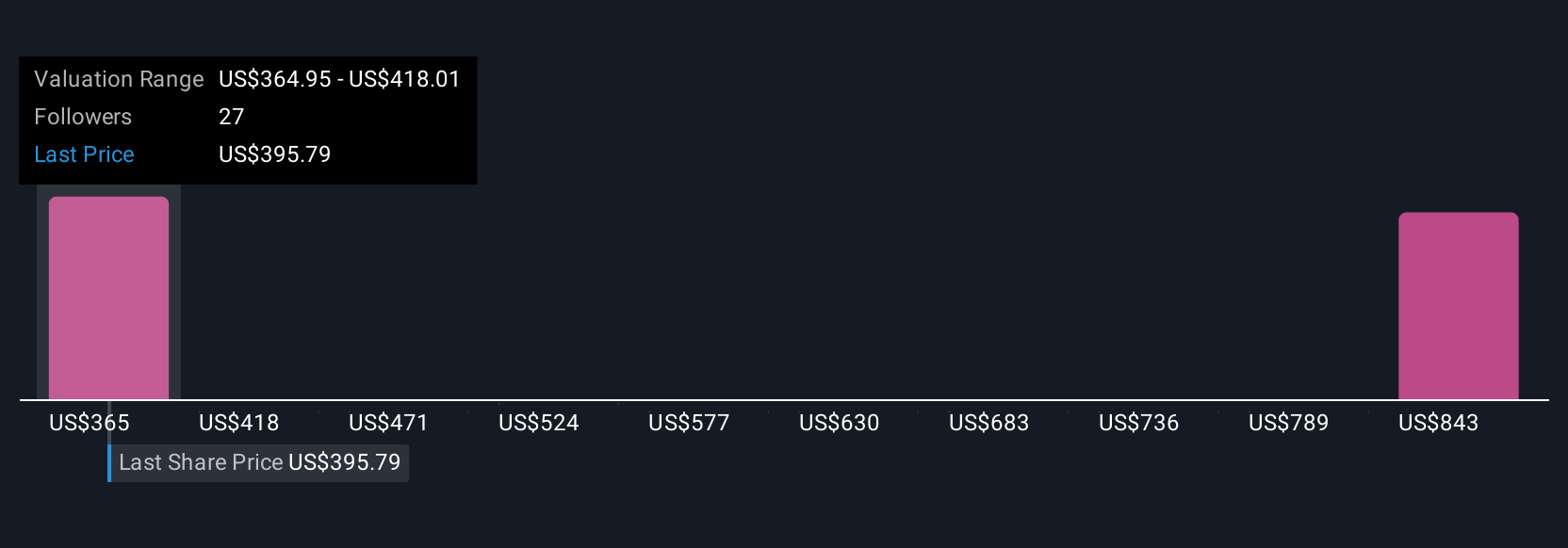

Fair value estimates from the Simply Wall St Community span US$364.95 to US$815.34, with seven distinct viewpoints. Against this backdrop, HCA’s ongoing emphasis on operating margin improvement continues to influence how the company’s performance is evaluated compared to its healthcare peers.

Explore 7 other fair value estimates on HCA Healthcare - why the stock might be worth 14% less than the current price!

Build Your Own HCA Healthcare Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your HCA Healthcare research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free HCA Healthcare research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate HCA Healthcare's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 32 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com